Kathmandu

Wednesday, June 17, 2026

Tens of thousands of savers—from farmers to retirees—have lost life savings in Nepal’s cooperative collapse, as embezzlement, political nexus, and delayed reforms continue to undermine trust

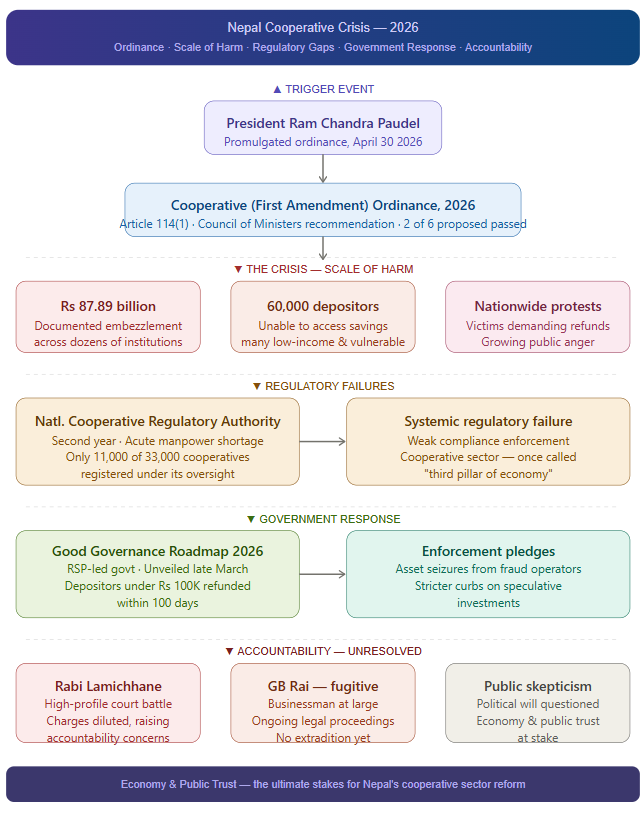

KATHMANDU: President Ram Chandra Paudel has promulgated the Cooperative (First Amendment) Ordinance, 2026, in a renewed bid to tackle Nepal’s deepening cooperative crisis. The ordinance was issued on April 30, 2026, under Article 114 (1) of the Constitution on the recommendation of the Council of Ministers. According to the president’s office, it is one of only two ordinances approved so far out of six proposed by the government.

The move comes as Nepal’s cooperative sector, once hailed as the third pillar of the economy, continues to reel from one of the country’s most devastating financial scandals.

As of May 1, 2026, parliamentary investigations have documented at least Rs 87.89 billion in direct embezzlement across dozens of institutions, with total liabilities likely far higher. Around 60,000 depositors remain unable to access their savings, many of them from low-income and vulnerable groups.

The crisis has exposed systemic regulatory failures. The National Cooperative Regulatory Authority, now in its second year, faces acute manpower shortages and weak compliance, with only about 11,000 of the country’s 33,000 cooperatives registered under its oversight. Nationwide protests by victims continue, reflecting growing public anger and loss of trust.

Amid mounting pressure, the RSP-led government unveiled its Good Governance Roadmap 2026 in late March, pledging to begin refunds for small depositors, prioritizing those with savings under Rs 100,000 within 100 days. The plan also promises asset seizures from fraud-accused operators and stricter curbs on speculative investments.

However, skepticism remains high. Ongoing court battles involving high-profile figures such as Rabi Lamichhane and fugitive businessman GB Rai, along with recent dilution of serious charges, have raised questions about political will and the government’s ability to deliver meaningful accountability and reform. This Nepal News explainer examines the multiple dimensions of Nepal’s cooperative crisis and what is ultimately at stake for the country’s economy and public trust.

How did the cooperative scam in Nepal actually begin and spread?

The roots of Nepal’s cooperative crisis stretch back decades but exploded into a full-blown scandal in the early 2020s when many institutions drifted far from their original mission. Cooperatives were meant to empower rural communities through savings, credit, and small-scale productive activities like agriculture and dairy.

Instead, after the 1992 Cooperative Act and constitutional recognition in 2007 and 2015, the sector ballooned to over 33,000 entities, with the vast majority focusing on deposit collection and lending rather than genuine economic production.

