Kathmandu

Monday, July 13, 2026

Commercial banks are posting record profits and holding more than Rs 1 trillion in excess liquidity, yet lending remains weak as bad loans climb, the economy slows, and structural challenges deepen

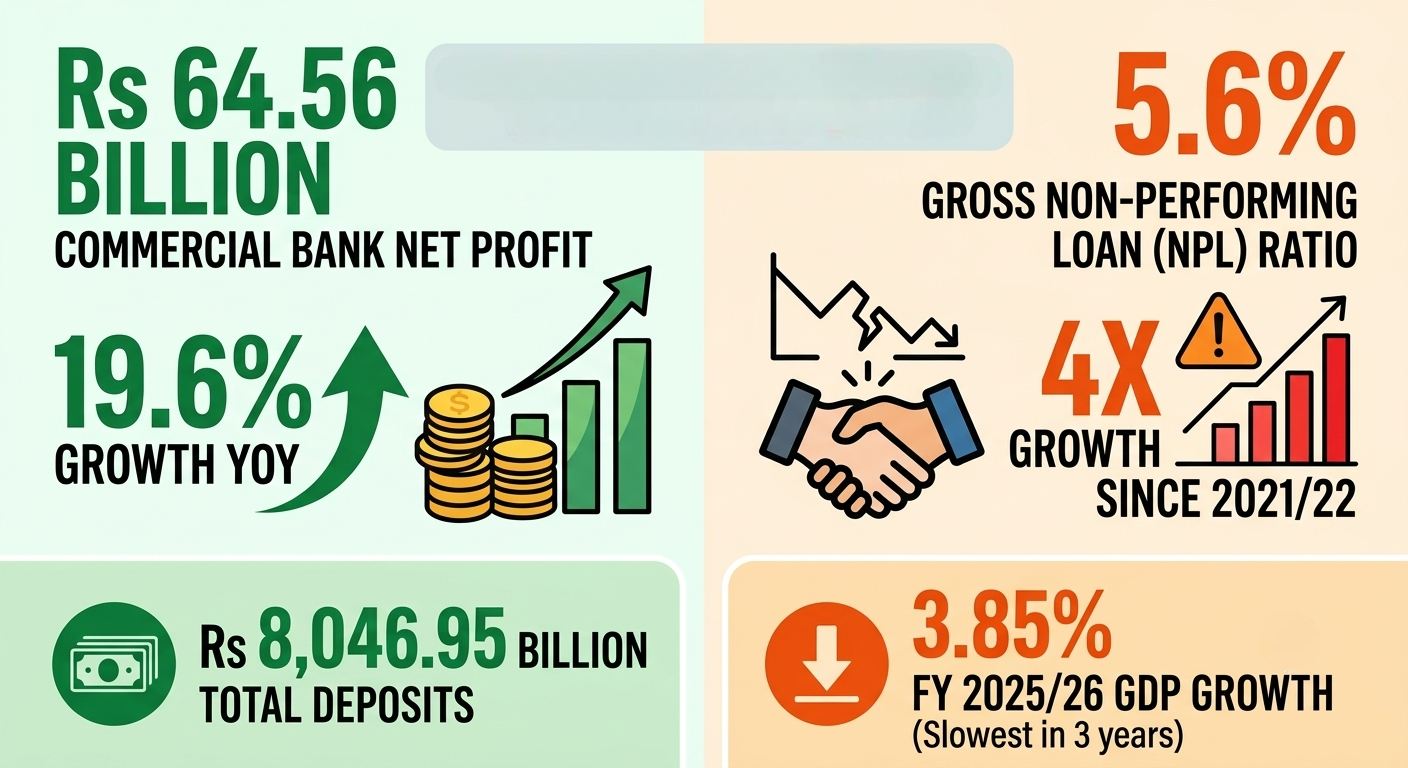

KATHMANDU: Nepal’s banking sector is about to enter the fiscal year 2026/27 carrying contradictory signals. Commercial banks have posted their strongest profit growth in years and are sitting on more than a trillion rupees of idle, lendable money, even as non-performing loans have more than quadrupled since 2021/22 and the broader economy grew just 3.85 percent, its slowest pace in three years, with a national resource gap that has nearly tripled in two years.

How large is Nepal’s banking sector today, in terms of assets, deposits, and credit?

According to Nepal Rastra Bank’s (NRB) own monthly banking and financial statistics for mid-June 2026, total deposits across all banks and financial institutions stood at Rs 8,046.95 billion, having grown from Rs 7,980.60 billion just a month earlier in mid-May. Total credit outstanding across the same institutions stood at Rs 5,918.03 billion.

Commercial banks alone, the 20 Class A institutions that dominate the sector, held total assets of Rs 9,082.36 billion, deposits of Rs 7,261.75 billion, and loans and advances of Rs 5,262.45 billion as of the same date, figures that are meaningfully higher than the Rs 7,756.23 billion in total assets recorded at the close of fiscal year 2024/25, reflecting continued growth through the year even as lending growth itself has been sluggish.

