Kathmandu

Saturday, July 4, 2026

The government has brought greater urgency to energy reform. Mobilising the capital needed to unlock Nepal’s hydropower potential remains unfinished.

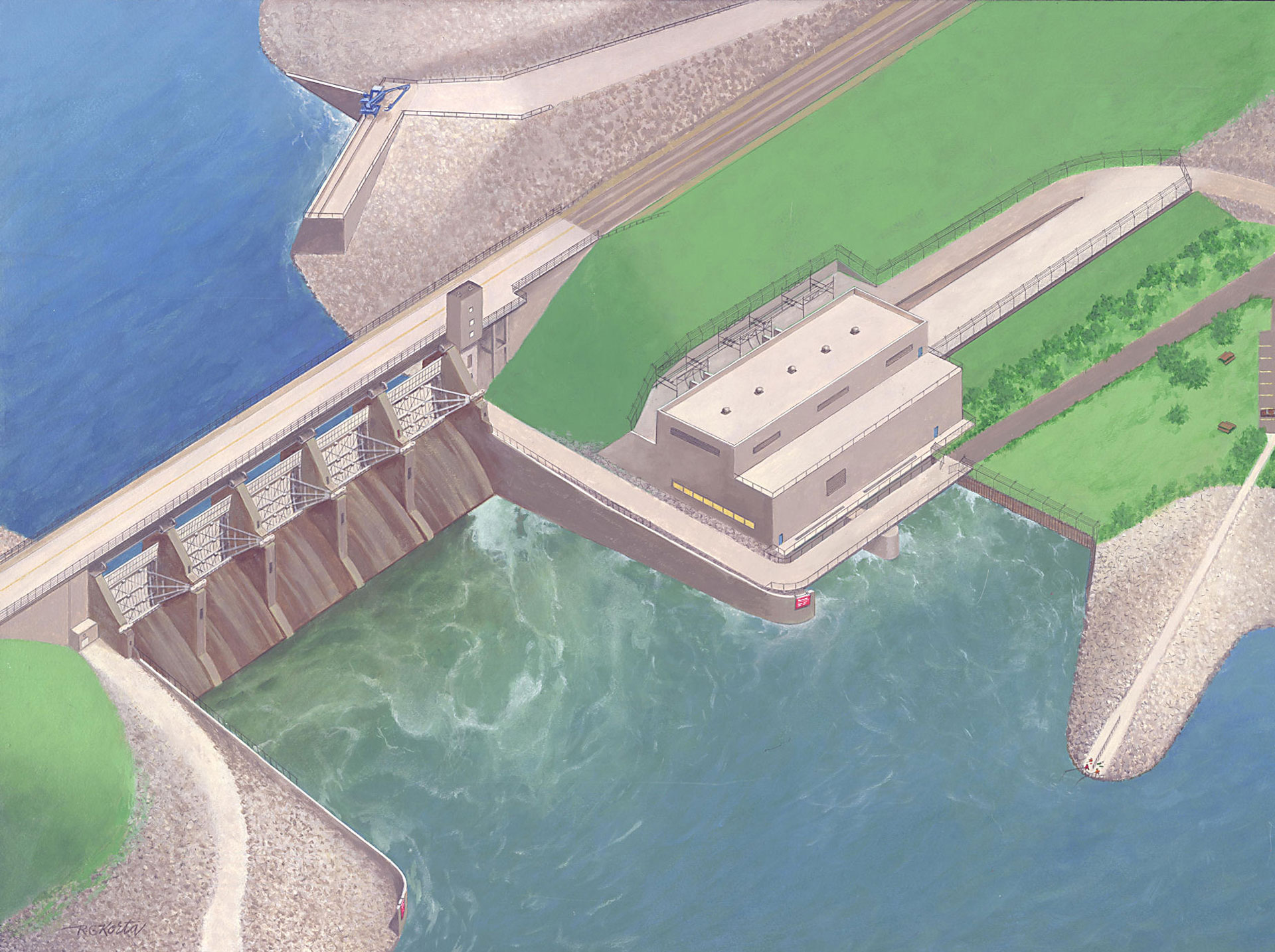

KATHMANDU: Few sectors carry as much transformative potential for Nepal as energy. Hydropower has long been portrayed as the country’s comparative advantage-a resource capable of reducing fuel imports, powering industrialisation, generating export earnings and reshaping the economy.

Yet successive governments have struggled to translate that promise into sustained economic transformation. Projects have stalled, transmission lines have lagged behind generation, investment has been constrained by regulatory uncertainty and ambitious political slogans have repeatedly outpaced implementation.

Prime Minister Balendra Shah has inherited both that opportunity and those structural weaknesses. During its first 100 days, the government has attempted to reposition energy at the centre of its economic strategy, presenting it not merely as an infrastructure sector but as the foundation of long-term economic transformation. The Ministry of Energy, Water Resources and Irrigation has backed that ambition with an Energy Consumption and Export Strategy aimed at expanding domestic electricity use while significantly increasing exports over the coming decade.

The strategy recognises one of Nepal’s longstanding paradoxes: despite producing growing volumes of clean electricity, domestic electricity consumption remains remarkably low.

Per capita electricity use is still a fraction of that in neighbouring emerging economies. Increasing consumption through electrified cooking, transport and industry would not only reduce fossil-fuel imports but also stimulate domestic demand and improve the economics of hydropower investment.

The government also deserves credit for acknowledging a structural weakness that has constrained Nepal’s power system for decades. Heavy dependence on run-of-river hydropower has created large seasonal imbalances, with surplus electricity during the monsoon but shortages in the dry season.