Weak multi-tiered federal regulation for a handful operating across provinces and provincial and local for the rest created massive loopholes. Directors, often with political connections, treated member funds as personal capital, channeling billions into risky real estate deals, cryptocurrency speculation, and even private media ventures.

The COVID-19 economic slowdown triggered panic withdrawals that exposed the rot. By 2023-2024, parliamentary probes uncovered systematic siphoning in at least 40 high-profile cooperatives, revealing how funds meant for farmers and housewives were funneled through shell accounts and related companies.

What started as isolated mismanagement snowballed into a nationwide crisis affecting tens of thousands, eroding public trust and forcing even solvent cooperatives to struggle with liquidity.

The lack of real-time audits, credit information systems, and independent oversight allowed the fraud to spread unchecked for years, turning what was once a grassroots success story into a symbol of elite capture and institutional failure that continues to haunt Nepal’s financial landscape even in 2026.

What is the true scale of losses today, and who are the main victims?

The human and financial toll of Nepal’s cooperative scandal remains staggering.

Official figures from parliamentary committees and the Problematic Cooperative Management Committee point to at least Rs 87.89 billion in confirmed embezzlement, though broader liabilities across distressed institutions are likely to exceed this, including unrecovered loans and hidden diversions.

Over 60,000 depositors, primarily low-income retirees, small farmers, housewives, daily-wage laborers, and small traders, have seen their life savings vanish. Many had deposited modest sums expecting safe, community-based returns, only to face total ruin.

In cases like Swarnalakshmi alone, thousands lost access to funds critical for medical treatment, education, and daily survival. The ripple effects are heartbreaking: families skipping healthcare, children pulled from school, and some descending into despair or suicide.

Even cooperatives not directly implicated suffer from panic-driven runs, threatening the livelihoods of the sector’s 7 million-plus members and nearly 100,000 employees.

As of early 2026, only a fraction of the claimed amounts around Rs 772 million in earlier phases has been returned, leaving most victims in limbo.

This isn’t just numbers on a balance sheet; it’s a profound betrayal that has widened inequality, crippled rural economies where cooperatives once filled banking gaps, and shattered faith in community institutions that were supposed to uplift the vulnerable rather than exploit them.

What was the finding of Surya Thapa-led parliamentary committee regarding cooperative fraud?

Formed on May 28, 2024, following relentless obstruction of Parliament by the Nepali Congress, the seven-member special committee led by then-MP from CPN (UML), Surya Thapa, investigated the embezzlement of billions in cooperative savings.

Surya Bahadur Thapa, then-MP and chair of the Parliamentary Investigation Committee on the Misuse of Cooperative Savings Fund formed by the previous House of Representatives. File photo.

The committee was established primarily to probe the illegal diversion of funds from several cooperatives into Gorkha Media Network, involving high-profile figures like Rabi Lamichhane.

The report found that 40 cooperatives had embezzled a total of Rs 87.89 billion from depositors. A committee also identified the involvement of four officials from Gorkha Media Network in the misappropriation of Rs 650 million obtained from a cooperative.

It further recommended legal action against Lamichhane and others for signing fraudulent checks.

Gagan Thapa was a pivotal figure in this process; his fiery parliamentary speeches and persistent demands for a “fair probe” forced the government’s hand.

He presented evidence including court records and check copies linking political leaders to the scam, later insisting that the government must implement the report’s findings to restore public trust and return depositors’ money.

Who is GB Rai, and why is he central to the biggest fraud cases?

Gitendra Babu Rai, better known as GB Rai, emerges as the central architect in Nepal’s largest cooperative embezzlement web.

As chairman of Gorkha Media Network, he stands accused of orchestrating the diversion of at least Rs 2.65 billion from multiple cooperatives, including Swarnalakshmi, Surya Darshan, Sahara Chitwan, and others directly into his media empire, notably to sustain Galaxy 4K Television operations.

GB Rai. File photo

Investigations revealed systematic transfers via unauthorized checks and accounts, with cooperative savings allegedly used to fund personal businesses, hospitals, colleges, and media ventures without repayment mechanisms.

Rai’s influence allowed him to monopolize leadership roles, pass control to relatives when scrutiny intensified, and evade accountability by fleeing the country. He remains a fugitive, reportedly in Malaysia or elsewhere, despite an Interpol diffusion notice, passport revocation, and red-corner alerts.

