Kathmandu

Monday, July 13, 2026

Record bank earnings mask a deeper problem: weak credit growth, mounting bad loans and a widening gap between savings and productive investment

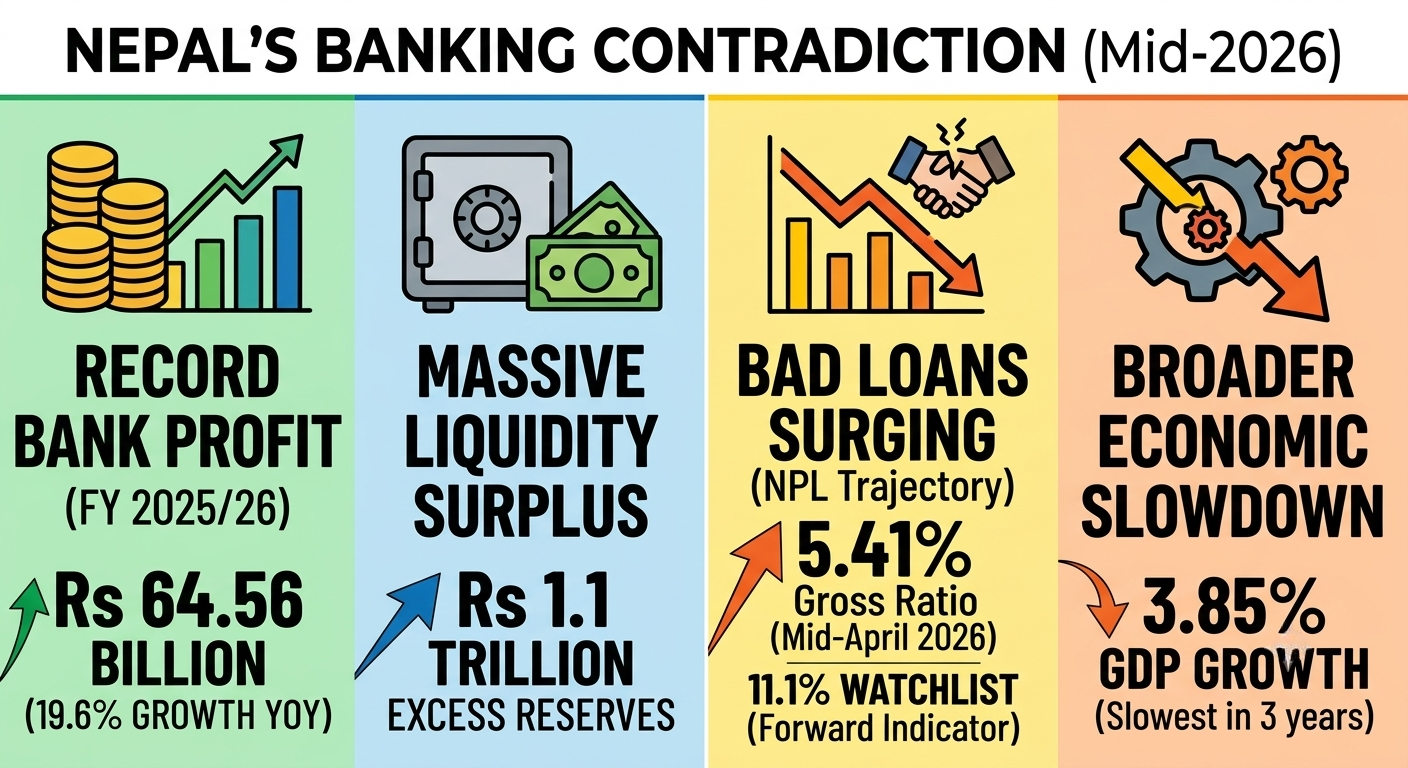

KATHMANDU: Nepal’s banking sector in mid-2026 presents one of the more unusual paradoxes in South Asian finance: an industry reporting record profit growth, comfortable capital buffers, and a liquidity surplus so large that regulators openly worry about where to park it, sitting directly alongside a non-performing loan trajectory that has more than tripled in a decade and a real economy that just recorded its slowest growth in three years.

