Kathmandu

Wednesday, July 8, 2026

The central bank's new monetary policy, unveiled on July 7, 2026, leaves the policy rate at 4.25 percent and projects inflation around 5.5 percent, even as a subdued credit market, a depreciating rupee, and risks from the West Asia conflict cloud the outlook

KATHMANDU: Nepal Rastra Bank (NRB) announced its monetary policy for fiscal year 2026/27 on July 7, 2026, alongside a companion Macroeconomic Report prepared by its Economic Research Department.

Governor Biswo Nath Poudel presented the policy as a continuation of the “cautiously flexible” stance NRB has followed in recent years, keeping borrowing costs low while backing the government’s ambitious 7 percent growth target for the year ahead.

What exactly did Nepal Rastra Bank announce on July 7, 2026, and how is this year’s process different from before?

Nepal Rastra Bank unveiled its twenty-fifth annual monetary policy on July 7, 2026, setting out the stance, structure, and instruments it intends to use through the fiscal year ending in mid-July 2027. What sets this year apart is a structural change in how NRB communicates its thinking. Under Section 94 of the Nepal Rastra Bank Act, 2002, the central bank is required to review the previous year’s policy and justify its plans for the year ahead.

Rather than folding all of this review and justification into the monetary policy document itself, NRB has now split the exercise into two separate publications: a slim monetary policy statement carrying the actual decisions, and a much longer Macroeconomic Report, titled “Macroeconomic Report: Analysis and Outlook, July 2026,” that lays out the detailed economic backdrop, data, and forecasts behind those decisions.

NRB says this new structure is meant to make both documents more transparent and easier to scrutinize, since the analytical justification is no longer buried inside the policy text. Governor Poudel, who has led NRB through a soft-money approach, framed the split itself as evidence of a push toward more rigorous economic analysis backing the central bank’s policy choices.

What are the headline growth and inflation targets for fiscal year 2026/27, and are they realistic?

The monetary policy targets economic growth of about 7.0 percent and average consumer price inflation of around 5.5 percent for fiscal year 2026/27, alongside foreign exchange reserves sufficient to cover at least seven months of prospective imports of goods and services. These figures mirror the government’s own budget assumptions, which similarly assume 7 percent growth with inflation capped at 6 percent.

The Macroeconomic Report is candid that 7 percent would be well above Nepal’s recent trend and above its estimated potential growth rate of around 4.2 percent, meaning the economy would need to operate above its normal capacity to hit the target.

A photo collage of the monetary policy and Governor Biswo Nath Poudel

NRB and the government argue this is achievable only if several favorable conditions line up together: private investment keeps recovering, the government actually executes its capital budget rather than letting it lapse as in past years, global conditions (especially oil prices linked to the West Asia conflict) stabilize, and investor confidence continues to firm up following the political transition after the September 2025 Gen Z movement and the subsequent March 2026 election.

Independent commentary, including from the World Bank’s South Asia teams, has generally treated Nepal’s growth estimates as running below such targets in recent years, so 7 percent should be read as an aspirational, reform-dependent ceiling rather than a base-case certainty.

How fast did Nepal’s economy actually grow in 2025/26, the year that just ended, and what drove it?

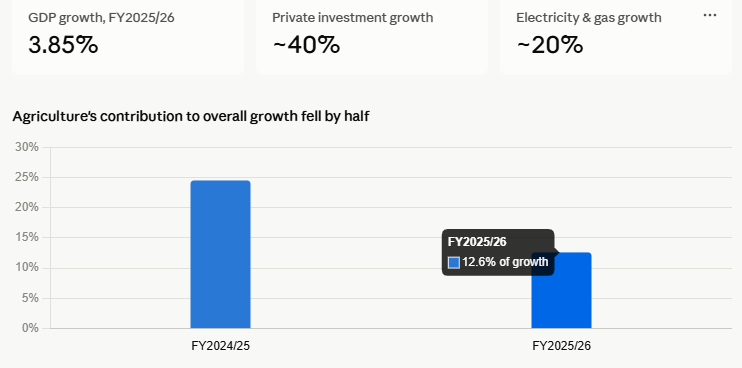

According to the National Statistics Office estimate cited in the Macroeconomic Report, Nepal’s economy expanded by an estimated 3.85 percent in fiscal year 2025/26, a modest moderation from the previous year. Growth was driven overwhelmingly by the service sector, which contributed the largest share of overall output growth, followed by industry and then agriculture.