Even after the attorney general’s January 2026 decision to drop money-laundering and organized-crime charges across linked cases benefiting him, alongside dozens of others, core fraud allegations persist. His case perfectly illustrates how cooperative funds were laundered into private empires, exploiting regulatory blind spots and political patronage.

Victims and watchdogs view him as symbolic of the scandal’s deeper rot, where connected insiders treated public savings as venture capital while ordinary depositors bore the devastating losses. Efforts to extradite him continue, but progress has been glacial, underscoring the challenges of cross-border justice in high-profile financial crimes.

What is Rabi Lamichhane’s latest legal status in the cooperative cases?

As of April 2026, Rastriya Swatantra Party chairman and former Home Minister Rabi Lamichhane remains embroiled in multiple cooperative fraud cases across five districts, including Kaski, Kathmandu, Rupandehi, Chitwan, and Parsa, linked to alleged misuse of funds funneled toward Gorkha Media Network during his tenure as managing director.

He faces accusations of authorizing hundreds of millions in transfers, including Rs 480 million via solo-signed checks in the Sahara Chitwan case alone.

In January 2026, the Attorney General approved amendments dropping the more serious money-laundering and organized-crime charges while retaining cooperative fraud allegations, a move that sparked three writ petitions in the Supreme Court.

GB Rai (left) and Rabi Lamichhane (right)/File photo

By late March, the Supreme Court bench of Binod Sharma and Abdul Aziz Musalaman referred those challenges to a full bench for deeper scrutiny, signaling ongoing legal contention.

Lamichhane has appeared in court for hearings, received formal dates (including one in the Swarnalakshmi case set for mid-April), and secured bail in several instances after posting guarantees equivalent to claimed amounts.

He maintains his innocence, insisting he was unaware of illicit fund sources. However, courts continue active proceedings, with some lower courts halting charge withdrawals temporarily.

Debates have intensified over conflicts of interest, especially given his past ministerial role, while his party’s push for “dialogue over detention” draws criticism for potentially undermining accountability. The cases remain far from resolved, with victims and legal experts watching closely for any sign of political influence.

What were the specific legal penalties and findings against Ichchha Raj Tamang and his associates regarding the Civil Cooperative money laundering case?

In early 2024, the Special Court sentenced former lawmaker and civil cooperative promoter Ichchha Raj Tamang to three years in jail and a fine of Rs 1.72 billion. His wife, Srijana Shakya, and relative Keshav Lal Shrestha each received one-and-a-half-year sentences, with fines of 1.03 billion and 256.58 million, respectively.

The court found them guilty under the Money Laundering Prevention Act for investing embezzled public deposits totaling approximately 5.67 billion into private ventures like Civil Homes.

Ichchha Raj Tamang. File photo

To ensure justice for the thousands of victims lured by promised 17% interest rates, the court ordered the seizure of properties from all defendants, decreeing that these assets be used for victim compensation.

While Tamang’s daughters received clean chits, the ruling emphasized that the laundered funds were systematically used to enrich the family through various real estate projects without collateral.

How deep does the political nexus run in protecting scam operators?

The political nexus in Nepal’s cooperative scandal runs disturbingly deep, often acting as both enabler and shield for those responsible. Many cooperative directors held affiliations with major parties or wielded economic influence that translated into political protection, allowing them to bypass leadership term limits, lending caps, and transparency rules for years.

High-profile cases like those tied to Gorkha Media reveal how funds were allegedly diverted to media ventures with indirect political links, blurring lines between business, media, and governance.

The January 2026 Attorney General decision to amend charges, dropping money-laundering and organized-crime counts against over 50 accused, including Lamichhane and fugitive GB Rai, ignited accusations of selective leniency, especially as it came amid election-year pressures.

Critics argue this move, later challenged in the Supreme Court, effectively softened accountability for powerful figures while victims waited empty-handed. Even the RSP’s own policy suggestions favoring dialogue in fraud cases have fueled perceptions of self-interest.

This entanglement explains why asset recovery remains painfully slow, prosecutions selective, and regulatory enforcement inconsistent.

Without genuine depoliticization such as insulating the National Cooperative Regulatory Authority from interference or enforcing strict conflict-of-interest bans, the system risks perpetuating the very capture that turned community savings into tools for elite enrichment.