Understanding why all of this is true at once, and what it means for the year ahead under a newly announced but deliberately unchanged monetary policy, requires pulling apart four interlocking stories: the profit and liquidity story, the asset quality story, the macroeconomic backdrop the National Statistics Office just laid bare, and the policy story Nepal Rastra Bank has now bet on to reconcile all three.

The profit paradox, and what it actually measures

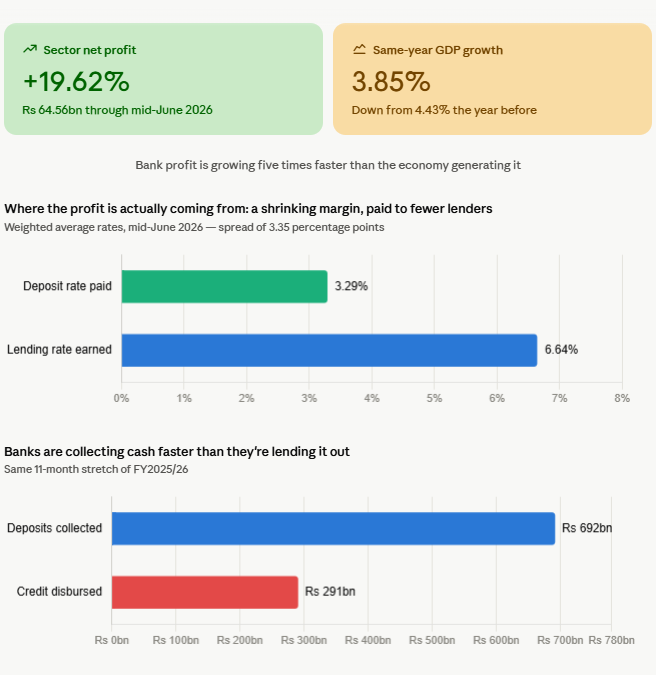

Start with the headline that looks most reassuring. Nepal’s 20 commercial banks earned a combined Rs 64.56 billion in net profit through mid-June 2026, an 19.62 percent jump over the same 11-month period a year earlier. Read in isolation, this looks like an industry in rude health. Read against the rest of the data, including the National Statistics Office’s newly released preliminary estimate that the whole economy grew just 3.85 percent in the same fiscal year, down from a revised 4.43 percent the year before, it looks more like an industry harvesting the easy gains available in a low-cost, low-competition funding environment rather than one earning its way through vigorous, well-priced lending growth into a genuinely accelerating economy.

The mechanics matter here. A commercial bank’s core profitability lever is net interest margin, the spread between what it pays depositors and what it earns from borrowers. With the weighted average deposit rate falling to just 3.29 percent and the weighted average lending rate easing to 6.64 percent by mid-June 2026, the arithmetic spread of roughly 3.35 percentage points is respectable by regional standards, but it is being generated on a shrinking base of genuinely new lending. Deposit collection of Rs 692 billion against credit disbursement of just Rs 291 billion in the same stretch of fiscal year 2025/26 tells the real story: banks are not growing profit primarily by writing more loans, they are growing it by paying savers less for money they already have in abundance, while simultaneously recovering previously delinquent loans that had been dragging on prior-year earnings.

