Kathmandu

Monday, June 29, 2026

A government with an overwhelming mandate promised to rebuild the economy. Instead, it has left investors asking not how to expand-but who will be arrested next.

KATHMANDU: Rarely in Nepal’s political history has a government entered office with such extraordinary public legitimacy. Following the Hosue of Representative election on March 05, 2026, the Rastriya Swatantra Party (RSP) secured an almost two-thirds parliamentary majority-an electoral mandate powerful enough to reshape the country’s political and economic trajectory.

It arrived with promises of clean governance, an uncompromising assault on corruption, and a bold economic transformation. Public expectations were immense. Millions believed Nepal had finally reached a political turning point; that decades of stagnation, patronage and institutional decay would give way to a more prosperous and accountable state.

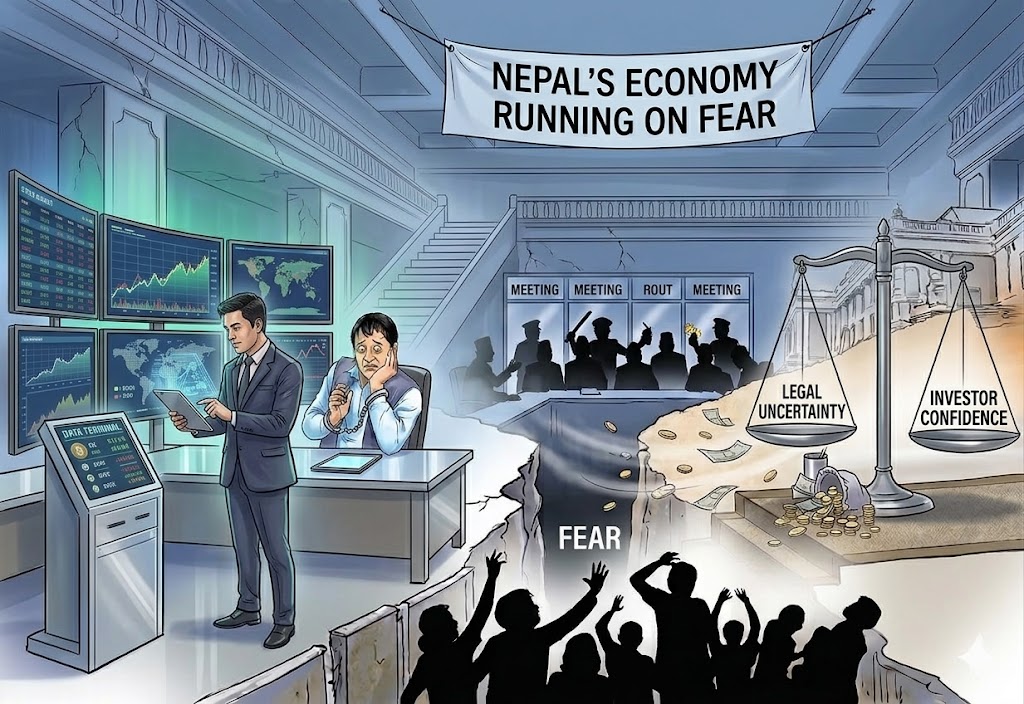

Only months later, that optimism has largely evaporated. The national conversation has changed. In Nepal’s marketplaces, business clubs and corporate boardrooms, entrepreneurs are no longer debating expansion plans or new investments. Their conversations revolve around a different question: “Who will be arrested next?”

For many in the private sector, this is no longer idle speculation. It is a measure of uncertainty. And uncertainty, more than taxation or regulation, is among the most powerful enemies of economic growth.

The psychological shock

To understand today’s business climate, one must return to September 2025. The Gen Z-led protests of September 08-09 became one of the most traumatic episodes for Nepal’s private sector in recent memory. What began as demonstrations rapidly descended into widespread violence. Businesses were selectively targeted. Shops were burned. Factories were vandalised. Businessmen homes were attacked. Years of accumulated investment disappeared overnight.

According to the World Bank’s Nepal Development Update (April 2026), the unrest inflicted economic losses equivalent to roughly 1.3% of Nepal’s GDP. Yet the direct financial damage may not prove the lasting legacy.