Within industries, wholesale and retail trade, financial and insurance services, and electricity and gas were the standout performers, with the electricity and gas subsector alone expected to expand by around 20 percent on the back of new generation capacity and better transmission.

Agriculture’s contribution nearly halved compared to the year before, falling to about 12.6 percent of overall growth from roughly 24.5 percent, largely because of drought during paddy planting and unseasonal rainfall at harvest time.

On the demand side, private consumption remained the largest driver of GDP even as its share gradually declined, while private investment staged a sharp rebound, growing close to 40 percent for the year as improved security conditions and confidence in the newly elected majority government encouraged businesses to resume capital spending that had stalled during the political unrest of late 2025.

Why did inflation rise through the second half of 2025/26 after falling to multi-year lows, and where is it headed?

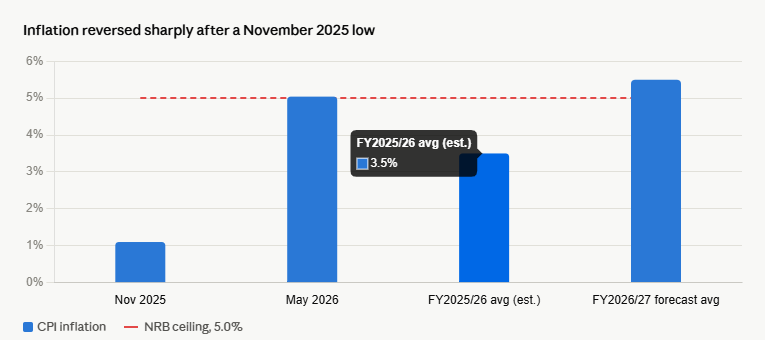

Consumer price inflation fell to a low of about 1.1 percent in November 2025 before reversing sharply, climbing to 5.04 percent by May 2026. The Macroeconomic Report attributes this turnaround mainly to petroleum and food prices. Global crude oil prices spiked after the escalation of the Israel-US conflict with Iran in early 2026, when the closure of the Strait of Hormuz briefly pushed crude above USD 100 a barrel; Nepal Oil Corporation passed these costs through to domestic pump prices quickly, which fed directly into transport costs and, from there, into the price of almost everything transported by road.

Food prices added further pressure once a period of deflation in food and beverages ended around March 2026, with fruits, ghee, cooking oil, and vegetables showing particularly sharp increases. For the year just ending, average inflation is expected to stay below 3.5 percent, comfortably inside NRB’s 5.0 percent ceiling, but the central bank’s own forecast for 2026/27 puts average inflation around 5.5 percent, with quarterly figures hovering between 5.3 and 5.6 percent.

Some of this expected relief stems from the diplomatic breakthrough between the United States and Iran, which by July 2026 had already restored a large volume of oil shipping through the Strait of Hormuz and pulled crude prices back down from their war-time peak.

Nepal’s banking system is sitting on unusually high liquidity, yet lending has barely grown. Why is credit not flowing despite cheap money?

This puzzle is explicitly flagged in the Macroeconomic Report as a “credit conundrum.” Excess reserves in the banking system stood at roughly Rs 1.1 trillion by mid-May 2026, and the weighted average lending rate had fallen to just 6.7 percent, historically low levels that would normally be expected to unleash a wave of borrowing.

Instead, private sector credit growth came in at around 6 percent for the year, well short of the 12 percent NRB had originally projected in its 2025/26 monetary policy. NRB’s analysis points to four specific constraints operating simultaneously rather than a single cause.

First, capital adequacy requirements still bind for a majority of banks and financial institutions, limiting how much more they can lend regardless of available cash. Second, the credit-to-deposit ratio is a binding constraint for some institutions, even if not most.

Third, declining asset quality, driven by rising non-performing loans, forces banks into more cautious underwriting even when they have surplus deposits to place. Fourth, the September 2025 political unrest and a stagnant real estate market, which underpins the majority of bank collateral, have made both borrowers and lenders more hesitant.

NRB expects credit growth to rebuild toward roughly 11 percent in 2026/27 as these strains gradually ease.

What did NRB actually decide about interest rates and other core monetary settings for the year ahead?