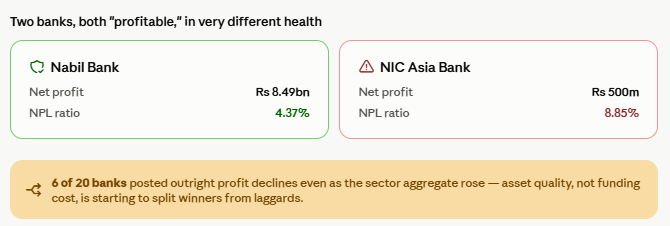

This is not an indictment of individual banks’ management, most of whom are behaving rationally given the incentives in front of them. It is, however, a warning against reading the profit headline as evidence that the underlying credit intermediation function of the banking system is working well. A bank that earns Rs 8.49 billion, as Nabil did, while carrying a 4.37 percent non-performing loan ratio is in a fundamentally different position than one earning Rs 500 million, as NIC Asia did, while carrying an 8.85 percent ratio and Rs 22.32 billion in provisioning, even though both technically posted a profit. The dispersion across the 20 banks, with six recording outright declines even as the sector aggregate rose, is itself a signal that asset quality divergence, not funding cost alone, is beginning to separate winners from laggards within the industry.

Why bad loans keep rising

The non-performing loan trajectory is the sharpest edge of this story, and the newly available detail on watchlist loans changes how it should be read. From a low of 1.20 percent in fiscal year 2021/22, the commercial bank ratio has climbed to 5.41 percent by mid-April 2026, the most recent figure Nepal Rastra Bank has published, since its detailed loan-classification data structurally lags its monthly balance-sheet releases by roughly two months. But the more forward-looking number sits one tier below outright non-performance: loans classified under the watchlist category, meaning those overdue between 31 and 90 days but not yet formally non-performing, rose from 6.7 percent of the total loan portfolio in mid-July 2023 to 11.1 percent by mid-April 2026. This is a genuinely important distinction.

Net non-performing loans, after subtracting the specific provisions banks have already set aside, remain contained at under 1.5 percent, which is why Nepal Rastra Bank can accurately describe the system as still within manageable limits in any given quarter. But a watchlist ratio that has nearly doubled in under three years is precisely the kind of leading indicator that tends to convert into tomorrow’s non-performing loan headline, and it suggests the deterioration documented so far is not close to having run its course.

Nepal Rastra Bank,Thapathali. File photo

In absolute terms, total non-performing loans held by commercial banks reached Rs 220.33 billion in fiscal year 2024/25 alone, a 22.4 percent jump in a single year. That the increase is concentrated overwhelmingly in privately owned banks, up 26.31 percent to Rs 191.63 billion, versus a nearly flat 1.48 percent rise for state-owned banks, undercuts any simple narrative that Nepal’s problem is primarily inefficient public-sector lending, the more familiar Bangladeshi and, historically, Indian pattern. Nepal Rastra Bank’s own supervisors have been unusually candid about why.

The Bank Supervision Report for fiscal year 2024/25 documents practices recognizable from India’s twin balance sheet crisis a decade ago: loans disbursed to firms with negative net tangible worth, financing extended beyond a borrower’s approved drawing power, loan rollovers timed to disguise overdue accounts at quarter-end, and restructuring exercises carried out without reassessing whether the underlying business remained viable. These are governance failures, not macroeconomic accidents, the direct product of what supervisors describe as compromised independence for chief risk officers and internal auditors whose performance reviews are effectively controlled by the same chief executives whose lending decisions they are meant to scrutinize.

Layered on top is a structural collateral problem the newer data makes explicit: roughly three-fifths of all bank loans in Nepal are secured against real estate, and with that market now stagnant following the correction that began around 2022 to 2023, banks are finding it increasingly difficult to actually liquidate collateral to recover value once a loan sours, turning what should be a recoverable asset into a frozen one. Nepal Rastra Bank’s own prescribed remedy, pushing banks toward project-based and character-based lending supported by a more institutionalized individual credit-scoring system, is a sound long-term direction, but it does nothing to unfreeze the roughly three-fifths of the existing loan book already sitting on real estate collateral that cannot currently be sold at anything like its book value.