Total deposits across the system stood at 131.76 percent of GDP and total credit at 96.92 percent of GDP as of mid-June 2026, according to Nepal Rastra Bank’s own ratio calculations, underscoring how deeply the banking sector’s balance sheet now exceeds the size of the real economy it serves.

Nepal Rastra Bank office in Thapathali. Photo: Bikram Rai/Nepal News

The gap between roughly Rs 8.05 trillion in deposits and Rs 5.92 trillion in credit remains the single most important number for understanding the sector, representing money collected from savers that has not yet found its way into loans.

How much profit did commercial banks earn this fiscal year, and how does that compare with last year?

Nepal’s 20 commercial banks posted a combined net profit of Rs 64.56 billion through the 11 months (from mid-July 2025 to mid-June 2026), based on Nepal Rastra Bank’s own profit and loss statements for the sector. This is a 19.62 percent increase, or Rs 10.59 billion more, compared with the Rs 53.97 billion the same 20 banks earned during the same 11-month window a year earlier.

Fourteen of the 20 banks recorded higher profits this year while six reported declines. Bankers attribute the improvement mainly to better recovery of previously unpaid loans, a falling cost of funds as deposit interest rates have declined toward a weighted average of just 3.29 percent by mid-June 2026, and reduced operating costs across the industry.

This profit growth needs to be read against a broader economy that itself slowed: the National Statistics Office’s preliminary estimate puts fiscal year 2025/26 GDP growth at 3.85 percent, down from a revised 4.43 percent in 2024/25, meaning bank profits accelerated even as the real economy they serve decelerated, a divergence that traces back to funding costs falling faster than lending income rather than to any broad-based expansion in productive credit.

Which banks earned the most profit, and which earned the least or saw the sharpest declines?

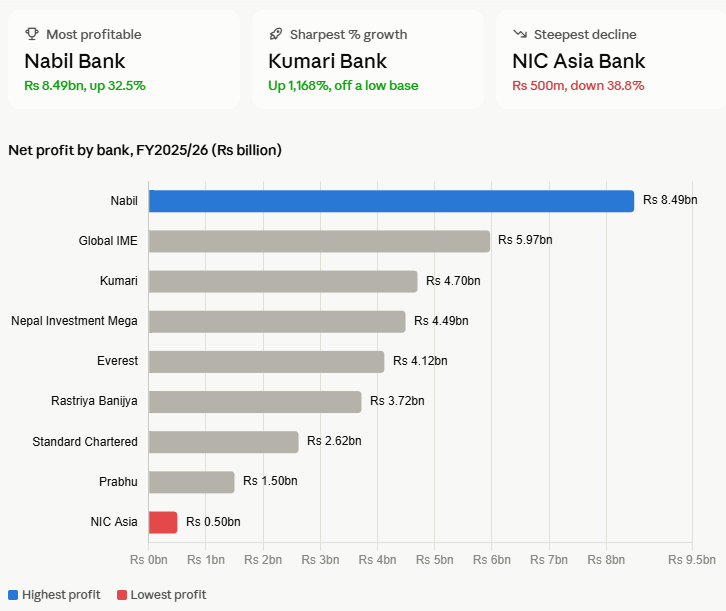

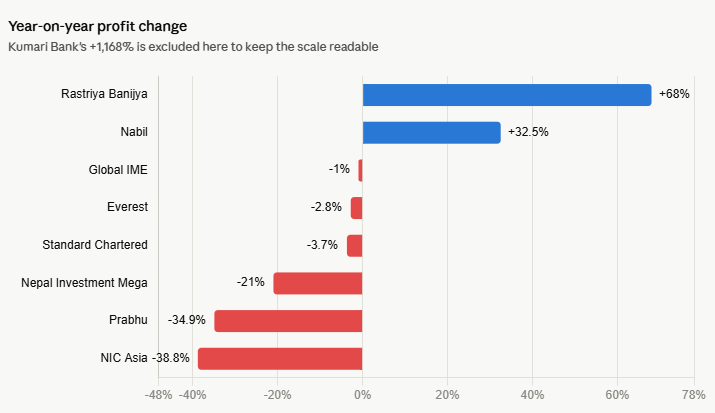

Nabil Bank remained Nepal’s most profitable commercial lender through mid-June 2026, with net profit of Rs 8.49 billion, up 32.51 percent from the prior year. Global IME Bank held the second position with Rs 5.97 billion, a marginal 0.96 percent decline. Kumari Bank recorded the sharpest percentage growth in the sector, with net profit surging to Rs 4.70 billion from just Rs 371 million a year earlier, an increase of 1,168 percent, driven mainly by improved loan recovery against a very low prior-year base.