Victims and civil society groups consistently highlight how this nexus has prolonged suffering, eroded judicial credibility, and delayed the systemic reforms Nepal desperately needs.

What concrete promises has the current government made to resolve the crisis?

The Balen-led government, sworn in after the March 2026 elections, has placed cooperative reform at the heart of its agenda through the ambitious Good Governance Roadmap 2026, unveiled in late March.

The Cabinet meeting at the Office of the Prime Minister and Council of Ministers recommended the ordinance on April 27. Photo courtesy: PMO

Key pledges include fast-tracking refunds for small depositors, prioritizing those with savings under Rs 100,000 via the Deposit and Credit Guarantee Fund, and aiming to begin disbursements within 100 days.

It commits to seizing and auctioning assets of convicted fraudsters to build a compensation pool, abolishing the outdated Department of Cooperatives, and empowering the National Cooperative Regulatory Authority with genuine autonomy and quasi-judicial powers.

Other promises involve banning unproductive investments like real estate and stocks, enforcing “one person, one cooperative” rules, rolling out digital off-site monitoring, establishing a dedicated Credit Recovery Tribunal, and linking all societies to a centralized Credit Information Center.

The roadmap also stresses federal-provincial coordination to plug local-level loopholes and prioritizes productive lending to realign cooperatives with their community roots.

Early April saw ministerial engagements with victim groups reaffirming these timelines. While these steps represent the most comprehensive blueprint yet, implementation remains the litmus test; past ordinances delivered limited results, and skepticism lingers among depositors who have heard similar assurances before.

Success will hinge on political will transcending electoral cycles and delivering tangible relief before further erosion of public trust.

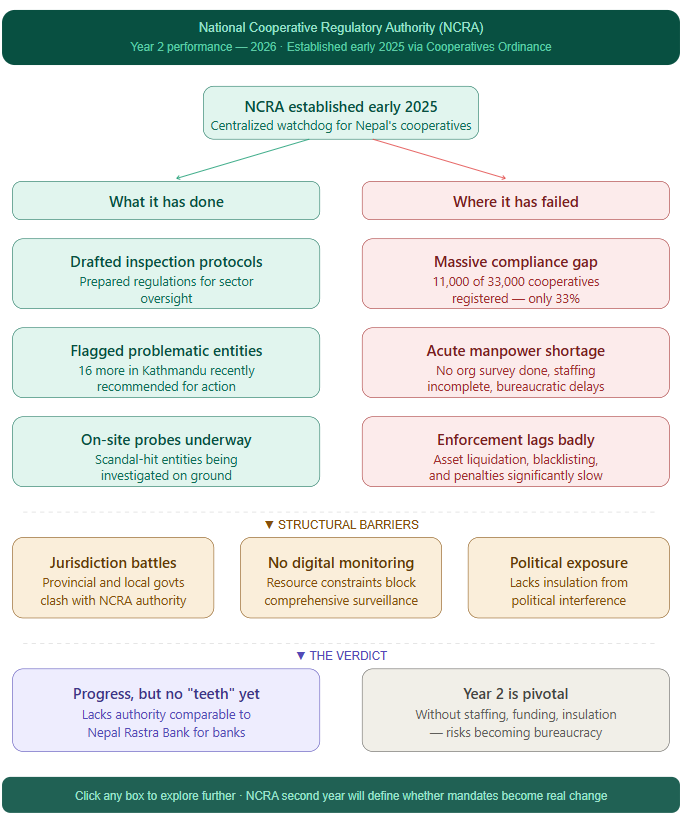

How has the National Cooperative Regulatory Authority performed since its creation?

Established in early 2025 via the Cooperatives Ordinance, the National Cooperative Regulatory Authority (NCRA) was hailed as the long-overdue centralized watchdog for Nepal’s fragmented sector.

Now entering its second year in 2026, its performance has been mixed at best, hampered by persistent structural challenges. The authority has drafted inspection protocols, prepared regulations, and begun recommending additional cooperatives as “problematic,” including 16 more in Kathmandu alone in recent months.

However, only about 11,000 of the country’s 33,000 cooperatives have registered under it, reflecting compliance gaps and capacity issues. Manpower shortages remain acute: no full organization and management survey has been completed, permanent staffing is incomplete, and frequent bureaucratic hurdles have slowed momentum.