NRB left its key policy rates unchanged for 2026/27. The policy rate remains at 4.25 percent, the standing deposit facility (the floor of the interest rate corridor) stays at 2.75 percent, and the bank rate, or standing liquidity facility rate at the top of the corridor, remains at 5.75 percent.

The cash reserve ratio, statutory liquidity ratio, and standing liquidity facility arrangements were likewise kept unchanged, signaling continuity rather than any fresh tightening or easing move. The weighted average interbank rate, which NRB uses as its operating target, has largely tracked the floor of this corridor over the past year, evidence that the transmission of the policy rate into short-term market rates is working reasonably well, even if the pass-through into longer-term bank lending rates remains partial, as is typical in developing economies with immature financial markets.

NRB also reaffirmed its intention to keep managing liquidity through a mix of instruments, including the standing deposit facility, deposit collection auctions, and NRB bonds, while continuing to encourage commercial banks to invest surplus dollars in foreign government securities and to use sterilized intervention when purchasing foreign currency, so that dollar purchases do not mechanically flood the domestic market with fresh rupee liquidity.

Nepal’s foreign exchange reserves are reportedly at record levels. How large are they, and how comfortable is the country’s external buffer really?

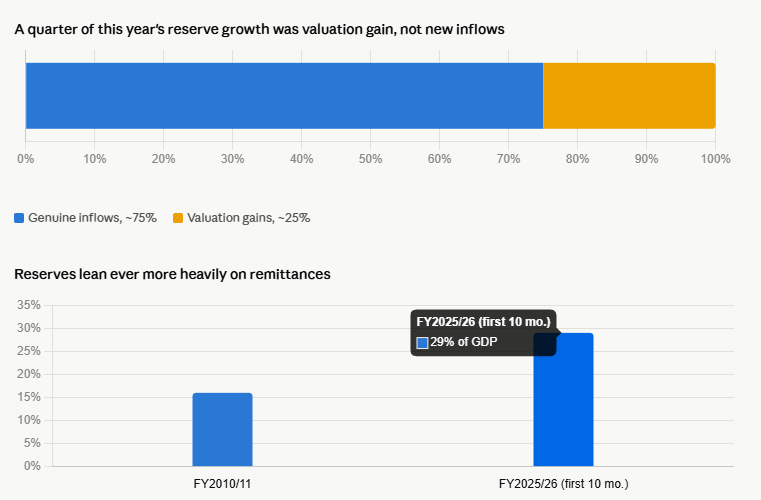

Gross foreign exchange reserves stood at Rs 3,704.5 billion, equivalent to about USD 24.19 billion, as of mid-May 2026, sufficient to cover a record 19.1 months of prospective imports of goods and services, far above the traditional benchmark of three months typically used to judge reserve adequacy for import-dependent economies.

Reserves grew by over 40 percent in rupee terms and 33 percent in dollar terms over the review year. However, the Macroeconomic Report itself cautions that this headline strength deserves scrutiny. About a quarter of the increase came not from genuine inflows but from valuation gains created purely by the depreciation of the Nepali rupee against the US dollar, meaning existing dollar-denominated reserves became worth more in rupee terms without any new dollars actually entering the country.

More fundamentally, Nepal’s reserve buoyancy rests overwhelmingly on remittances, which have grown from around 16 percent of GDP in 2010/11 to nearly 29 percent of GDP in the first ten months of 2025/26, dwarfing what the country earns from exports or tourism. NRB itself describes this as a structural imbalance that needs to be corrected over time through stronger exports and tourism earnings, not treated as a permanent cushion.

Why has the Nepali rupee been depreciating against the US dollar, and what does that mean for ordinary Nepalis?

The Nepali rupee depreciated by about 10.5 percent against the US dollar between mid-July 2025 and the review period in 2026, a decline that traces back almost entirely to Nepal’s fixed exchange rate peg to the Indian rupee (currently held at Rs 1.60 per Indian rupee) rather than to any weakness specific to Nepal’s own economy.

The Indian rupee itself slid by close to 6 percent against the US dollar between January and May 2026, a move that independent commentary has linked to capital flowing out of India and other emerging markets toward US assets amid the artificial-intelligence-driven boom in American equity markets, compounded by punitive American tariffs on South Asian exports.

As Nepal’s currency is mechanically tied to India’s, that Indian weakness was imported wholesale into the Nepali exchange rate. For everyday Nepalis, a weaker rupee against the dollar makes imported fuel, machinery, and other dollar-priced goods costlier, feeding directly into the inflation described earlier.