The liquidity glut and the resource gap

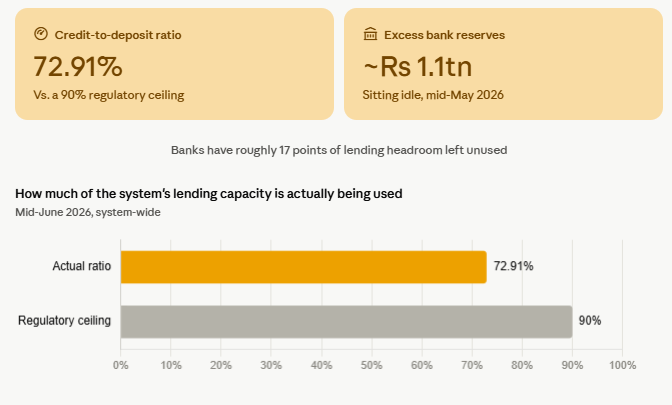

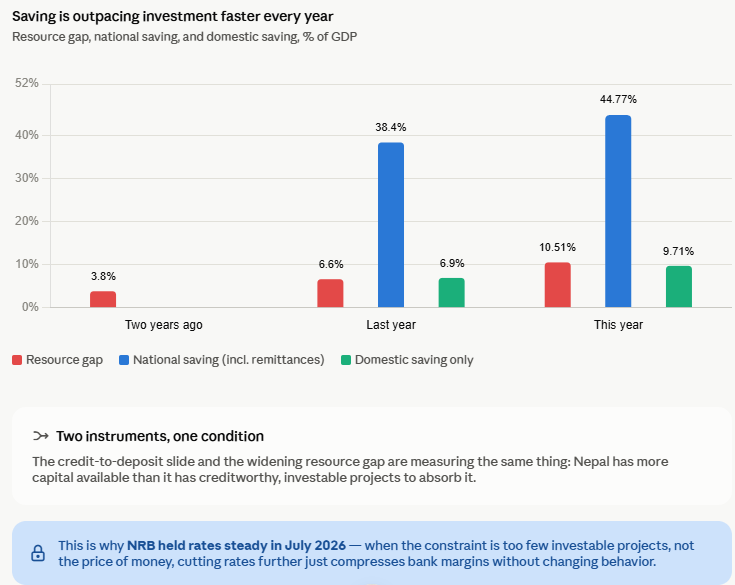

If rising non-performing loans represent the asset side of Nepal’s banking sector going wrong, the liability side tells an almost inverse story of accumulating too much of a good thing without a productive outlet, and the newly released national accounts data reveals this is not just a banking-sector phenomenon but a whole-economy one. The credit-to-deposit ratio has fallen in an uninterrupted multi-year slide, standing at 72.91 percent system-wide as of mid-June 2026, even as the regulatory ceiling remains a full 90 percent. Excess reserves in the banking system stood at roughly Rs 1.1 trillion by mid-May 2026.

The National Statistics Office’s own figures now put a precise number on the macroeconomic version of this same problem. Nepal’s resource gap, meaning the difference between what the country invests domestically through gross capital formation and what it saves, reached 10.51 percent of GDP in fiscal year 2025/26, up sharply from 6.60 percent the year before and just 3.8 percent two years earlier, a near tripling in just two years. Over the same period, gross national saving, boosted heavily by remittances, climbed to 44.77 percent of GDP from 38.4 percent, while gross domestic saving, the portion generated purely within Nepal rather than from abroad, rose more modestly to 9.71 percent of GDP from 6.9 percent.

Read together, these numbers say something quite specific: Nepal is saving an increasing share of its national income, that saving is disproportionately foreign-sourced through remittances rather than domestically generated, and a widening share of it is simply not being converted into productive investment, whether through bank credit or direct capital formation. The banking sector’s credit-to-deposit slide and the nation’s widening resource gap are, in effect, two different instruments measuring the identical underlying condition: Nepal has more capital available than it currently has viable, bankable uses for.

This is not a uniquely Nepali affliction, but the scale of the mismatch, a resource gap that nearly tripled in two years against remittance inflows equivalent to a third of GDP, is unusually stark even by the standards of remittance-dependent economies. It also explains why Nepal Rastra Bank’s monetary policy tools, which mainly work by changing the cost of capital, have had limited traction: when the binding constraint is not the price of money but the absence of enough creditworthy, investable projects to absorb it, cutting interest rates further simply compresses bank margins without meaningfully changing behavior, which is precisely the logic behind the central bank’s decision to hold rates steady in July 2026 and instead pursue structural measures.