On-site probes of scandal-hit entities are underway, but asset liquidation, defaulter blacklisting, and enforcement actions lag significantly. Critics note that while the NCRA represents progress toward uniform oversight, it still lacks the full “teeth” of an independent body comparable to Nepal Rastra Bank for commercial lenders.

Jurisdiction battles with provincial and local governments persist, and resource constraints have limited its ability to conduct comprehensive digital monitoring.

Victims and analysts argue that without accelerated staffing, dedicated funding, and insulation from political pressure, the authority risks becoming another layer of bureaucracy rather than the decisive reformer it was designed to be. Its second year will be pivotal in proving whether it can translate mandates into meaningful change.

What major reforms does the Good Governance Roadmap 2026 propose?

The Good Governance Roadmap 2026 stands as Nepal’s boldest attempt yet to overhaul the cooperative sector, proposing sweeping structural, legal, and technological changes. At its core is the push to dissolve the Department of Cooperatives and vest real authority in an autonomous National Cooperative Regulatory Authority equipped with on-site inspection powers, digital monitoring tools, and quasi-judicial enforcement.

It calls for mandatory registration of all savings-and-credit cooperatives, strict term limits for directors, conflict-of-interest prohibitions, and a nationwide credit information center to track defaulters in real time.

Unproductive investments, real estate, speculative stocks, or unrelated ventures are to be banned outright, with lending refocused on productive sectors like agriculture and small enterprises.

For victims, the roadmap prioritizes small depositors with refunds starting within 100 days through a revamped guarantee fund, financed partly by auctioned fraudster assets.

A dedicated debt recovery tribunal is proposed to expedite cases, alongside stronger federal-provincial-local coordination to close oversight gaps. Technology-driven off-site supervision and member education campaigns aim to rebuild transparency and trust.

If fully executed, these measures could realign cooperatives toward their original community-empowerment mandate while preventing future abuse.

However, the roadmap’s success depends on rapid legislative backing, resource allocation, and sustained political commitment, which are elements that have eluded previous reform efforts. Implementation timelines are ambitious, but early signals suggest the new government is treating this as a flagship priority.

Why do victims keep protesting despite repeated government assurances?

Cooperative victims continue taking to the streets in 2026 because years of unfulfilled promises have bred profound, well-earned skepticism.

Since the 2023 Maitighar protests and subsequent parliamentary probes, depositors have heard repeated commitments to partial refund caps in the ordinance, crisis declarations for select institutions, and now the Roadmap’s 100-day pledge, yet tangible relief remains elusive for most.

Only a small fraction of the claimed Rs 87 billion-plus has been returned, with bureaucratic delays, court backlogs, and asset-sale obstacles stalling progress.

Many victims, already living hand-to-mouth, see high-profile charge amendments (like the January 2026 decision diluting cases against key accused) as evidence that politics still trumps justice.

Protests serve as their only consistent leverage, drawing media attention and pressuring authorities when ministerial dialogues feel performative. The human stakes are immediate: untreated illnesses, lost homes, and shattered futures for retirees and farmers who trusted the system.

Even as the new government unveils ambitious roadmaps, victims recall past cycles where commissions formed, reports submitted, and little changed. Until concrete refunds reach bank accounts, arrests produce visible accountability, and reforms deliver systemic safeguards rather than paper promises, skepticism will fuel continued mobilization.

Their persistence underscores a deeper democratic demand: that governance must prioritize ordinary citizens’ savings over elite protection.

How does Nepal’s cooperative model differ from successful global examples, making it so vulnerable?

Nepal’s cooperative model deviates sharply from global best practices, creating inherent vulnerabilities that fueled the current crisis. Internationally, successful cooperatives—whether in dairy in India’s Amul model, agriculture in Europe, or credit unions in North America—emphasize productive activities, member ownership, democratic governance, and diversified revenue beyond pure financial intermediation.

They operate with robust internal audits, professional management, and strong regulatory oversight akin to banks. In Nepal, however, over 25,000 of roughly 33,000 cooperatives skewed heavily toward savings-and-credit operations, collecting deposits with minimal checks on lending quality or asset quality.

This deposit-driven focus invited speculation in real estate and unrelated ventures without corresponding productive assets to buffer downturns.

