Kathmandu

Tuesday, July 14, 2026

Record remittances, swelling foreign exchange reserves and a massive balance of payments surplus have strengthened Nepal's external position. But beneath the headline numbers, weak investment, sluggish credit growth, rising inflation and a widening trade deficit expose an economy still heavily dependent on overseas earnings

KATHMANDU: Nepal Rastra Bank’s eleven-month review of fiscal year 2025/26, released on July 13, paints the picture of an economy that looks unusually comfortable on its external accounts and dangerously imbalanced on almost everything else. Headline surpluses deserve careful scrutiny when they are not matched by improvements in an economy’s productive base, and Nepal’s latest macroeconomic figures illustrate why.

The country is running a current account surplus of Rs 802.06 billion and a balance of payments surplus of Rs 926.06 billion, both roughly double their year-earlier levels, foreign exchange reserves have swelled 40.3 percent to Rs 3,755.64 billion, sufficient to cover 19.1 months of combined goods and services imports, and the currency has nonetheless depreciated 9.8 percent against the dollar. This is not the profile of an economy strengthening its underlying competitiveness; it is the profile of an economy whose external position is being carried almost entirely by remittances, while the domestic engines of growth, credit expansion, capital investment, and export diversification, are stalling simultaneously.

The remittance-dependency problem, restated in harder terms

Remittance inflows rose 38.2 percent to Rs.2,120.80 billion over the eleven months, or 29.6 percent in dollar terms to USD 14.59 billion, even as the number of Nepalis obtaining first-time approval for foreign employment fell from 452,324 to 367,211. This is worth dwelling on. A rising remittance total paired with a falling outflow of new labor migrants means that the average remittance sent per existing worker abroad has increased substantially, likely reflecting wage gains in destination markets such as the Gulf states, Malaysia, and increasingly South Korea and parts of Europe, combined with greater use of formal banking channels possibly encouraged by the exchange rate differential and improved digital remittance infrastructure.

In IMF program countries with comparable remittance dependence, such as El Salvador or the Philippines, this kind of income is typically treated in Article IV consultations as a structural feature requiring careful macro-prudential management rather than a cause for celebration, precisely because it substitutes for, rather than builds, domestic productive capacity. Nepal’s net secondary income for the period, at Rs 2,321.07 billion, is nearly double the trade deficit of Rs 1,616.13 billion, meaning remittances alone are financing not just the entire merchandise trade gap but generating a substantial surplus on top of it. This is the single most important fact in the entire report: Nepal’s currently comfortable external position exists because Nepali households are effectively subsidizing the country’s import bill out of foreign wages, not because domestic industry, agriculture, or exports are generating the foreign exchange the economy needs.

Trade structure: a deficit that keeps widening despite export growth

Exports grew 12.3 percent to Rs 277.97 billion, but this figure needs to be read against the previous year’s extraordinary 77.8 percent growth, a comparison that reveals last year’s export boom, likely driven by one-off factors in edible oil re-exports and similar trade arbitrage activity given the composition data showing final consumption goods at 69.3 percent of exports, is now normalizing rather than compounding. Imports, meanwhile, grew 15.2 percent to Rs 1,894.10 billion, faster than exports, meaning the trade deficit widened 15.7 percent to Rs.1,616.13 billion and the export-to-import coverage ratio slipped further to just 14.7 percent from 15.1 percent.

For every rupee Nepal exports, it now imports roughly seven rupees worth of goods, an extremely narrow structural base by the standards of any economy, and one that leaves the country acutely exposed to swings in global commodity prices, since petroleum products, silver, transport equipment, and chemical fertilizer dominated import growth. The terms of trade index fell 13.9 percent during the review period, driven by import prices rising 21.0 percent against export prices rising only 4.2 percent, a deterioration that functions as a direct transfer of purchasing power out of the Nepali economy to its trading partners, principally India and China, whose import shares grew 11.8 percent and 21.5 percent respectively.

In classic external-sector analysis, a terms-of-trade shock of this magnitude, combined with rupee depreciation, would normally be expected to compress the current account; that it has not done so here, and indeed the current account improved, is attributable entirely to the remittance offset described above, reinforcing rather than contradicting the structural fragility diagnosis.