Why credit growth stayed weak and what would actually need to change

Nepal Rastra Bank’s own diagnosis of the credit conundrum, now stated with unusual clarity in its July 2026 Macroeconomic Report, identifies four constraints operating together rather than any single cause: binding capital adequacy at many individual banks, a binding credit-to-deposit ratio for some institutions, declining asset quality that is itself forcing more cautious underwriting even where surplus cash exists, and the combination of post-Gen Z political uncertainty with a stagnant real estate market that underpins most collateral.

The third of these deserves particular emphasis, because it means the credit conundrum and the non-performing loan problem are not two separate crises running in parallel, they are the same crisis viewed from two different angles. Rising bad loans make banks more cautious about new lending; more cautious lending, in an economy already short of viable investable projects, leaves deposits piling up unlent; and a widening pool of unlent deposits does nothing to address the underlying governance and collateral problems generating the bad loans in the first place. Breaking this loop requires progress on all three simultaneously, not sequentially.

Encouragingly, Nepal Rastra Bank has set out a fairly specific structural agenda for trying to do exactly that: ending unlimited personal liability on loan guarantees to reduce a disincentive that discourages new borrowing and guaranteeing altogether, easing blacklisting consequences for a single bounced cheque so minor incidents don’t permanently exclude otherwise viable borrowers from the formal system, and studying how a more institutionalized individual credit-scoring system and peer-to-peer lending platforms could reduce the system’s near-total reliance on real estate as collateral.

Nepal Rastra Bank’s own forecast, that credit growth rebuilds to roughly 11 percent and money supply grows 14 percent in fiscal year 2026/27, effectively bets that these structural fixes, combined with continuing political stability following the March 2026 election’s decisive mandate, will be enough to break the loop within a single fiscal year. Given that the same report’s own four-factor diagnosis shows the problem is genuinely multi-causal, that forecast should be read as an optimistic upper bound rather than a base case, particularly since fiscal policy, examined next, is not currently pulling in the same direction with the urgency the situation calls for.