On the positive side, the Macroeconomic Report notes that Nepal’s real effective exchange rate, which adjusts for relative inflation and trade-weighted currency movements, actually depreciated even more than the nominal rate, which in principle makes Nepali goods and services somewhat more price-competitive in international markets, even though Nepal’s narrow export base limits how much it can capitalize on that.

How healthy are Nepal’s banks and financial institutions right now, and should depositors be worried?

The Macroeconomic Report describes the overall financial system as broadly stable but flags specific and growing pressure points. The gross non-performing loan ratio across banks and financial institutions reached 5.6 percent by April 2026, and for commercial banks specifically it has climbed from just 1.81 percent in the third quarter of 2016 to 5.41 percent a decade later, a significant deterioration over that period.

Average net non-performing loans, after accounting for provisioning, remain more contained at under 1.5 percent, and NRB describes this as still within manageable limits. What worries NRB more is the trajectory: loans classified under the “watchlist” category, meaning loans showing early signs of stress but not yet formally non-performing, rose from 6.7 percent of the portfolio in mid-July 2023 to 11.1 percent by mid-April 2026, suggesting today’s manageable NPL figures could deteriorate further if economic conditions do not improve.

Average net non-performing loans, after accounting for provisioning, remain more contained at under 1.5 percent, and NRB describes this as still within manageable limits.

A large part of the problem traces back to a real estate boom and its subsequent correction; roughly three-fifths of all bank loans are secured against land and buildings, and with the real estate market now stagnant, banks are finding it difficult to liquidate collateral to recover stressed loans.

NRB’s response is to push banks toward project-based and character-based lending, supported by a more institutionalized individual credit-scoring system, so that future lending relies less exclusively on real estate collateral.

What structural or regulatory reforms is NRB introducing this year for the banking sector itself?

Beyond interest rates, this year’s monetary policy contains a set of institutional reforms aimed at making banks more efficient and better supervised. NRB plans to complete an ongoing study on reclassifying banks and financial institutions so that different categories of institutions, and even non-bank financial institutions, can be encouraged to expand into specific underserved market segments rather than all competing in the same space.

The central bank also intends to simplify and consolidate the web of directives it issues to banks, starting in the first phase with directives covering credit flow, interest rates, and financial consumer protection, in order to reduce linguistic complexity and duplication across different circulars.

On the consumer protection side, NRB wants to end the practice of unlimited personal liability arising from personal guarantees on loans, ease the blacklisting consequences that follow a single bounced cheque so that people are not permanently locked out of banking services over one incident, and set clearer rules for restructuring loans extended to distressed industries.

NRB also plans to study how peer-to-peer lending platforms built on individual credit scoring could be regulated, and will continue consolidating bank branches in areas where digital banking has reduced the need for physical outlets, a process that had already removed 160 branches by mid-May 2026 without materially harming access to financial services.

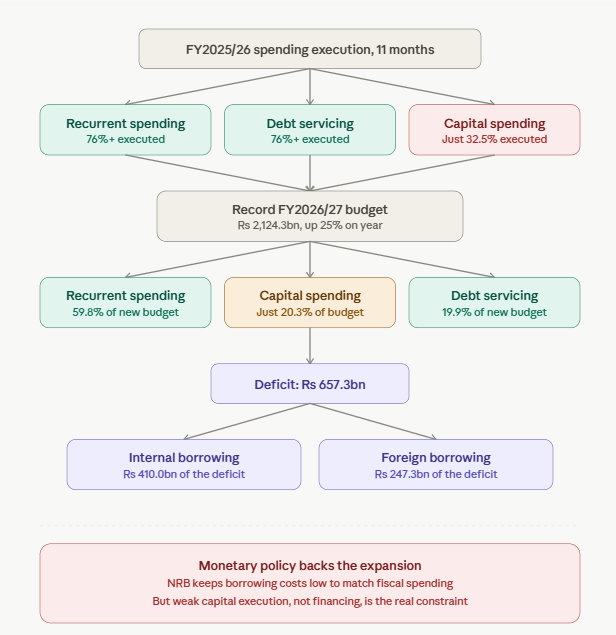

What does Nepal’s fiscal position look like, and how does the record Rs 2,124.3 billion budget for 2026/27 fit into the monetary policy picture?