Inflation: a late-cycle acceleration with a wholesale-price warning sign

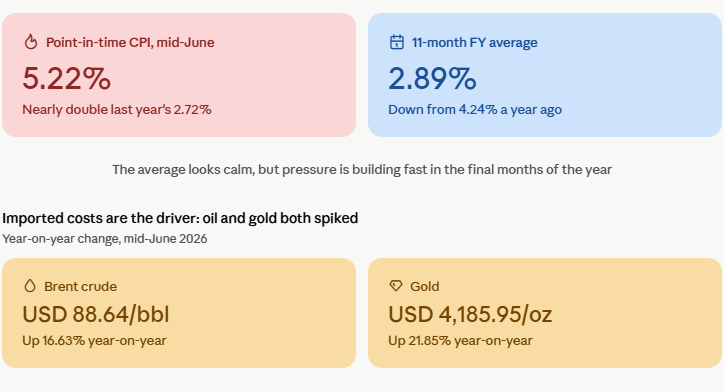

Headline CPI inflation reached 5.22 percent in mid-June 2026, nearly double the 2.72 percent recorded a year earlier, even though the eleven-month average for the fiscal year actually eased to 2.89 percent from 4.24 percent. This divergence between the average and the point-in-time figure indicates that price pressure has been building specifically in the final months of the fiscal year rather than throughout it, a pattern consistent with the transmission of rupee depreciation and higher global oil and gold prices into the domestic price level.

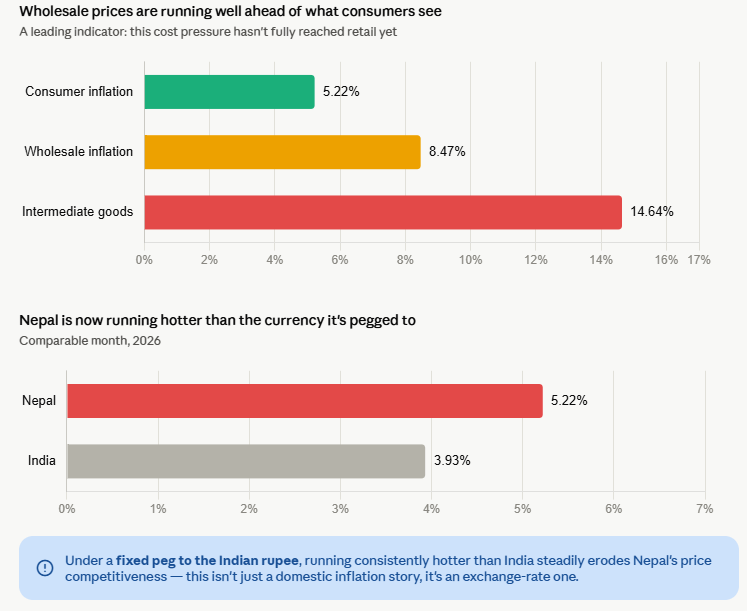

Brent crude rose 16.63 percent year-on-year to USD 88.64 a barrel and gold rose 21.85 percent to USD 4,185.95 an ounce, both squarely imported cost pressures given Nepal’s total reliance on foreign supply for both commodities. More tellingly, wholesale price inflation reached 8.47 percent, far outpacing consumer inflation, with intermediate goods inflation at 14.64 percent. In standard inflation-forecasting frameworks, wholesale or producer price inflation running well ahead of consumer price inflation is treated as a leading indicator: cost pressures embedded in intermediate and capital goods have not yet fully passed through to the retail level, meaning further consumer price increases are likely in the coming months absent an offsetting appreciation of the currency or decline in global commodity prices.

Nepal Rastra Bank should treat this gap as an early warning requiring vigilance, particularly because the country’s inflation, at 5.22 percent, already runs well above India’s 3.93 percent figure for the comparable month, a divergence that matters enormously for a fixed exchange rate regime because it steadily erodes Nepal’s price competitiveness against the currency to which it is pegged.