Multi-level regulation (federal, provincial, and local) created fragmentation and capacity gaps, unlike centralized models elsewhere. Political patronage often trumped merit in leadership selection, violating core cooperative principles of autonomy and neutrality.

The absence of mandatory credit bureaus or real-time reporting until recent reforms exacerbated risks. Global successes thrive on transparency and member education; Nepal’s version suffered from opacity and elite capture.

The 2026 Roadmap acknowledges these flaws by pushing diversification, NRB-style supervision, and technology integration steps that could align Nepal closer to resilient international models if implemented rigorously. Until then, the sector remains exposed to the very shocks that turned trust into widespread financial ruin.

What specific red flags emerged from investigations into cooperatives like Swarnalakshmi?

Investigations into Swarnalakshmi Multipurpose Cooperative exposed textbook patterns of fraud that mirrored dozens of other cases. Forensic audits traced over Rs 1.19 billion allegedly diverted from more than 5,000 depositors through unauthorized checks, fictitious loans, and direct transfers to Gorkha Media Network entities.

Leadership was monopolized, with founders and relatives cycling through key positions to evade scrutiny. Funds were funneled into unrelated businesses, media, hospitals, and colleges without repayment plans or collateral enforcement, creating massive asset-liability mismatches.

Swarnalakshmi Multipurpose Cooperative

Similar red flags appeared in Sumeru, Capital Savings, and Surya Darshan: chronic under-recovery of loans, inflated leadership tenures, and political-economic ties that shielded operators.

Parliamentary committees documented Rs 71 billion in savings against Rs 88 billion in liabilities across 40 entities, highlighting systemic weak debt collection and governance capture.

In Swarnalakshmi’s case, even after the chairman fled, control passed to family members, perpetuating the scheme. These patterns’ lack of internal controls, absence of independent audits, and diversion to connected enterprises proved how cooperatives operated as personal fiefdoms rather than member-owned institutions.

The revelations shifted public discourse from isolated incidents to systemic failure, pressuring authorities into forming the NCRA and drafting the 2026 Roadmap, though full accountability for these specific frauds remains pending in courts.

Why has recovering depositors’ money proven so difficult?

Recovering embezzled cooperative savings has proven extraordinarily challenging due to a toxic mix of legal, logistical, and political hurdles.

Fugitives like GB Rai remain beyond immediate reach despite Interpol notices, while identified assets are often tied up in protracted litigation or concealed through complex corporate structures. Court backlogs delay asset auctions, with challenges from defendants further slowing processes.

Many borrowers listed as defaulters are either untraceable or politically connected, making enforcement selective. Even when properties are seized, valuation and sale procedures under existing laws are cumbersome and yield far less than claimed losses.

The 2025 ordinance and 2026 roadmap introduce faster mechanisms like a dedicated tribunal and guarantee fund, but implementation lags amid resource constraints at the NCRA.

Earlier partial refund schemes capped at modest amounts left larger depositors in limbo, while panic-driven liquidity crises in healthier cooperatives complicated sector-wide solutions. International cooperation for extradition and asset tracing remains slow.

Without aggressive political neutrality, real-time digital tracking, and streamlined debt-recovery courts, billions stay frozen while victims endure years of uncertainty. The human cost compounds daily, as families forgo essentials waiting for justice that feels perpetually delayed by systemic inertia and vested interests.

What broader economic and social fallout has the crisis caused?

The cooperative scandal’s fallout extends far beyond lost savings, inflicting deep economic and social wounds across Nepal.

Financially, panic withdrawals have destabilized even solvent institutions, triggering closures, job losses among 94,000 sector employees, and a credit crunch in rural areas where cooperatives once bridged formal banking gaps.

The sector’s historical contribution to GDP and financial inclusion has been tarnished, deterring new investment and pushing depositors toward already strained commercial banks.

Socially, the impact is heartbreaking: low-income families report skipped medical care, children withdrawn from school, increased indebtedness, and in extreme cases, suicides linked to financial despair.

Trust in community institutions has evaporated, widening inequality as the poor disproportionately affected bear the brunt while elites evade full consequences.

Regionally, rural economies suffer most, reversing decades of grassroots empowerment. Nationally, the crisis has fueled political polarization, protests, and cynicism toward governance, contributing to broader discontent that helped topple previous administrations.