Government finances continued to underperform through the first eleven months of fiscal year 2025/26: total expenditure reached only 68.6 percent of the annual budget target, and capital spending, the money meant to build roads, irrigation, and other productive infrastructure, executed at just 32.5 percent of its target, continuing a long-standing pattern in which Nepal is better at allocating budgets than at actually spending them.

Recurrent expenditure and debt servicing, by contrast, both executed at well over 75 percent of their allocations. Against this backdrop, the government tabled its largest-ever budget for 2026/27 at Rs 2,124.3 billion, about 25 percent larger than the prior year’s revised estimate. Of this, 59.8 percent is recurrent spending, 20.3 percent is capital spending, and 19.9 percent goes toward debt servicing and other financial management.

The budget doubles the personal income tax exemption threshold from Rs 500,000 to Rs 1 million and cuts the top marginal tax rate from 39 to 29 percent, moves designed to boost disposable income and consumption. The resulting deficit of about Rs 657.3 billion is to be financed through a combination of internal borrowing (Rs 410.0 billion) and foreign borrowing (Rs 247.3 billion).

NRB’s monetary policy is explicitly designed to complement this expansionary fiscal stance by keeping borrowing costs low, though the central bank’s own Macroeconomic Report warns that Nepal’s chronic weakness in executing capital budgets, not a shortage of financing, remains the binding constraint on turning this spending into growth.

Total public debt has been rising steadily. How much does Nepal now owe, and is this level considered sustainable?

Nepal’s total outstanding public debt rose from about Rs 2,010 billion in 2021/22 to Rs 2,961.2 billion, by the end of the first eleven months of 2025/26, a cumulative increase of around 48 percent over four years. As a share of GDP, total public debt climbed from 40.4 percent to 44.9 percent over the same period, with internal debt holding broadly steady around 20 to 21 percent of GDP while external debt rose more noticeably, from about 20.6 to 24.0 percent of GDP.

A joint debt sustainability analysis conducted by the World Bank and the International Monetary Fund still classifies Nepal’s public debt as low risk of distress, but the Macroeconomic Report notes that Nepal’s own composite risk indicator score in these assessments has been gradually deteriorating since 2020.

The more pressing concern the report raises is not the debt level itself but how the borrowed money is being used: with only about a third of the capital budget executed in the review period, a large share of new borrowing effectively goes toward financing recurrent government spending and servicing existing debt rather than building the roads, irrigation, and energy infrastructure that would expand the economy’s future capacity to repay that debt.

How exactly is the war between Israel, the United States, and Iran connected to Nepal’s inflation and reserve numbers?

The connection runs through oil markets and remittances. West Asia supplies roughly a fifth of the world’s oil and much of it transits the Strait of Hormuz, so when Israel and the United States struck Iran on February 28, 2026, killing its Supreme Leader and prompting Iran to close the strait in retaliation, global crude prices spiked past USD 100 a barrel and diesel prices rose disproportionately because many diesel refineries sit in West Asian countries.

Nepal Oil Corporation passed these costs through domestically almost immediately, which is the primary reason Nepal’s inflation diverged from India’s inflation trend starting in April and May 2026, since India kept its own domestic fuel prices comparatively stable despite the same global price shock. At the same time, around 41 percent of Nepal’s total remittance inflow originates from workers in the West Asia region, so the conflict also threatened one of Nepal’s most important sources of foreign currency.

In practice, remittances kept growing regardless, up 41.2 percent for the review year, suggesting labor markets in destination countries stayed resilient even amid the fighting. The United States and Iran signed a memorandum of understanding on June 17, 2026, that reopened the Strait of Hormuz and set up a sixty-day negotiating window; Iran has since exported more than 40 million barrels of crude, and oil prices have eased back from their wartime peak, which underpins NRB’s relatively benign inflation forecast for 2026/27 despite the recent price shock.

What is the Interest Rate Corridor, and why does NRB keep referring to it as the anchor of its monetary policy?

The Interest Rate Corridor, introduced by NRB in July 2017 when it shifted from a quantity-targeting approach to an interest-rate-targeting regime, consists of three rates: the policy repo rate in the middle, the standing deposit facility rate as the floor, and the bank rate, or standing liquidity facility rate, as the ceiling.

The weighted average interbank rate, the actual overnight rate banks charge each other, is supposed to stay within this band, and NRB has managed to keep it close to the corridor floor for most of the past two years, indicating that its short-term liquidity operations are functioning as intended.