Nepal Investment Mega Bank posted Rs 4.49 billion, a 21 percent decline, and Everest Bank posted Rs 4.12 billion, down 2.76 percent. Rastriya Banijya Bank, a state-owned lender, grew profit 68 percent to Rs 3.72 billion. At the other end, NIC Asia Bank recorded the steepest decline in the sector, with profit falling 38.81 percent to just Rs 500 million, the lowest absolute profit among all 20 commercial banks, a decline directly connected to its unusually heavy loan loss provisioning burden, which Nepal Rastra Bank data placed at Rs 22.35 billion against loans classified as non-performing.

Prabhu Bank’s profit fell 34.91 percent to Rs 1.50 billion. Standard Chartered Bank Nepal slipped 3.74 percent to Rs 2.62 billion. The divergence between banks like Nabil and Kumari, which grew strongly, and banks like NIC Asia and Prabhu, which saw earnings fall by a third or more, tracks closely with differences in loan book quality and provisioning burden across the industry.

What exactly is a non-performing loan, and how does Nepal Rastra Bank classify bad loans?

Under Nepal Rastra Bank’s regulatory framework, a loan is classified as non-performing once scheduled repayment has not been received for three months or more. Nepal’s loan classification system divides credit into five categories based on how overdue repayment is. Loans within 30 days of being overdue are classified as good or pass loans. Those overdue between 31 and 90 days fall into a watchlist category, a distinct classification that sits just below formal non-performing status and functions as an early warning signal.

Loans overdue from 91 to 180 days are termed substandard, those overdue from 181 days to a year are doubtful, and any loan overdue for more than a year is classified as loss, meaning it is considered highly unlikely to ever be recovered. Against each category, banks must set aside loan loss provisions from their profits as a financial cushion, with required provisioning rising sharply as loans deteriorate: roughly 1.1 percent for pass loans, 5 percent for watchlist loans, 25 percent for substandard loans, 50 percent for doubtful loans, and a full 100 percent for loss loans.

As a bank’s loan book worsens, an increasingly large share of its capital gets locked away as a buffer rather than being available for fresh lending or profit distribution, which is precisely the mechanism through which rising bad loans squeeze bank earnings and credit capacity simultaneously.

What is the current non-performing loan ratio for Nepal’s banking sector, and how has it changed over time?

The most recent official figure, drawn from Nepal Rastra Bank’s July 2026 Macroeconomic Report, puts the gross non-performing loan ratio across all banks and financial institutions at 5.6 percent as of April 2026, with commercial banks specifically at 5.41 percent. This represents a climb from just 1.81 percent a decade earlier, in the third quarter of fiscal year 2016/17.

Nepal’s fiscal third quarter ends at mid-April and this April 2026 reading remains the newest non-performing loan figure Nepal Rastra Bank has published as of mid-July 2026, since the central bank’s detailed loan-classification data structurally lags its monthly balance-sheet releases by roughly two months. Two additional details matter for judging how serious this is.

First, average net non-performing loans, meaning the gross figure after subtracting specific provisions banks have already set aside, remain more contained at under 1.5 percent, which Nepal Rastra Bank itself describes as still within manageable limits.

Second, and more concerning for the trajectory ahead, loans classified under the watchlist category, meaning loans showing early signs of stress but not yet formally non-performing, rose from 6.7 percent of the total loan portfolio in mid-July 2023 to 11.1 percent by mid-April 2026, a leading indicator suggesting today’s headline non-performing loan figures could deteriorate further before they improve.

In absolute rupee terms, total non-performing loans held by commercial banks reached Rs 220.33 billion in fiscal year 2024/25 alone, a 22.40 percent jump from Rs 180.01 billion the year before, with private banks driving 26.31 percent of that increase against a comparatively modest 1.48 percent rise among state-owned banks.

Which individual banks currently carry the highest and lowest non-performing loan ratios?

