Kathmandu

Friday, June 26, 2026

Regulatory paralysis at SEBON freezes Rs 66 billion in IPOs, stalls hydropower projects, and fuels legal disputes and corruption concerns across Nepal’s capital market

KATHMANDU: Every time a Nepali company wants ordinary citizens to buy its shares for the first time, it must get permission from the Securities Board of Nepal (SEBON). This system, designed to protect small investors, has collapsed into a bureaucratic swamp.

Companies wait years. Projects stall. Communities go uncompensated. Corruption allegations surface. Parliamentary committees contradict each other. And in the background, Nepal’s dream of becoming a regional electricity powerhouse quietly suffocates: not from lack of rivers, but from lack of regulatory competence.

In plain terms, what exactly is stuck and who is affected?

Think of it this way: 98 separate companies across Nepal have formally knocked on the regulator’s door, submitted their paperwork, paid their fees, and said, “We are ready to raise money from the public.”

Together, these companies want to collect Rs 66.23 billion from ordinary Nepali investors through the sale of 442.17 million shares. That money is not sitting in any account. It does not exist yet. It is waiting to be mobilized the moment a government body called SEBON stamps an approval.

But that stamp is not coming, at least not at any speed resembling normalcy. The affected parties span an astonishing range: power plant builders who cannot finish construction, hotel developers who cannot expand, small manufacturers who cannot scale, and microinsurance companies that cannot reach rural customers.

Securities Board of Nepal (SEBON). File photo

Sitting at the very bottom of this pile are tens of thousands of ordinary Nepali citizens, in villages near rivers, near construction sites, and near project areas, who are legally entitled to receive shares in companies operating in their backyard but have received nothing because the approval chain is broken.

How did a functioning system become this dysfunctional?

The breakdown did not happen overnight. It was assembled piece by piece over several years of neglect and political carelessness. The first serious crack appeared when Nepal’s government of the time allowed SEBON to go without a full-time chairperson from late 2023 onwards, a vacancy that lasted nearly a full year.

Regulatory institutions without leadership do not simply pause and wait. They fragment. Staff morale erodes. Junior officials become unwilling to make decisions. Paperwork piles up. Protests broke out among SEBON employees, further paralyzing the institution from within.

By the time the government appointed Santosh Narayan Shrestha as executive chairperson in November 2024, the backlog had already grown enormous. What followed was 17 months of controversy rather than correction. Shrestha approved a limited number of applications while facing bribery investigations and sustained criticism from industry groups.

He resigned on April 17, 2026. Nepal now once again has no permanent SEBON chairperson, and the cycle of vacancy-and-paralysis is threatening to repeat itself from the beginning. The pattern reveals a structural flaw: Nepal treats its capital market regulator as a political appointment subject to cabinet whims, rather than an independent institution insulated from government transitions.

What is this Rs 90 rule, and who invented it?

On December 28, 2023, the Public Accounts Committee of Nepal’s House of Representatives issued a directive with sweeping consequences. It told SEBON to stop approving IPOs for any company whose net worth per share was below Rs 90.

The logic was protective on the surface: stop loss-making companies from harvesting money from unsuspecting retail investors. But the implementation has been catastrophic.

First, the Rs 90 figure has no basis in any Nepali law. It does not appear in the Securities Act. It is not referenced in any internationally recognized financial standard. SEBON’s own spokespersons cannot point to a statutory foundation for it.

Second, SEBON went a step further by applying a concept called “real net worth,” which does not exist in Nepali legal vocabulary or in standard accounting practice anywhere in the world, as an additional filter. This invented standard gave SEBON enormous discretionary power to reject applications that might otherwise have qualified under conventional accounting measures.

Third, and most damaging, the Finance Committee of the very same parliament later told SEBON that net worth should not be the only criterion for approval, directly contradicting the PAC’s instruction.

SEBON was now trapped between two parliamentary masters issuing opposite commands, and companies were trapped waiting for the contradiction to be resolved.

Why is hydropower particularly devastated by this crisis?

To understand why hydropower companies are suffering more than anyone else, you need to understand one fundamental fact about how they are built and financed. A hydropower project in Nepal is not constructed the way a factory or hotel is. It requires enormous capital expenditure upfront: clearing land, blasting tunnels, building dams, and installing turbines before a single unit of electricity is generated or a single rupee of revenue arrives.