The exchange rate paradox and monetary policy autonomy

The 9.8 percent depreciation of the rupee against the dollar, more than triple the 3.0 percent depreciation of the prior year, occurred despite reserves rising 40.3 percent and the current account swinging to a larger surplus. Under a conventional floating-rate framework this combination would be almost impossible; a country running twin surpluses of this magnitude would ordinarily see its currency appreciate as capital and current account inflows exceed outflows. The explanation lies entirely in the peg: because the Nepali rupee is fixed to the Indian rupee, Nepal’s bilateral dollar rate simply follows the rupee’s movement against the dollar, regardless of Nepal’s own balance of payments position. This is the core trade-off of any currency board or peg arrangement, well documented in the literature on small open economies with pegged regimes, such as the CFA franc zone or the Eastern Caribbean Currency Union: monetary and exchange rate policy autonomy is sacrificed for exchange rate stability and lower transaction costs with the anchor economy.

For Nepal, this means Nepal Rastra Bank cannot use exchange rate appreciation to offset the imported inflation problem described above, even though its own reserve position would easily support such a move if the peg were more flexible. The central bank’s only available lever is domestic monetary tightening, and the data show it using this lever, reserve money grew just 2.8 percent during the period versus 6.4 percent a year earlier, through open market operations and bond issuance, precisely to sterilize the liquidity injection coming from the remittance-driven foreign asset accumulation.

Liquidity abundance without productive absorption

The scale of Nepal Rastra Bank’s sterilization operations is itself remarkable: the central bank absorbed a net Rs 39,100.70 billion in liquidity through transaction-basis instruments during the review period, nearly double the Rs 21,340.60 billion absorbed a year earlier, primarily through the Standing Deposit Facility at Rs 35,584.20 billion. This is liquidity mop-up on a scale that dwarfs the entire deposit base of the banking system, underscoring just how much excess liquidity the remittance and reserve inflows are generating relative to the economy’s capacity to absorb it productively.

Despite this liquidity abundance, and despite interest rates falling across the board, the weighted average lending rate for commercial banks down to 6.64 percent from 7.99 percent, and base rates down to 4.88 percent from 6.09 percent, private sector credit grew just 6.2 percent during the review period, only slightly below the 8.0 percent growth of the prior year, and domestic credit overall grew just 0.5 percent, a sharp deceleration from 3.4 percent. This is the classic signature of a liquidity trap dynamic in miniature: banks have ample deposits, savings deposits alone rose to 46.6 percent of the total deposit base from 36.2 percent, and can lend cheaply, yet businesses and households are not borrowing at a pace commensurate with the available liquidity.

The most plausible explanations are twofold: first, elevated non-performing loans, at 5.60 percent as of mid-April 2026, are making banks cautious about credit quality even as they cut rates to attract volume; second, real demand for credit remains subdued because businesses face weak domestic demand, itself partly a function of anemic capital expenditure by government, which actually contracted 7.5 percent during the period even as recurrent spending rose 6.7 percent. When the public sector is not investing and private credit growth is stuck near 6 percent in nominal terms, actual real credit growth net of inflation is close to flat, insufficient to support the kind of investment-led growth Nepal needs to reduce its remittance dependence over time.

Capital expenditure contraction is the central concern

The fiscal accounts tell a story of a government that is, in effect, retrenching on investment while its financing needs ease. Total government expenditure grew just 5.0 percent, decelerating from 8.6 percent a year earlier, but this aggregate masks a troubling composition: capital expenditure fell 7.5 percent to Rs 132.67 billion even as recurrent expenditure rose 6.7 percent to Rs 908.27 billion. In public finance terms, this is precisely the wrong direction for a developing economy attempting to build the infrastructure, roads, hydropower transmission, irrigation, that would eventually allow it to diversify exports and reduce its trade deficit.

Capital expenditure as a share of total government spending, already historically low in Nepal due to well-documented weaknesses in project preparation, procurement delays, and local-level implementation capacity, has now fallen further in absolute terms. Meanwhile, the government’s cash balance at Nepal Rastra Bank tripled to Rs 418.54 billion from Rs 137.78 billion, a level that, combined with the capital expenditure shortfall, strongly suggests under-execution of the budget rather than a genuine fiscal consolidation strategy.

Revenue growth also decelerated, total revenue up 6.4 percent versus 10.5 percent a year earlier, with non-tax revenue growth slowing sharply to just 1.9 percent from 8.8 percent, indicating that non-tax revenue sources, often tied to natural resource royalties, dividends from state enterprises, and administrative fees, are not scaling with the broader economy. The improvement in the government’s financing position, net claims on government by the monetary sector fell 35.1 percent, is therefore better read as a symptom of capital spending paralysis than as evidence of fiscal discipline in the constructive sense the term usually implies.