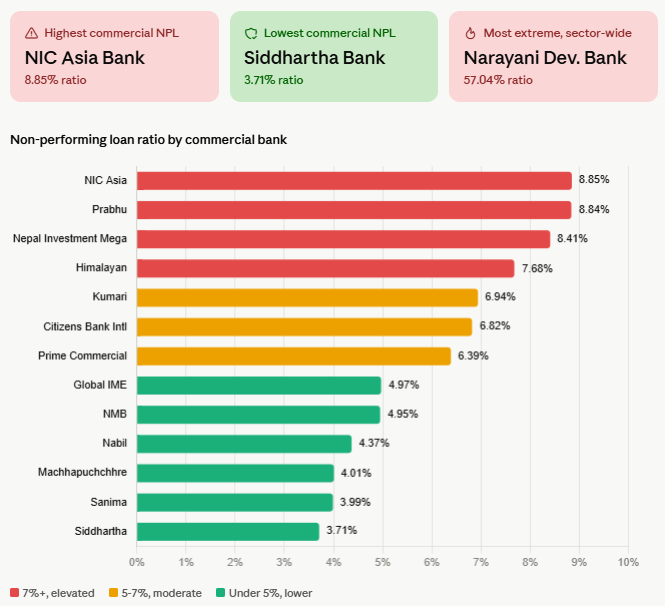

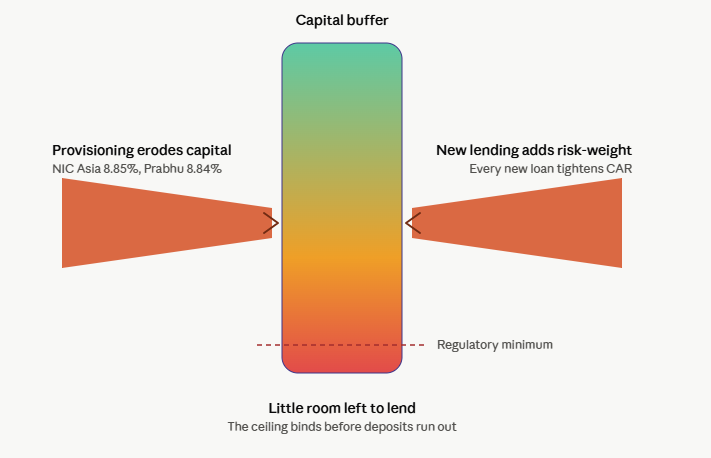

According to Nepal Rastra Bank data, NIC Asia Bank carried the highest non-performing loan ratio among the 20 commercial banks at 8.85 percent, with loan loss provisioning of Rs 22.32 billion. Prabhu Bank followed closely at 8.84 percent with Rs 22.84 billion in provisioning, and Nepal Investment Mega Bank stood at 8.41 percent with the sector’s largest absolute provisioning figure at Rs 28.45 billion.

Himalayan Bank recorded a 7.68 percent ratio with Rs 25.18 billion in provisions, and Kumari Bank stood at 6.94 percent with Rs 28.20 billion. Citizens Bank International’s ratio was 6.82 percent, and Prime Commercial Bank’s was 6.39 percent. At the more conservative end, Nabil Bank held a 4.37 percent ratio, Siddhartha Bank stood at 3.71 percent, and Sanima Bank at 3.99 percent, among the lowest in the sector.

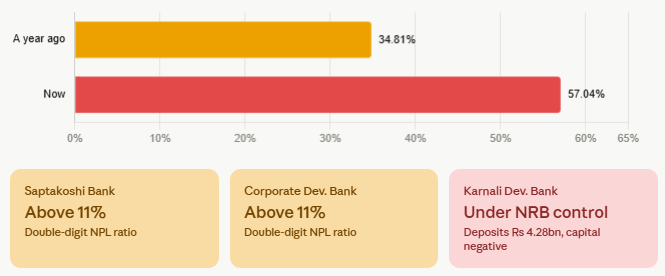

Machhapuchchhre Bank recorded 4.01 percent, NMB Bank 4.95 percent, and Global IME Bank 4.97 percent. Development banks, a separate and generally weaker regulatory tier, show far more extreme stress: Narayani Development Bank recorded a non-performing loan ratio of 57.04 percent, up sharply from 34.81 percent a year earlier, while Saptakoshi and Corporate Development Bank carried double-digit ratios above 11 percent, and Nepal Rastra Bank has already placed the troubled Karnali Development Bank under management control, a fact visible in Nepal Rastra Bank’s own mid-June 2026 balance sheet data, which shows Karnali’s deposit base collapsed to just Rs 4.28 billion against a capital fund that has turned negative.

Why exactly are non-performing loans increasing across Nepal’s banking sector?

Nepal Rastra Bank’s Bank Supervision Report for fiscal year 2024/25 attributes the rise in bad loans to a combination of macroeconomic disruption, sector-specific downturns, aggressive lending in earlier boom years, and outright weaknesses in corporate governance inside the banks themselves.

The report documents specific practices that inflated apparent loan quality while masking real risk: banks disbursing loans to firms with negative net tangible assets, financing borrowers beyond their approved drawing power, and accepting shares of financial institutions that themselves already carried non-performing loan ratios above 5 percent as collateral for margin lending.

Supervisors also documented loan rollover practices, in which fresh disbursements were made to the same borrowers near quarter-end specifically to close out overdue accounts, and restructuring exercises carried out without properly reassessing whether the underlying business remained viable.

A structural factor compounds all of this: roughly three-fifths of all bank loans in Nepal are secured against real estate collateral, and with the real estate market now stagnant following the correction that began around 2022 to 2023, banks are finding it increasingly difficult to actually liquidate that collateral to recover value from stressed loans, turning what should be a recoverable asset into a frozen one.

Beyond bank-level practices, the broader economy has simply generated more distressed borrowers: growth slowed to 3.85 percent in fiscal year 2025/26 from 4.43 percent the year before, and new business registration has fallen, with only 461 new businesses registered nationwide in the first six months of the fiscal year compared with 581 a year earlier, meaning fewer viable new borrowers are entering the credit pipeline to replace those failing.

How does Nepal Rastra Bank’s priority sector lending requirement connect to the rising bad loan problem?