The new strategy places greater emphasis on storage and semi-storage hydropower projects, recognising that a more balanced generation mix is essential if Nepal is to become a reliable regional electricity exporter.

Transmission infrastructure—historically one of the weakest links in Nepal’s electricity sector—has also received renewed attention. Several long-delayed high-voltage transmission lines have moved forward after years of administrative and land acquisition disputes. Progress on the Hetauda-Dhalkebar 400 kV corridor and the long-stalled Balkumari GIS substation illustrates a greater willingness to tackle projects that previous administrations repeatedly postponed. Cross-border transmission projects with India are likewise receiving renewed priority, reflecting Nepal’s growing integration into the regional electricity market.

The budget reinforces this direction. More than Rs. 85 billion has been allocated to electricity generation, transmission and distribution

infrastructure, with particular emphasis on completing strategic transmission lines. The government has also proposed opening electricity trading to the private sector, allowing private investors to participate in cross-border electricity markets while introducing legal provisions for privately financed transmission infrastructure through wheeling charges.

If implemented effectively, these reforms could gradually liberalise Nepal’s electricity market and reduce the financial burden on the state.

The administration has also introduced smaller but symbolically important governance reforms. A 24-hour public hotline for electricity-related complaints, faster customer service, efforts to recover outstanding electricity dues and a review of dormant hydropower licences all reflect a greater emphasis on administrative accountability.

The review of hundreds of project licences may prove particularly significant. For years, speculative licence holding has locked up valuable hydropower sites without meaningful construction, discouraging genuine investors and slowing sectoral development. The government’s willingness to cancel inactive licences could improve market discipline if applied consistently.

These measures represent sensible institutional improvements.

Yet they stop well short of the structural transformation Nepal’s energy sector still requires.

The most important weakness is investment.

Despite presenting hydropower as the engine of economic transformation, the government has yet to create an investment environment capable of attracting the scale of capital required. Nepal will require tens of billions of dollars over the coming decades to finance generation, transmission, storage, grid modernisation and export infrastructure. Public resources alone are insufficient. Success therefore depends overwhelmingly on domestic private investment and large international investors.

Here the government’s record remains mixed.

Although policy announcements have become more ambitious, there is still no clear signal that Nepal has fundamentally improved its investment climate. Investors continue to face lengthy approval processes, overlapping bureaucratic jurisdictions, regulatory uncertainty, inconsistent environmental clearances and prolonged land acquisition disputes. While some administrative bottlenecks have eased, institutional predictability remains weak.

Perhaps more importantly, the government has yet to secure the confidence of major international strategic investors. Global infrastructure funds, sovereign wealth funds, multinational utilities and pension funds continue to invest cautiously in Nepal despite its enormous hydropower potential.

Few landmark foreign direct investment commitments have emerged during the administration’s first 100 days, suggesting that policy confidence has yet to translate into investment confidence.

The government has also struggled to articulate a coherent strategy for engaging large foreign partners beyond neighbouring countries. Nepal increasingly competes with South and Southeast Asian economies for infrastructure capital, yet its investment promotion remains relatively fragmented. There has been little evidence of a coordinated international investment campaign targeting major institutional investors capable of financing multi-billion-dollar energy projects.

Industrial demand also remains underdeveloped.

Expanding electricity generation alone will not transform the economy unless domestic industries consume substantially more power. Nepal still lacks a comprehensive industrial strategy linking cheap electricity with manufacturing, data centres, green hydrogen, electric mobility, digital infrastructure and export-oriented production. Without stronger domestic demand, the country risks producing surplus electricity without generating corresponding industrial growth.

Green hydrogen and battery storage have appeared in government plans, but both remain pilot initiatives rather than components of a broader industrial transformation strategy. Similarly, while electricity exports offer important opportunities, Nepal remains heavily dependent on the evolution of regional electricity markets and bilateral agreements, factors largely outside its direct control.

Regulatory uncertainty also persists. Although licence reforms are welcome, investors continue to seek greater clarity regarding power purchase agreements, tariff structures, currency risks, taxation, project transfers and long-term ownership arrangements. These issues remain among the principal concerns raised by both domestic and international developers.

The sector also continues to face governance risks. Political interference, delays in environmental approvals, legal disputes and changing policy priorities have historically undermined investor confidence. Unless regulatory institutions become more stable and predictable, ambitious export targets may prove difficult to achieve.

Perhaps the government’s greatest challenge lies in bridging the gap between technical planning and economic strategy. Hydropower should not be viewed simply as an export commodity. Its greatest long-term value lies in enabling industrialisation, reducing energy imports, supporting electrified transport, attracting manufacturing and strengthening Nepal’s broader competitiveness. That integrated vision has yet to emerge fully.

None of this diminishes the importance of the reforms already underway. Accelerating transmission projects, improving governance, tightening licence management and preparing long-term export strategies are meaningful achievements. Compared with previous administrations, the government has demonstrated greater administrative urgency and stronger institutional direction.

But energy policy ultimately succeeds not through plans, budgets or strategies alone. It succeeds when capital flows, projects are built, industries expand and electricity becomes the foundation of sustained economic growth.

The Shah government has taken important first steps towards modernising Nepal’s energy sector. Its larger challenge now is convincing investors-both domestic and international-that Nepal is not only rich in hydropower potential but also capable of providing the stable, predictable and commercially attractive environment required to unlock it. Only then can the country’s long-promised energy revolution move from political aspiration to economic reality.

![When Home Minister Gurung fondly mingled with a security check dog [Photo Feature]](https://english.nepalnews.com/wp-content/uploads/2026/07/9f40cd0f-9ebd-4bea-91f4-9b09b07a41b0.jpg)