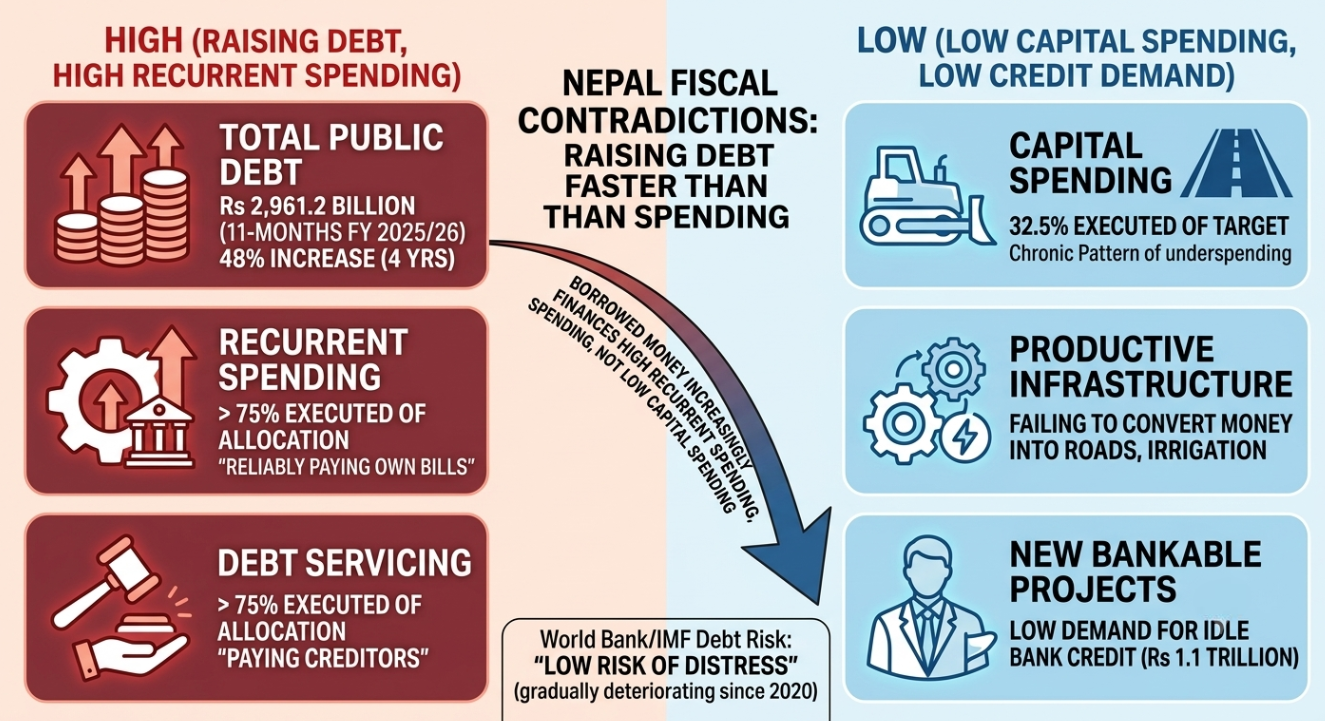

A government that raises debt faster than it spends it

Nepal’s banking sector story cannot be fully separated from what is happening on the fiscal side, and the picture there adds a further layer of concern rather than offering an offsetting source of demand. Through the first eleven months of fiscal year 2025/26, total government expenditure reached only 68.6 percent of its annual budget target, and capital spending, the money that actually builds roads, irrigation, and productive infrastructure, executed at just 32.5 percent of target, continuing a chronic pattern in which Nepal allocates budgets far more effectively than it spends them.

Recurrent expenditure and debt servicing, by contrast, both executed at well over 75 percent of their allocations, meaning the government is reliably paying its own bills and its creditors while consistently failing to convert borrowed and budgeted money into the kind of infrastructure investment that would generate new bankable projects for the private sector to build around, and new demand for the very bank credit currently sitting idle.

Against this backdrop, Nepal’s total public debt rose from about Rs 2,010 billion in fiscal year 2021/22 to Rs 2,961.2 billion by the eleven-month mark of 2025/26, a cumulative increase of around 48 percent in four years, with debt-to-GDP climbing from 40.4 percent to 44.9 percent over the same period. A joint World Bank and International Monetary Fund debt sustainability analysis still classifies this as low risk of distress, but the Macroeconomic Report itself notes Nepal’s own composite risk score in these assessments has been gradually deteriorating since 2020.

The more immediate concern is less the debt level itself than what the borrowed money is actually funding: with only about a third of the capital budget executed, a large share of new borrowing effectively finances recurrent spending and existing debt service rather than the productive infrastructure that would expand the economy’s future capacity to repay it, or generate the kind of large-scale, bankable projects that could absorb some of the banking sector’s Rs 1.1 trillion in excess reserves.

The government’s record Rs 2,124.3 billion budget for 2026/27, about 25 percent above the prior year’s revised estimate and including a doubling of the income tax exemption threshold from Rs 500,000 to Rs 1 million alongside a cut in the top marginal rate from 39 to 29 percent, is designed to boost private consumption and investor confidence, and Nepal Rastra Bank’s decision to hold monetary policy steady is explicitly meant to complement this expansionary fiscal stance. But if the pattern of the past several years holds and capital spending again lags badly behind allocation, the fiscal side of the equation will keep failing to generate the demand for credit that the monetary side has already made so cheap to supply.