Nepal Rastra Bank requires banks and financial institutions to direct a mandatory share of lending toward designated priority sectors, chiefly agriculture and micro, small, and medium enterprises, as a tool for expanding financial inclusion. Banking data and industry disclosures examined in mid-2026 show these very sectors have become disproportionately large sources of non-performing loans, undercutting that original goal.

Microfinance Bankers’ Association has said microfinance institutions alone have extended close to Rs 500 billion in loans, of which roughly 85 percent rely on group guarantees rather than physical collateral, meaning there is little to recover once a borrower defaults. Association officials argued the deterioration mainly reflects genuinely worsening rural economic conditions rather than deliberate default, noting that factories which once operated five or six days a week now run only two or three, directly cutting the incomes of households who took out these loans.

Officials at Nepal Finance Companies Association have separately argued banks apply a double standard, showing far greater flexibility toward large corporate borrowers facing repayment trouble while classifying smaller borrowers as non-performing more readily, and that the simultaneous crisis affecting savings and credit cooperatives has disrupted cash flow for thousands of small businesses that had been juggling borrowing across multiple cooperatives and microfinance institutions at once.

Although Nepal Rastra Bank’s prudential guidance generally expects sector-wide non-performing loans to stay below 5 percent, the central bank has so far avoided much stronger supervisory action, a restraint officials attribute partly to concern that tougher measures could deepen stress in an economy still working through a broader slowdown.

What is the current state of liquidity in Nepal’s banking system?

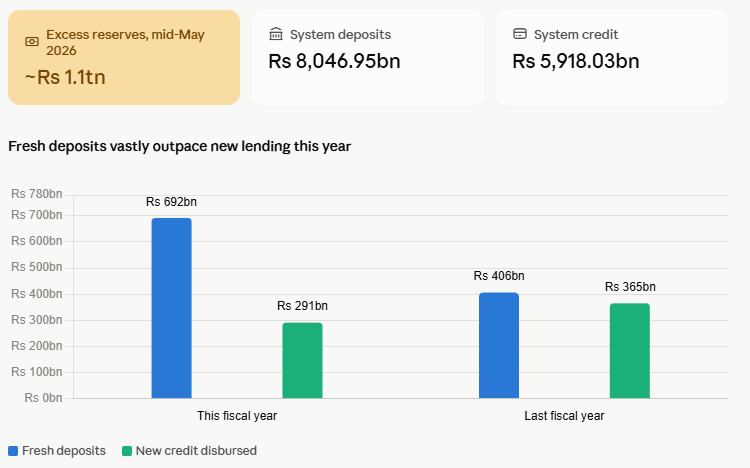

Nepal’s banking sector is carrying an unusually large volume of excess, unlent liquidity. Excess reserves stood at roughly Rs 1.1 trillion by mid-May 2026, according to Nepal Rastra Bank’s own Macroeconomic Report, and the gap between total system deposits of Rs 8,046.95 billion and total credit of Rs 5,918.03 billion as of mid-June 2026 confirms the surplus has persisted into the most recent data.

Up to May 24, 2026, commercial banks had collected Rs 692 billion in fresh deposits over the fiscal year but managed to disburse only Rs 291 billion in new credit, a stark contrast with the same period of the previous fiscal year, when banks collected Rs 406 billion in deposits and disbursed Rs 365 billion in loans, nearly matching deposit growth.

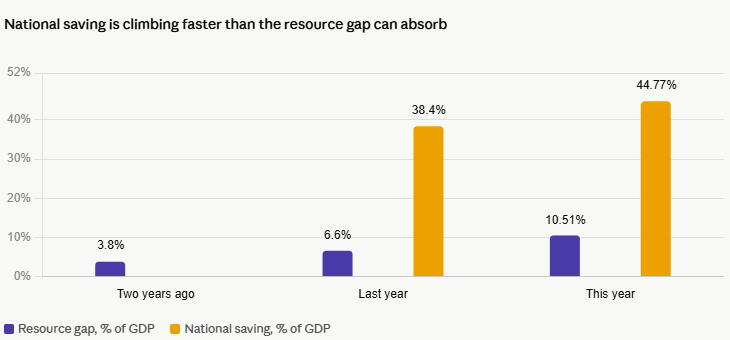

This liquidity glut connects directly to a separate but related national statistic: Nepal’s resource gap, meaning the difference between what the country invests domestically and what it saves, reached 10.51 percent of GDP in fiscal year 2025/26 according to the National Statistics Office, up sharply from 6.60 percent the year before and just 3.8 percent two years earlier, even as gross national saving, boosted heavily by remittances, climbed to 44.77 percent of GDP from 38.4 percent.

In plain terms, Nepal is saving an increasing share of its national income, much of that saving is landing in bank deposits, and a growing share of it is simply not being converted into productive domestic investment, whether through bank lending or direct capital formation.

One direct consequence for banks specifically is that they have increasingly been forced to lend surplus cash back to Nepal Rastra Bank at low rates through deposit collection auctions rather than earning normal interest margins from private borrowers, compressing potential interest income even as deposits keep piling up.

What is the credit-to-deposit ratio, and why does Nepal Rastra Bank watch it so closely?