The deeper scar was psychological. Capital is ultimately built on confidence. An entrepreneur who watches his factory burn or his business destroyed does not immediately begin planning another investment. Buildings can be rebuilt; confidence takes considerably longer.

From anti-corruption to economic anxiety

The political transition that followed introduced an aggressive anti-corruption campaign.

In principle, few would dispute its necessity. Nepal has long required stronger enforcement against corruption, illicit wealth accumulation and financial crime. Powerful individuals who manipulate the economy should indeed face legal scrutiny.

The problem lies elsewhere. The campaign’s increasingly aggressive style has blurred the distinction between the genuinely corrupt and those merely operating within an atmosphere of heightened suspicion.

Prominent businessmen- including Devi Bhattachan, Om Prasad Pandey, Sulav Agrawal, Deepak Bhatt and former Federation of Nepalese Chambers of Commerce and Industry president Shekhar Golchha among dozens of businessmen found themselves under investigation or arrested, while several other high-profile entrepreneurs entered the orbit of law-enforcement agencies.

Financial markets responded almost immediately. The Nepal Stock Exchange (NEPSE), often viewed as a barometer of investor confidence rather than current economic conditions, fell sharply after the new government assumed office.

Three months after taking office, the Balen government’s stock market performance tells a starkly different story. The NEPSE index has fallen 301 points, from 2,950.16 to 2,649.76, while investors have lost around Rs 471 billion as market capitalisation dropped from Rs 5.009 trillion to Rs 4.534 trillion.

Trading trends point to a confidence crisis rather than a liquidity shortage, with investors still waiting for a clear economic roadmap, investment-friendly policies, and stronger support for the capital market. The sell-off intensified after the national budget, with almost all sectoral indices declining except manufacturing. Stock markets measure expectations, not history. When investors lose confidence in tomorrow, prices fall today.

Among entrepreneurs-particularly those whose wealth was built through capital markets-a lingering fear has emerged: not simply whether regulations will tighten, but whether legal action may become increasingly unpredictable.

That fear does not remain confined to wealthy investors. It spreads throughout the economy, discouraging investment, delaying business decisions and weakening overall economic momentum.

The numbers justify the anxiety

Business pessimism is not merely emotional.

Nepal’s own official statistics suggest the economy remains considerably weaker than political rhetoric implies.

According to preliminary estimates from the National Statistics Office, Nepal’s economy is expected to reach approximately Rs 6.6 trillion during fiscal year 2025/26, with real GDP growth of 3.85%.

At first glance, this appears respectable. It is not. The government had originally targeted 6% growth.

Missing nearly one-third of an annual growth target represents more than statistical disappointment. It illustrates the widening gap between political ambition and economic reality.

The World Bank has warned that when both the September unrest and heightened geopolitical tensions in the West Asia are incorporated into forecasts, Nepal’s growth could slow to as little as 2.3%. During the first half of the fiscal year, actual growth was only 3.4%.

Sectoral performance tells an equally uneven story. Electricity generation expanded by roughly 21%, driven largely by hydropower.

Agriculture-the sector that still contributes roughly one-quarter of GDP-grew by only 3.4%, weakened by drought across Madhesh and untimely flooding during October 2025 that severely reduced rice production.

Construction, meanwhile, remains sluggish. Declining imports of construction materials indicate that infrastructure activity has failed to regain momentum.

Plenty of money. Very little confidence. Perhaps the clearest contradiction within Nepal’s economy appears inside its banking system.

Commercial banks are awash with liquidity. Deposits have reached nearly Rs 7.95 trillion, representing annual growth of around 16%.

Borrowing costs have fallen substantially. Average commercial lending rates have declined from 8.11% to 6.73%. Base rates have dropped below 5%. Even 91-day Treasury bill yields have fallen to approximately 2.63%.

Normally, such conditions would trigger rapid private investment. Instead, private-sector lending has increased by only 5.7%, slower than the previous year.

Economists describe this phenomenon as a capital trap.

Money exists.

Credit is cheap.

Banks are eager to lend.