Adequate buffers but watch asset quality and market concentration

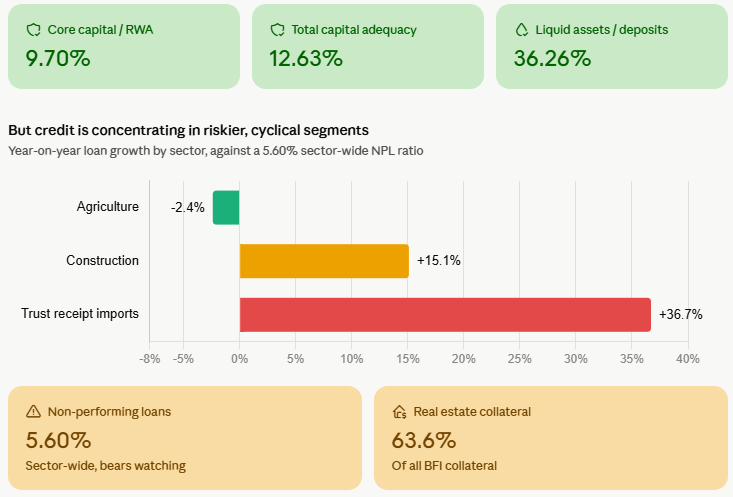

On the positive side of the ledger, Nepal’s banking system continues to show reasonable capital buffers, with core capital to risk-weighted assets at 9.70 percent and total capital adequacy at 12.63 percent, both above the regulatory minimums typically required under Basel-aligned frameworks, and net liquid assets to deposits at a healthy 36.26 percent. However, the non-performing loan ratio of 5.60 percent bears watching, particularly given the sectoral credit data showing agriculture sector loans contracting 2.4 percent while construction sector loans grew 15.1 percent and trust receipt import loans surged 36.7 percent, a combination suggesting credit risk is becoming increasingly concentrated in import-financing and construction exposures precisely as import costs and interest-rate-sensitive real estate collateral, still 63.6 percent of total BFI collateral, come under pressure from the exchange rate and commodity price shocks described above.

The capital market, meanwhile, remains narrow and concentrated: the NEPSE index gained only modestly to 2,724.03 from 2,655.39, market capitalization to GDP actually eased to 70.52 percent from 71.34 percent, and banks, financial institutions and insurance companies still account for 50.9 percent of total market capitalization. A stock market this dependent on the health of the banking sector itself, rather than reflecting a diversified productive economy, offers limited value as an independent barometer of broader economic health and instead essentially duplicates the risks already visible in the banking data.

Overall assessment and outlook

Viewed as a whole, Nepal’s eleven-month macroeconomic position for fiscal year 2025/26 exhibits the structural signature of what development economists sometimes term a “remittance equilibrium”: external accounts that look strong by conventional balance-of-payments and reserve-adequacy metrics, masking a domestic economy where private investment, government capital spending, export diversification, and credit growth are all simultaneously weak. The comfortable reserve position, 19.1 months of import cover, and the large current account surplus provide Nepal Rastra Bank with genuine policy space, space that has been sensibly used to defend financial stability through liquidity sterilization and gradual interest rate normalization.

But reserve adequacy and current account surpluses are necessary, not sufficient, conditions for durable macroeconomic health. The risks to watch over the remainder of fiscal year 2025/26 and into 2026/27 are threefold: first, the wholesale-price-to-consumer-price inflation gap suggests further consumer inflation is likely to materialize even without new external shocks, testing the central bank’s tightening stance; second, continued capital expenditure underperformance by government will constrain the medium-term growth potential needed to eventually wean the economy off remittance dependence; and third, credit quality in import-financing and construction-linked lending warrants close supervisory attention given the confluence of currency depreciation, higher input costs, and already-elevated non-performing loan ratios.

Nepal’s policymakers have, for now, the fiscal and reserve space to address these risks proactively; the eleven-month data suggest the window to do so is open but not indefinite.

![Landless families appeal to NHRC [Photo Feature]](https://english.nepalnews.com/wp-content/uploads/2026/07/IMG-20260714-WA0160.jpg)