The credit-to-deposit ratio, commonly called the CD ratio, measures what share of a bank’s total deposits has actually been lent out as credit. Nepal Rastra Bank permits banks and financial institutions to lend up to 90 percent of deposits under this ratio.

As of mid-June 2026, Nepal Rastra Bank’s own published ratio stood at 72.91 percent system-wide, with commercial banks alone at 71.83 percent, development banks at 84.31 percent, and finance companies at 76.87 percent. This represents a continued slide from 78.89 percent at the end of fiscal year 2023/24, 75.78 percent at the end of fiscal year 2024/25, and roughly 74.32 percent in March of the current fiscal year, confirming the multi-year downward trend has persisted through the most recent available data rather than reversing.

Individual institutions vary considerably: as of mid-2025 data, Citizens Bank International, NMB Bank, and Prime Commercial Bank operated with some of the highest CD ratios in the sector, near 83 to 84 percent, reflecting a more aggressive lending posture relative to deposits, while state-owned banks such as Rastriya Banijya Bank and Nepal Bank maintained far more conservative ratios closer to 62 to 71 percent.

A falling sector-wide CD ratio across multiple consecutive years and months, as confirmed by the newest available reading, remains one of the clearest quantitative signals of a persistent credit conundrum, in which deposits keep accumulating faster than viable new loans can be found for them.

Why is credit growth still so weak despite banks holding so much surplus cash and lending rates falling to historic lows?

Nepal Rastra Bank’s July 2026 Macroeconomic Report explicitly labels this puzzle a credit conundrum and identifies four specific constraints operating simultaneously.

First, capital adequacy requirements still bind for a majority of banks and financial institutions, limiting how much more they can lend regardless of available cash.

Second, the credit-to-deposit ratio is a binding constraint for some, though not most, individual institutions even as the sector average keeps falling.

Third, declining asset quality, driven by the rising non-performing loans described earlier, is itself forcing banks into more cautious underwriting even when they have ample surplus deposits to place, meaning the bad-loan problem and the weak-lending problem are not separate issues but two faces of the same one.

Fourth, the political unrest that followed the September 2025 Gen Z protests, combined with a stagnant real estate market that underpins most bank collateral, has made both borrowers and lenders more hesitant.

By mid-May 2026, the weighted average lending rate had fallen to just 6.7 percent, and by mid-June 2026 it had eased further to 6.64 percent, historically low levels that would ordinarily be expected to unleash a wave of new borrowing, yet private sector credit growth for the fiscal year came in at around 6 percent, well short of the 12 percent Nepal Rastra Bank had originally targeted.

Looking ahead, Nepal Rastra Bank’s own Macroeconomic Report projects credit growth rebuilding toward roughly 11 percent in fiscal year 2026/27 alongside 14 percent money supply growth, as these constraints are expected to gradually ease, though the central bank’s own candor about the four-part nature of the problem suggests this recovery depends on political stability, asset quality improvement, and real estate recovery all moving together rather than any single lever.

What is the current state of capital adequacy across Nepal’s banks, and is it strong enough?

Nepal Rastra Bank requires commercial banks to maintain a minimum total capital adequacy ratio of 11 percent of risk-weighted assets, stricter than the 8 percent Basel minimum, reflecting the higher risk regulators attach to Nepal’s banking system.

As of mid-June 2026, the most current available figure, commercial banks’ core Tier 1 capital to risk-weighted assets stood at 9.60 percent and total capital to risk-weighted assets at 12.52 percent, with the system-wide figures, including development banks and finance companies, at 9.70 percent and 12.63 percent respectively. This is comfortably above the regulatory floor but represents a modest decline from the 13.19 percent recorded roughly ten months earlier in August 2025, showing gradual compression as rising provisioning requirements eat into the capital cushion.

Analysts caution that headline capital ratios can overstate real resilience when non-performing loans are climbing simultaneously, because rising bad loans force banks to divert an increasing share of capital into loan loss provisions rather than holding it as a genuine buffer against future shocks.

Nepal’s credit-to-GDP ratio, a broader measure of financial system exposure to the real economy, stood at 96.92 percent system-wide as of mid-June 2026, up from roughly 91 percent in mid-2025 data, reflecting deep and deepening credit penetration that increases the system’s overall exposure to any sharp deterioration in loan quality, funding costs, or external shocks such as remittance volatility or renewed political instability.

What did Nepal Rastra Bank actually announce in its monetary policy for fiscal year 2026/27?

Nepal Rastra Bank unveiled its 25th annual monetary policy on July 7, 2026, presented by Governor Biswo Nath Poudel. Under Section 94 of the Nepal Rastra Bank Act, 2002, the central bank is required each year to review the previous year’s policy and justify its plans ahead, and this year NRB structurally changed how it does this, splitting what used to be one document into a slim monetary policy statement carrying the actual decisions and a separate, much longer Macroeconomic Report titled Macroeconomic Report: Analysis and Outlook, July 2026, that carries the detailed data and forecasts behind those decisions.