Nepal’s standard financing model for these projects is a 70-to-30 ratio: roughly 70 percent of the project cost is borrowed from banks, and the remaining 30 percent is raised from the public through an IPO.

Representatioal image, Sanibheri Hydropower. File photo

The IPO is not a reward at the end of a successful project. It is a structural component of the financing architecture, without which the project often cannot reach completion. When SEBON refuses or delays the IPO, banks also hold back on disbursing their portion of the loan because the equity base of the project is incomplete.

Construction halts. Deadlines are missed. The Nepal Electricity Authority, which has a contractual agreement to purchase the electricity, imposes financial penalties for every day the project fails to deliver power. Interest on outstanding loans continues to compound. The project that was supposed to generate electricity ends up generating debt. This is the trap that dozens of Nepali hydropower companies currently find themselves in.

How large is the financial damage, and who has calculated it?

The Independent Power Producers’ Association of Nepal put a number to the suffering in October 2025: the total financial cost of IPO delays to the hydropower sector alone had crossed Rs 108 billion. This is not a guess or a rounded estimate: it reflects the accumulated weight of delayed revenue, inflated construction costs, compounding loan interest, and regulatory penalties.

Beyond hydropower, the broader economy has been deprived of Rs 66.23 billion in capital that should have been circulating productively. Consider what that sum represents: it is money that would have gone from Nepali households; from savings accounts, from remittances, from retirement funds, into productive enterprises that generate electricity, process goods, provide tourism services, and create employment. Instead, it sits frozen in a regulatory queue.

The Rs 1.5 trillion that the private hydropower sector has already invested in Nepal sits increasingly at risk because the final capital-raising instrument that developers planned around is indefinitely delayed.

At the project level, individual hydropower developers face a grimly compounding arithmetic: every month without IPO approval means higher construction costs, more unpaid loan interest, and a shrinking window before penalty clauses kick in.

Who specifically has been rejected and thrown out of the queue?

SEBON’s enforcement of the Rs 90 net worth rule resulted in at least 14 companies being formally removed from the IPO pipeline. The hydropower companies that lost their queue position include Laughing Buddha Power Nepal, Yambaling Hydropower, Unique Hydropower, Beni Hydro, Puwa Khola One Hydro, Sanima Hydro, Richet Hydropower, and Jhapa Energy.

The non-energy companies swept out in the same process include Accord Pharmaceuticals, Apex Hospitality, Annapurna Cable Car, Orchid Holdings, Prabhu Helicopter, and Kantipur Television. One hydropower company was expelled on a separate technical ground: its Power Purchase Agreement with the NEA had fewer than five years of validity remaining, which SEBON considered too short to assure investors of sustainable returns.

SEBON stated that all removed companies retain the right to reapply after meeting the specified conditions. But that offer rings hollow for a company mid-construction, carrying bank debt, and legally prohibited from generating electricity yet.

Improving net worth to Rs 90 per share requires either generating profits or injecting more promoter capital, both of which are nearly impossible for a project that has not yet produced a kilowatt of electricity.

What has the crisis done to local communities who live near these projects?

Nepal’s law contains a specific, well-intentioned provision: hydropower companies must allocate 10 percent of their IPO shares to people whose land, water, or livelihoods have been affected by the project. This is not charity. It is a legal obligation, designed to ensure that communities bearing the environmental and social cost of hydropower development receive a financial stake in return.

The IPO bottleneck has made this provision meaningless in practice. Companies cannot distribute what they have not been authorized to issue. Communities that gave up farmland, lived through years of construction dust and noise, and watched their rivers altered have received nothing.

The frustration has boiled over in some project areas, with residents reportedly vandalizing company vehicles, a striking inversion of the usual dynamic, where protesters oppose projects.

Here, communities are angry not because a project exists, but because the benefits they were promised are being withheld by a bureaucratic failure in Kathmandu that they had no part in creating and no power to resolve.

What corruption allegations emerged from this crisis?