The importance of the corridor lies in what economists call interest rate pass-through: the process by which a change in the policy rate eventually shows up in the rates banks charge borrowers and pay depositors.

NRB’s own research estimates this pass-through in Nepal at about 0.5 percentage points, roughly in line with other developing economies and notably below the near-complete pass-through seen in advanced financial markets.

Term deposits, which make up about 38 percent of total deposits, are identified as the main source of friction, because banks cannot quickly reprice these fixed-term liabilities when the policy rate moves, which slows down how fast changes at the top filter through to the loans and deposits that households and businesses actually experience.

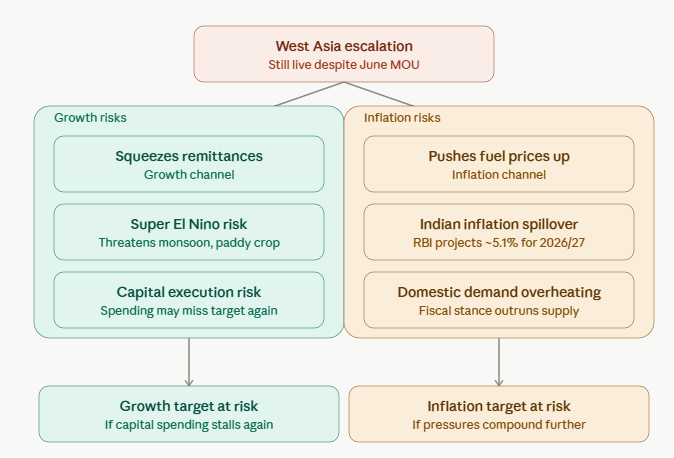

What are the biggest downside risks that could derail both the growth and inflation targets for 2026/27?

NRB’s own risk assessment, laid out in the Macroeconomic Report, centers on three main threats. First, renewed escalation in West Asia remains a live possibility even after the June 2026 memorandum of understanding between the United States and Iran, since the underlying disputes over the Strait of Hormuz’s governance and Iran’s nuclear program remain unresolved; any resumption of hostilities could simultaneously push fuel prices back up and squeeze remittance inflows from a region that supplies a large share of Nepal’s overseas workers.

Second, a forecast “super El Niño” weather pattern threatens to disrupt the monsoon cycle that Nepali agriculture depends on, potentially triggering droughts that would hit paddy production much as unfavorable weather already did in 2025/26.

Third, and perhaps most within Nepal’s own control, growth momentum depends heavily on whether the government can finally execute its capital budget at scale after years of persistent under-execution; if delayed project preparation, slow procurement, and weak institutional capacity persist as they have in past years, the current spending-led growth strategy will simply not deliver the intended boost to demand.

On the inflation side, additional risks include the possibility that Indian inflation, currently projected by the Reserve Bank of India at around 5.1 percent for 2026/27, comes in higher than expected and transmits across the open border, and that Nepal’s own accommodative fiscal stance overheats domestic demand faster than supply can respond.

Putting it all together, what is the overall assessment of Nepal’s economic outlook heading into fiscal year 2026/27?

NRB and its Economic Research Department describe the outlook as “moderately favorable” but conditional on several things going right simultaneously. Growth is expected to firm up from 3.85 percent in 2025/26 toward a level closer to, though likely still below, the government’s ambitious 7 percent target, supported by tax cuts that increase disposable income, a politically stable majority government restoring private investment confidence, and continued strength in remittances and services.

Inflation, after this year’s spike to just above 5 percent, is projected to average around 5.5 percent in 2026/27, kept from rising further by moderating global oil prices following the US-Iran de-escalation, even as an accommodative fiscal stance pushes in the opposite direction.

The external sector is expected to stay comfortable, with reserves remaining well above import-coverage benchmarks, though this comfort continues to rest on remittances rather than a genuinely diversified export base. Money supply is projected to grow by 14 percent and private sector credit by 11 percent, both a step up from this year’s sluggish pace, assuming banks’ non-performing loan pressures ease as economic activity picks up.

NRB’s own conclusion is that its “cautiously accommodative” policy stance, keeping money cheap and abundant while nudging structural reforms forward, remains appropriate for now, but the central bank has explicitly reserved the right to reverse course and tighten the interest rate corridor if inflation, financial stability, or external pressures move beyond what it currently expects.