The policy targets economic growth of about 7.0 percent and average consumer price inflation of around 5.5 percent for fiscal year 2026/27, mirroring the government’s own budget assumptions. The Macroeconomic Report itself is candid that 7 percent growth would sit well above Nepal’s estimated potential growth rate of around 4.2 percent, meaning the economy would need to operate above its normal capacity to hit the target, an assessment that looks especially cautious set against the 3.85 percent growth actually recorded for the year just ending.

Nepal Rastra Bank left all key interest rates unchanged: the policy repo rate remains at 4.25 percent, the standing deposit facility floor at 2.75 percent, and the bank rate ceiling at 5.75 percent, alongside unchanged cash reserve ratio, statutory liquidity ratio, and standing liquidity facility arrangements, signaling continuity rather than fresh tightening or easing. Governor Poudel described the stance as cautiously accommodative, and business groups including the Federation of Nepalese Chambers of Commerce and Industry broadly welcomed it as positive and balanced.

How is this new monetary policy likely to affect banks and the broader liquidity situation going forward?

Because Nepal Rastra Bank chose continuity over further rate moves, the immediate practical effect on banks is one of stability, but the central bank’s own Macroeconomic Report explicitly projects continued excess liquidity through the coming fiscal year, meaning the underlying glut is unlikely to resolve on its own.

Instead, Nepal Rastra Bank is relying on a package of structural measures. It plans to complete a study on reclassifying banks and financial institutions so different categories of institutions can be encouraged to expand into specific underserved market segments rather than all competing in the same space, and intends to simplify and consolidate its web of regulatory directives, starting with those covering credit flow, interest rates, and financial consumer protection.

On consumer protection specifically, the central bank wants to end unlimited personal liability arising from personal guarantees on loans, ease the blacklisting consequences that follow a single bounced cheque, and set clearer rules for restructuring loans extended to distressed industries.

Nepal Rastra Bank also plans to study how peer-to-peer lending platforms built on individual credit scoring could be regulated, and will continue consolidating bank branches in areas where digital banking has reduced the need for physical outlets, a process that had already removed 160 branches by mid-May 2026 without materially harming access to financial services.

Alongside this, the central bank intends to keep managing day-to-day liquidity through the standing deposit facility, deposit collection auctions, and Nepal Rastra Bank bonds, while continuing to encourage commercial banks to invest surplus foreign currency in foreign government securities.

Nepal Rastra Bank’s own forecast is that money supply will grow 14 percent and private sector credit 11 percent in fiscal year 2026/27, both a meaningful step up from this year’s sluggish pace, contingent on non-performing loan pressures easing as economic activity picks up.

What role are remittances and foreign exchange reserves playing in all of this, and how solid is that external buffer really?

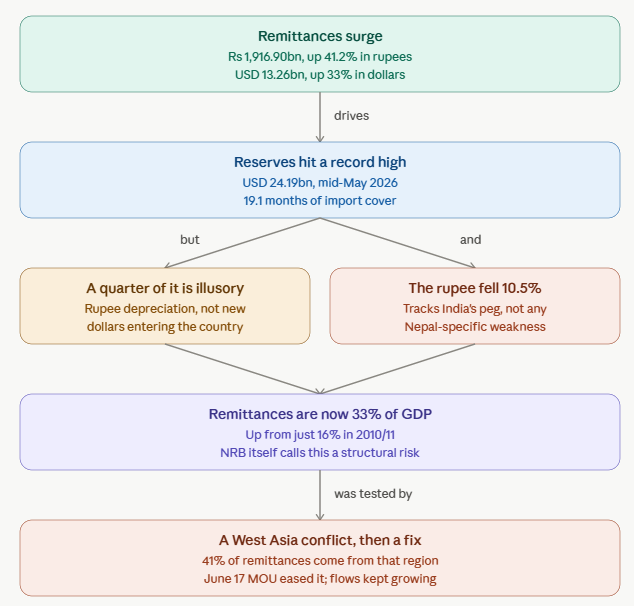

Remittances are the single biggest driver of the deposit glut. Inflows rose 41.2 percent in rupee terms to Rs 1,916.90 billion over the first ten months of fiscal year 2025/26, equivalent to a 33.0 percent increase in dollar terms to USD 13.26 billion. This has pushed gross foreign exchange reserves to Rs 3,704.5 billion, equivalent to roughly USD 24.19 billion, as of mid-May 2026, sufficient to cover a record 19.1 months of prospective imports, far above the traditional three-month adequacy benchmark.

However, Nepal Rastra Bank’s Macroeconomic Report adds an important caution the headline figure obscures: about a quarter of the reserve increase over the review year came not from genuine new inflows but from valuation gains created purely by the depreciation of the Nepali rupee against the US dollar, meaning existing dollar-denominated reserves simply became worth more in rupee terms without any new dollars actually entering the country.