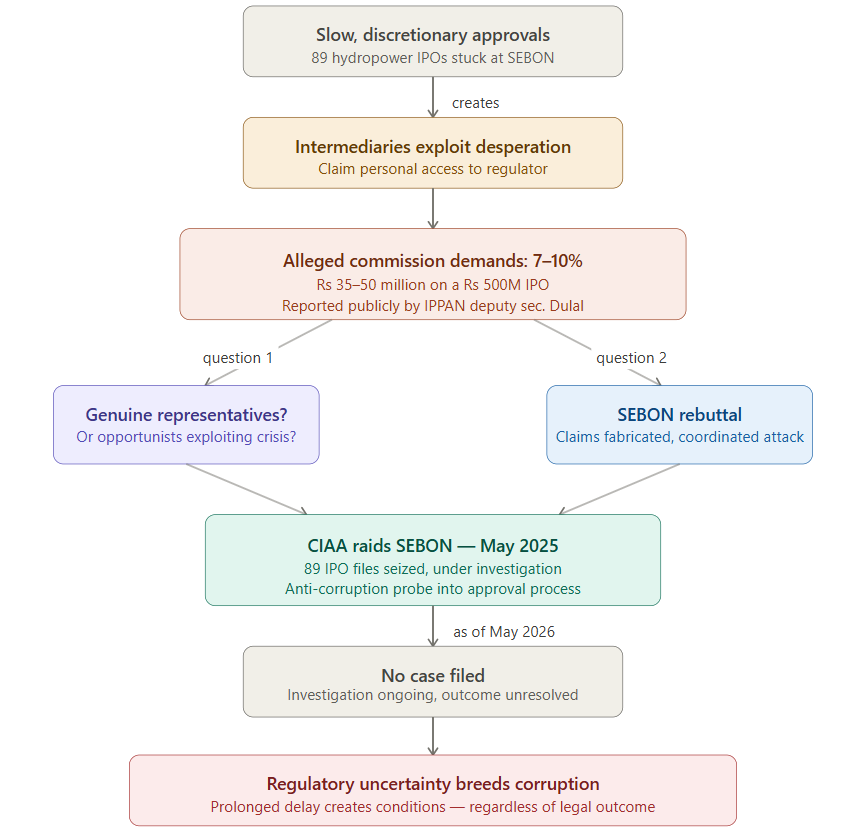

Wherever official approval processes are slow and discretionary, intermediaries thrive. IPPAN’s deputy general secretary Prakash Chandra Dulal went public with a specific and serious allegation: individuals claiming personal connections to then-SEBON chairman Santosh Narayan Shrestha were approaching hydropower developers and demanding commissions of between 7 and 10 percent of the total IPO amount in exchange for expediting approvals.

On even a Rs 500 million IPO, that amounts to a bribe demand of Rs 35 to Rs 50 million. The allegation left open the crucial question of whether these individuals genuinely represented the chairman or were opportunists exploiting a climate of desperation.

SEBON issued a sharp rebuttal, calling the claims fabricated, characterizing them as part of a coordinated campaign to damage the regulator’s credibility, and challenging anyone with concrete evidence to come forward. The Commission for the Investigation of Abuse of Authority investigated the matter.

In May 2025, the Commission for Investigation of Abuse of Authority (CIAA) carried out a raid at the Securities Board of Nepal (SEBON) and seized files related to 89 hydropower companies awaiting approval for initial public offerings (IPOs). The seized documents are now under investigation as part of the anti-corruption body’s probe into irregularities in the IPO approval process.

As of May 2026, no case had been filed. What the episode conclusively demonstrated, regardless of legal outcome, is that prolonged regulatory uncertainty does not simply cause inconvenience: it actively creates the conditions for corruption to flourish.

What shadow market has grown in SEBON’s absence?

With the front door of the capital market effectively closed, companies have found a side door. An unregulated pre-IPO market has expanded dramatically in Nepal, with companies raising hundreds of millions of rupees from private investors before receiving any SEBON approval.

The mechanics work like this: a company uses merchant banks, WhatsApp messages, direct SMS, and personal referral networks to sell equity stakes at prices significantly above the Rs 100 face value of shares. Investors are told that once the company eventually lists on NEPSE, the shares will trade at Rs 1,500 to Rs 2,500, and after a lock-in period expires, they can cash out handsomely.