What Bangladesh, Sri Lanka and India suggest about the roads not yet taken

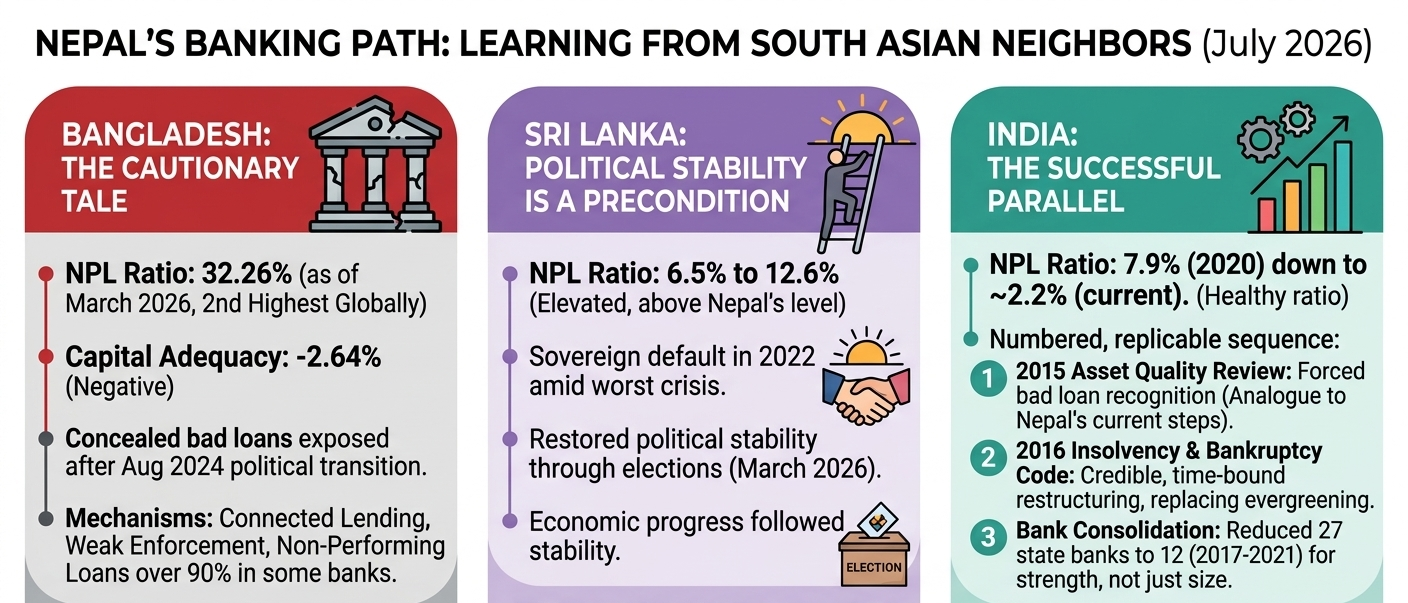

Nepal’s current position becomes clearer when set against its immediate neighbors, each of whom has already lived through a version of the choice Nepal now faces. Bangladesh represents the starkest cautionary tale in the region. Its banking sector’s non-performing loan ratio reached 32.26 percent of total loans by March 2026, the second highest in the world after war-torn Ukraine, and its capital adequacy ratio actually turned negative, at minus 2.64 percent, after the political transition of August 2024 forced the exposure of bad loans concealed for years through exactly the kind of practices Nepal Rastra Bank’s own supervisors have now documented domestically: connected lending, aggressive rescheduling that masked true asset quality, and weak enforcement that let individual banks accumulate non-performing loan ratios above 90 percent.

The parallel for Nepal is not one of scale, Nepal’s roughly 5.6 percent ratio and 12.5 to 12.6 percent capital adequacy ratio are categorically healthier, but one of mechanism: the specific governance practices Nepal has already flagged, left unaddressed for long enough at scale, are what produced Bangladesh’s outcome.

Sri Lanka offers a more encouraging, if still humbling, comparison. Despite a sovereign default in 2022 amid its worst economic and political crisis in decades, Sri Lanka has since restored political stability through elections and made substantial economic progress, even as its non-performing loan ratio remains elevated at somewhere between 6.5 and 12.6 percent depending on the measurement period, still above Nepal’s current level.