But entrepreneurs are unwilling to borrow.

The central bank has even been forced to absorb excess liquidity from commercial banks because so much idle cash has accumulated within the financial system—a highly unusual situation.

Meanwhile, banks face another challenge.

By mid-April 2026, non-performing loans had climbed to 5.6%.

Higher bad loans require banks to allocate larger provisions against future losses, reducing both profitability and lending capacity.

In other words, confidence has weakened on both sides of the balance sheet.

Businesses hesitate to borrow.

Banks hesitate to lend.

An economy supported from abroad

Nepal’s external accounts continue to appear remarkably healthy.

Remittance inflows rose by 41.2%, reaching approximately Rs 1.92 trillion within ten months.

Foreign exchange reserves climbed to Rs 3.7 trillion (roughly $24.2 billion), sufficient to finance more than 19 months of imports.

At first glance, these figures suggest resilience. They also conceal a structural weakness.

Exports totalled only Rs 249 billion, while imports reached almost Rs 1.69 trillion, leaving Nepal with a trade deficit exceeding Rs 1.44 trillion.

The export-import ratio stands at just 14.7%. Nepal purchases nearly seven times more from the world than it sells.

Its external stability therefore rests not upon industrial competitiveness or export strength but upon remittances sent home by workers abroad.

This foundation is inherently fragile. Recent increases in global Brent crude prices—up to around $111 per barrel-will inevitably increase Nepal’s import bill, raise transportation and production costs, fuel inflation and further weaken household purchasing power.

The government’s credibility problem

The government’s own spending behaviour further undermines confidence.

By June 2026, only Rs 142 billion in capital expenditure had been executed-less than 35% of the annual development budget. During the same period the previous year, capital spending exceeded 44%.

This matters enormously. Capital expenditure creates tomorrow’s employment. When governments fail to build roads, transmission lines, industrial infrastructure and public investment projects, they simultaneously reduce demand for private-sector activity.

Expecting businesses to drive growth while the state itself fails to spend its investment budget resembles asking an undernourished patient to carry heavy loads. The contradiction is difficult to ignore.

Confidence is economic policy

Nepal’s private sector provides approximately 86% of national employment.

Its confidence therefore affects not merely corporate profits but millions of livelihoods.

Recognising growing anxiety, RSP chairman Rabi Lamichhane recently reassured business leaders that they had “no reason to fear.”

The reassurance itself was revealing. Governments rarely attempt to calm fears that do not exist.

Meanwhile, ministers continue announcing ambitious initiatives-from cross-border economic integration and hydropower exports to IT parks, startup programmes and industrial villages. Finance Minister Swarnim Wagle has correctly argued that Nepal cannot realistically aspire to become a $100-billion economy without the private sector.

The diagnosis is accurate.

The operating environment is not.

Vision and direction are different things.

Vision imagines the destination.

Direction determines whether anyone actually arrives.

Today, capital expenditure remains weak. Banks remain burdened by rising non-performing loans. Investment decisions are postponed. Business confidence remains clouded by uncertainty.

The economy needs trust more than slogans

Nepal’s economy increasingly resembles a house supported by two different foundations.

The external sector appears remarkably strong. Foreign reserves remain abundant. Remittances continue flowing. The current account remains comfortable.

Inside the country, however, the foundations are far less secure.

Private investment is slowing.

Credit demand remains weak.

Development spending has stalled.

Confidence has deteriorated.

A government armed with an overwhelming electoral mandate possesses a rare opportunity to reshape history. But electoral strength alone does not produce economic growth. Power must be accompanied by restraint, predictability and institutional wisdom.

Governments should unquestionably prosecute corruption. But they must also distinguish between enforcing the law and creating an atmosphere in which legitimate enterprise fears becoming collateral damage.

Nepal today appears caught in a classic capital trap-not because money has disappeared, but because confidence has.

Ultimately, confidence is itself economic policy.

The day Nepal’s entrepreneurs once again feel free to build factories instead of worrying about investigations, to purchase machinery instead of postponing investment, and to take commercial risks instead of political ones, the economy will require far fewer government slogans.

It will begin growing on its own.