Companies including Laxmi Steels, Sunrise Holdings, Annapurna Cable Car, Ridge Line Energy, Muktinath Cable Car, and Supreme Pharmaceuticals have been actively operating in this space. The legal ground underneath this activity is dangerously thin.

A Supreme Court ruling from the Unity Life scandal established that any company selling shares to more than 50 people falls under SEBON’s jurisdiction, but enforcement has been essentially absent. Senior SEBON officials privately acknowledge the problem but have taken no decisive action. The consensus fear is that Nepal may be building toward a major retail investor scandal.

How are parliamentary committees making things worse rather than better?

Nepal’s parliament has two committees with overlapping oversight of financial institutions: the Public Accounts Committee (PAC) and the Finance Committee. Both are issuing instructions to SEBON. Both instructions contradict each other.

The PAC says to block all IPOs where net worth is below Rs 90. The Finance Committee says net worth alone cannot be the blocking criterion. SEBON is left choosing which parliamentary master to obey, while companies and investors watch from the sidelines. This is not a minor procedural confusion, it is a governance failure that has paralyzed a regulator for over two years.

Adding to the institutional chaos, several parliamentarians have used SEBON’s committee appearances as occasions for theatrical criticism rather than constructive reform. Members accused the regulator’s leadership of market manipulation, loss of investor confidence, and partisan appointment practices.

While some of this criticism may be entirely justified, none of it has produced clear corrective legislation. The PAC directive that started this crisis was itself issued by a committee that has since been dissolved. Yet SEBON continued enforcing its directive long after the body that issued it ceased to exist: a regulatory posture that raises serious questions about institutional judgment.

What does the new post-production IPO proposal mean for the sector?

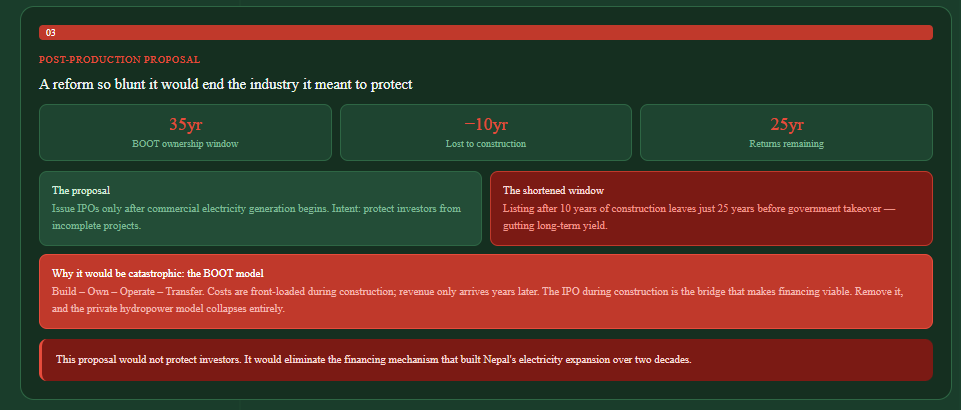

The High-Level Economic Reform Recommendation Commission proposed something that alarmed the entire hydropower industry: requiring companies to issue their IPOs only after the project has begun generating electricity commercially. The intent of preventing investors from funding projects that may never reach completion sounds reasonable. The implementation would be disastrous.

Hydropower development in Nepal follows what is called the BOOT model: Build, Own, Operate, Transfer. Private developers construct and run a project for between 30 and 35 years, after which ownership transfers to the government. The entire financing architecture of these projects is front-loaded: costs are highest during construction, revenues only arrive years later.

The IPO during construction is precisely what bridges this gap and makes the financing viable. Requiring post-production IPOs would eliminate this bridge at the worst possible moment. Worse, under the BOOT framework, if developers only list on the stock exchange after the project is generating revenue, shareholders would have a drastically shortened window of ownership before government takeover.

A project that operates for 35 years but lists after 10 years of construction leaves investors with only 25 years of returns before the asset transfers away. Industry observers argue that this proposal would effectively end the private hydropower development model that has driven Nepal’s electricity expansion over the past two decades.

What has SEBON said in its own defense?

SEBON has not been entirely silent or passive, and its institutional perspective deserves fair representation. The regulator’s spokesperson has consistently maintained that approvals are processed on the basis of complete documentation and full regulatory compliance and that companies meeting all stated requirements receive clearance without unnecessary delay.