The lesson here is less about banking mechanics specifically and more about sequencing: political stability, once achieved, appears to be a genuine precondition for banking sector health to improve rather than a parallel track that can be addressed independently, a pattern Nepal’s own trajectory, from the September 2025 Gen Z protests through the March 2026 election that delivered a near two-thirds parliamentary majority, appears to be following in miniature.

India provides the most directly instructive parallel, because it actually solved a version of the exact problem Nepal now faces. India’s twin balance sheet crisis, in which over-leveraged corporations and a bank system carrying rapidly rising bad loans reinforced each other’s distress, pushed its non-performing loan ratio to roughly 7.9 percent in 2020; it has since fallen to around 2.2 percent, among the healthier ratios in Asia, through a specific and replicable sequence: the Reserve Bank of India’s 2015 Asset Quality Review forced banks to recognize hidden bad loans rather than continuing evergreening, a direct analogue to what Nepal Rastra Bank’s Bank Supervision Report has just begun doing by publicly naming loan rollover and restructuring abuses; the 2016 Insolvency and Bankruptcy Code gave creditors a credible, time-bound path to restructure or force asset sales, replacing a system with strong incentives to keep extending troubled loans rather than crystallizing losses; and consolidation among the weakest public sector banks reduced India’s state-owned bank count from 27 to 12 between 2017 and 2021, combining weaker balance sheets with stronger management and capital rather than simply reducing headcount.

Nepal’s own Banking Sector Reform Task Force has been asked to answer the same question India confronted a decade ago, and its December 2025 report shows early signs of learning the right lessons rather than reaching for the most obvious but least effective tool, notably pushing back against reflexive further mergers on the grounds that Nepali banks which remained independent have often outperformed those that consolidated, a more sophisticated reading than simply copying India’s merger playbook wholesale.

What would genuinely move the needle

Taken together, the evidence points toward a fairly specific diagnosis and a correspondingly specific set of priorities for Nepal’s banking sector over fiscal year 2026/27. The capital position is adequate for now, at roughly 12.5 to 12.6 percent against an 11 percent floor, but that cushion has already compressed from over 13 percent less than a year ago, and it will erode faster than headline numbers suggest if the watchlist-to-non-performing pipeline continues converting at anything like its recent pace, particularly for the cluster of banks, NIC Asia, Prabhu, Nepal Investment Mega, Himalayan, and Kumari among them, already carrying ratios above 6.5 percent.

The most urgent fix is not more liquidity, since Nepal already has roughly Rs 1.1 trillion of it sitting idle, and not lower interest rates, since lending rates at 6.64 percent are already historically cheap; it is governance and collateral. Restoring genuine independence to chief risk officers and internal auditors would directly address the mechanism the Bank Supervision Report identifies as the proximate cause of loan rollover and restructuring abuse.

Diversifying away from the roughly three-fifths of the loan book currently anchored to a stagnant real estate market, through the credit-scoring and character-based lending reforms Nepal Rastra Bank has already outlined, would reduce the collateral-liquidation bottleneck currently trapping banks even when a borrower is willing to settle.

On the liquidity and resource-gap side, the more durable fix lies not in monetary policy at all but in the government finally closing the gap between what it allocates and what it actually spends: capital budget execution running at just 32.5 percent is not a banking sector problem, but its solution would directly generate the large, bankable infrastructure projects capable of absorbing a meaningful share of the sector’s excess reserves, doing more to close Nepal’s 10.51 percent of GDP resource gap than any conceivable further easing of bank lending rates.

Nepal is not Bangladesh, and its capital position gives it real room to act before a governance problem becomes a solvency crisis. Whether it uses that room, whether the government converts this year’s record budget into actually executed capital spending rather than another year of underspending, and whether the watchlist loan pipeline can be arrested before it fully converts into headline non-performing loans, will likely be the defining triad of Nepal’s banking and macroeconomic story for fiscal year 2026/27.