The rupee itself depreciated by about 10.5 percent against the dollar between mid-July 2025 and mid-2026, a decline that traces almost entirely to Nepal’s fixed peg to the Indian rupee rather than to any Nepal-specific weakness, since the Indian rupee slid roughly 6 percent against the dollar over the same window amid capital flows toward US assets.

More fundamentally, Nepal’s reserve strength rests overwhelmingly on remittances, which have grown from around 16 percent of GDP in 2010/11 to an estimated 33.02 percent of GDP in fiscal year 2025/26 by the National Statistics Office’s full-year measure, a structural imbalance Nepal Rastra Bank itself says needs correcting over time through stronger exports and tourism earnings rather than being treated as a permanent cushion.

The escalation of conflict between Israel, the United States, and Iran in early 2026, following a February 28, 2026 strike that killed Iran’s Supreme Leader and prompted a retaliatory closure of the Strait of Hormuz, briefly pushed crude oil prices above USD 100 a barrel and threatened roughly 41 percent of Nepal’s total remittance inflow that originates from workers in the West Asia region, though remittances kept growing regardless, and a June 17, 2026 memorandum of understanding between the United States and Iran reopened the strait and eased prices back down.

How does Nepal’s banking sector health compare with other countries in South Asia?

Placed alongside its regional neighbors, Nepal’s banking sector sits in a genuinely awkward middle position, worse than India but considerably better than Bangladesh. Comparative non-performing loan data reported around 2026 places India at roughly 2.2 to 2.3 percent, Bhutan at 4.5 percent, the Maldives at 5.5 percent, Nepal at 5.6 percent, Pakistan at 5.8 to 7.4 percent depending on the source and period, and Sri Lanka at 6.5 to 12.6 percent.

Bangladesh stands in a category of its own: its non-performing loan ratio reached 32.26 percent of total loans by March 2026, the second highest in the world after war-torn Ukraine, following the exposure of previously concealed bad loans after the fall of the Awami League-led government in August 2024. Bangladesh’s capital adequacy ratio actually turned negative, at minus 2.64 percent by the end of 2025, compared with 17.20 percent in India, 20.80 percent in Pakistan, and 19.40 percent in Sri Lanka.

Sri Lanka offers a more encouraging parallel: despite formally defaulting on its sovereign debt in 2022, it has since restored political stability through elections and made substantial economic progress, even as its non-performing loan ratio remains elevated.

India, for its part, worked through its own severe bad loan crisis a decade ago, commonly called the twin balance sheet problem, and brought its ratio down from around 7.9 percent in 2020 to roughly 2.2 percent today through forced transparency, legal reform, and bank consolidation.

According to the Asian Development Bank’s 2025 report on non-performing loans in Asia, the regional South Asian average stood at 3.5 percent as of the end of 2024, meaning Nepal’s current ratio already sits meaningfully above the regional norm.

What are the key risks ahead, and what reforms have been proposed to address them?

Nepal Rastra Bank commissioned a dedicated Banking Sector Reform Recommendation Task Force, chaired by Rewat Bahadur Karki, whose comprehensive report was released in December 2025.

Governor Biswo Nath Poudel handing over letter of appointment to task force coordinator Rewat Bahadur Karki in June 2025. File photo

It identified ten specific supervisory challenges, including regulatory arbitrage that misclassifies high-risk loans into lower-risk categories to inflate reported capital adequacy, compromised independence for chief risk officers and internal auditors whose evaluations are effectively controlled by the same chief executives they are meant to check, inadequate verification of how loan proceeds are actually used, and poor-quality supervisory data that undermines system-wide monitoring of large borrowers.

The task force notably pushed back against reflexive further bank mergers, observing that institutions which have remained independent have often outperformed those that consolidated. Beyond banking specifically, Nepal Rastra Bank’s own risk assessment for fiscal year 2026/27 centers on three broader threats that would flow directly through to bank balance sheets if they materialize.

First, renewed escalation in West Asia remains a live possibility even after the June 2026 memorandum of understanding between the United States and Iran, since underlying disputes over the Strait of Hormuz and Iran’s nuclear program remain unresolved, with any resumption of hostilities threatening to simultaneously push fuel prices back up and squeeze remittance inflows.

Second, a forecast super El Niño weather pattern threatens to disrupt the monsoon cycle Nepali agriculture depends on, potentially triggering droughts similar to those that already hurt paddy production in 2025/26.

Third, growth momentum depends heavily on whether the government can finally execute its capital budget at scale, having managed only 32.5 percent of its capital spending target and 68.6 percent of total expenditure through the first eleven months of fiscal year 2025/26; continued under-execution would leave the current spending-led growth strategy unable to deliver its intended demand boost, indirectly prolonging the weak credit demand and rising non-performing loans already straining the banking sector.

![Police heighten security after suspiciously parked vehicles found outside media houses and Bhatbhateni [Photo Feature]](https://english.nepalnews.com/wp-content/uploads/2026/07/media-house-ma-suspectful-gadi_NPL-5-44f91c39-1650-4d93-aab5-3214a95e3374.jpeg)