SEBON argues that many applications remain pending not because of institutional foot-dragging but because the applicant companies themselves have not submitted complete paperwork or have unresolved compliance deficiencies that must be addressed before public investors can be invited.

The regulator also points to the new framework announced in mid-April 2026, which it says introduces greater transparency and speed into the IPO processing system.

SEBON further notes that over the course of the Shrestha tenure, more than a dozen companies did receive approval and proceeded to list successfully. From the regulator’s perspective, the Rs 90 threshold is a legitimate investor protection measure, and approving financially weak companies would expose retail investors, many of them ordinary Nepalis with limited financial literacy, to the kind of losses that have historically damaged trust in the capital market.

The defense has not satisfied industry groups, but it reflects a genuine tension between investor protection and capital market efficiency that has no easy resolution.

How has this crisis damaged investor confidence beyond the companies waiting in line?

The damage to investor confidence is both immediate and long-term. In the immediate sense, the pipeline of new investment opportunities for retail Nepali investors has shrunk dramatically. IPOs are one of the most accessible and popular investment instruments in Nepal: ordinary citizens apply for shares using their Demat accounts, investing as little as Rs 10,000, in the hope of receiving an allotment and making a return once the company lists.

When the pipeline of new IPOs dries up, this opportunity disappears. In the longer term, the crisis signals to potential investors, both domestic and foreign, that Nepal’s capital market regulatory environment is unreliable, politically vulnerable, and prone to indefinite gridlock.

The emergence of the pre-IPO black market is perhaps the starkest evidence of this confidence collapse: investors are so hungry for new opportunities and so doubtful that SEBON will deliver them that they are willing to hand money to unverified operators in an entirely unregulated space. That is not a sign of investor optimism, it is a sign of institutional despair.

How does this connect to Nepal’s energy export ambitions?

Nepal has a commercially transformative opportunity in front of it. India has already been importing 1,000 MW of Nepali electricity and has expressed willingness to absorb considerably more. Regional energy trade, including potential exports to Bangladesh, has been discussed at the highest diplomatic levels.

Nepal’s government has committed to a 28,500 MW generation target by 2035, which requires roughly USD 46.5 billion in total investment. Private hydropower developers, who currently supply the majority of Nepal’s domestically generated electricity, are indispensable to achieving that target.

The IPO crisis does not merely delay a few individual projects. It structurally undermines the capital-raising mechanism that the entire private energy development model depends on.

Every month that SEBON fails to clear its backlog is a month where 975 MW of hydropower capacity under development remains financially stalled, where projects facing construction deadlines fall further behind, and where Nepal’s export revenues from electricity remain lower than they should be.

The countries Nepal hopes to sell electricity to are watching, and what they see is a country that cannot coordinate its own regulatory institutions well enough to let its private sector access public capital.

What reforms do stakeholders actually want?

The reform demands coming from different stakeholder groups are fairly consistent, even if the political will to implement them is not. IPPAN and hydropower developers want the Rs 90 net worth threshold abolished or replaced with a sector-appropriate framework that accounts for the fact that construction-phase companies will naturally have lower net worth than operational ones.

They also want the inter-parliamentary contradiction between the PAC and Finance Committee resolved through a clear, unified legislative position. Industry groups want fixed, publicly stated processing timelines at SEBON so that a company knows within a defined period whether its application is approved, rejected, or requires additional information.

Merchant bankers want the pre-IPO market brought under transparent regulatory oversight before it causes a scandal. Capital market reformers want SEBON’s leadership selection process insulated from political transitions so that a change in government does not automatically mean another year of regulatory paralysis.

And virtually everyone agrees that the multi-agency documentation burden, requiring sequential approvals from the ERC, the Company Registrar, and SEBON, needs to be streamlined into a more coordinated and time-bound process.

What immediate steps have been taken, and have any worked?

Several partial measures have been announced. SEBON declared a new streamlined framework in April 2026, although this came just days before the chairman resigned, raising obvious questions about implementation continuity.

The Electricity Regulatory Commission chairperson publicly committed to making pre-SEBON documentation requirements more efficient. Individual hydropower companies that did meet the Rs 90 threshold managed to get through the queue eventually, Solu Hydropower, for instance, received approval and conducted a successful IPO in November 2025, with its foreign employment quota oversubscribed.

These individual successes demonstrate that the system is not completely non-functional: it is selectively functional, which may be worse in some respects, because it fuels suspicion about why some applications advance while others with similar profiles do not.

The formation of a 15-member protest coordination committee by IPPAN, and the association’s public issuance of a 15-day ultimatum to SEBON in October 2025, generated enough political pressure to force some ministerial engagement. But no structural fix has been legislated, no parliamentary contradiction has been formally resolved, and no permanent SEBON leadership is yet in place.

What is at stake if nothing changes in the next 12 months?

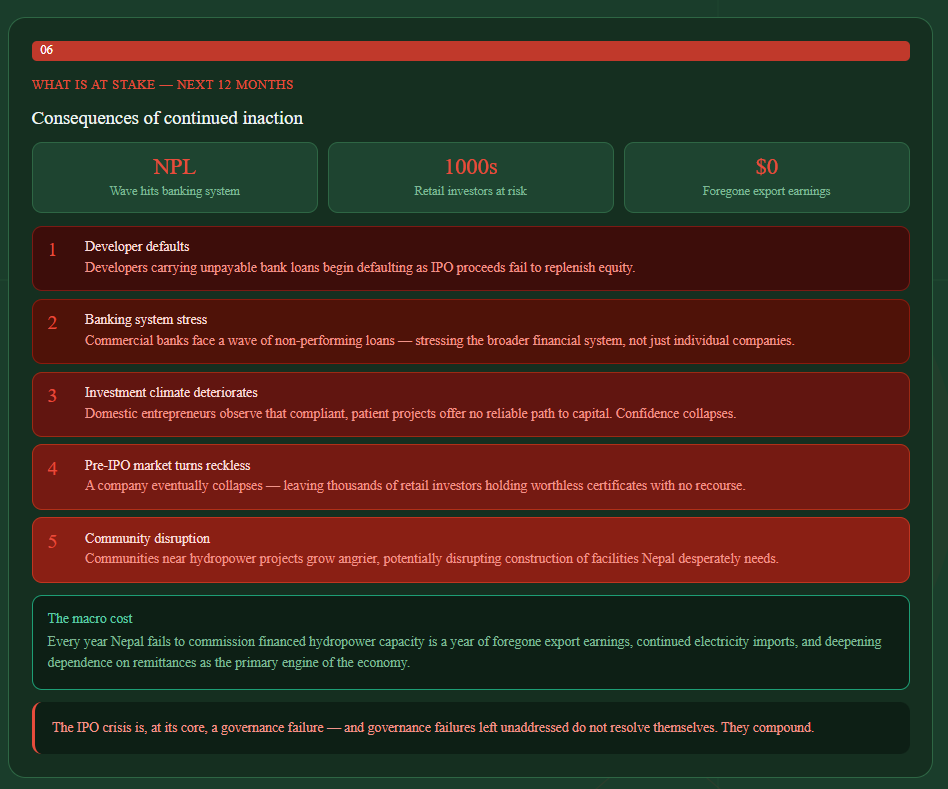

The consequences of continued inaction are not abstract or distant. In the energy sector, developers carrying unpayable bank loans will begin defaulting. Commercial banks that lent to hydropower projects on the assumption that IPO proceeds would replenish the equity base will face a wave of non-performing loans, which will stress the broader financial system, not just individual companies.

Nepal’s private investment climate will deteriorate further, as domestic entrepreneurs observe that building a compliant, legally structured project and patiently waiting in SEBON’s queue offers no reliable path to capital. The pre-IPO market will expand into increasingly reckless territory, and eventually a company will collapse, leaving thousands of retail investors with worthless certificates and nowhere to seek redress.

Communities near hydropower projects will grow angrier, potentially disrupting construction or operation of facilities that Nepal desperately needs. And at a macro level, every year that Nepal fails to commission hydropower capacity it has already financed is a year of foregone export earnings, continued electricity imports, and deepening dependence on remittances as the primary engine of the economy.

The IPO crisis is, at its core, a governance failure, and governance failures left unaddressed do not resolve themselves. They compound.