Long-term, without credible recovery and reform, Nepal risks repeating cycles of informal finance vulnerability whenever new savings vehicles emerge.

The scandal underscores how unchecked financial mismanagement can erode social cohesion and economic resilience in a country already navigating post-pandemic recovery and development challenges.

What role did parliamentary probes play in exposing the scam?

Parliamentary investigations played a pivotal role in dragging the cooperative scandal from whispers to national reckoning. The 2024 Special Committee on Misuse of Cooperative Savings, chaired by Surya Thapa, conducted forensic-level scrutiny of 40 problematic institutions, documenting Rs 71 billion in savings against higher liabilities and recommending prosecutions, regulatory overhaul, and victim compensation.

It spotlighted Bagmati Province as a hotspot and flagged political-economic capture, shifting the narrative from isolated fraud to systemic rot. Subsequent committees reinforced calls for asset seizures, leadership bans, and an independent authority. These probes triggered the formation of NCRA and pressured governments into action, including the Balen government’s roadmap.

By publicly naming high-profile figures and tracing fund flows to media ventures, the committees empowered victims, mobilized media attention, and forced judicial processes.

Though follow-through has been imperfect with some charge amendments later drawing criticism, the probes proved that legislative oversight can drive accountability when wielded with determination.

They also highlighted the need for permanent mechanisms like a dedicated tribunal, influencing current reform debates and ensuring the crisis remains a political priority rather than fading into bureaucratic obscurity.

What key changes did the 2025 Cooperatives Ordinance actually deliver?

The Cooperatives Ordinance 2025 marked an initial legislative response by creating the National Cooperative Regulatory Authority as a centralized overseer. It introduced director term limits, capped large deposits, mandated quarterly defaulter reporting to credit bureaus, and tightened lending rules to curb speculation.

Inter-provincial cooperatives came under stronger federal scrutiny, while modest refund priorities were outlined for crisis-ridden entities. Registration became mandatory for savings-and-credit societies, aiming to bring the sector’s fragmented operations under one umbrella.

However, delivery has been uneven: the NCRA still faces staffing and jurisdictional hurdles, with low compliance rates persisting into 2026. The ordinance prioritized partial refunds and basic governance fixes but stopped short of full NRB-style supervision or comprehensive asset-recovery mechanisms.

It served as a necessary foundation, prompting further recommendations in the 2026 Roadmap for digital tools and tribunals. While positive on paper, enforcement gaps have left many provisions feeling like incremental rather than transformative change.

Victims note that without aggressive implementation and political backing, the ordinance’s impact remains limited, underscoring the gap between legislation and on-the-ground relief.

Why does regulation still feel toothless despite new laws and institutions?

Regulation in Nepal’s cooperative sector feels toothless in 2026 because new institutions like the NCRA operate within the same fragmented, under-resourced, and politically influenced ecosystem that enabled the original crisis.

Despite the 2025 ordinance, the 2026 roadmap, and the latest ordinance issued on April 30, oversight remains split across federal, provincial, and local levels, with 80% of cooperatives still under weaker local governance.

The NCRA grapples with manpower shortages, incomplete digital infrastructure, and jurisdiction disputes, limiting its ability to conduct meaningful on-site inspections or enforce blacklisting.

Frequent staff transfers disrupt continuity, while the absence of a fully functional debt recovery tribunal leaves asset liquidation mired in courts. Political meddling evident in charge amendments and selective enforcement undermines independence, as seen in controversies surrounding high-profile cases.

Even former central bank experts have hesitated to lead due to perceived risks. Without genuine autonomy, dedicated funding, and real-time technological monitoring, regulators lack the “teeth” to deter fraud or compel compliance.

Public pressure and judicial oversight provide some checks, but until the system addresses these core weaknesses, the sector risks repeating history. The roadmap’s emphasis on centralization and tech offers hope, yet execution will determine whether regulation evolves from symbolic to substantive.

How have federal, provincial, and local governments failed in oversight?

Oversight failures across Nepal’s three tiers of government lie at the heart of the cooperative scandal.

Federal authorities regulated only a tiny fraction (around 145) of interprovincial societies, while provincial and especially local governments handling over 80% of the 33,000 entities lacked expertise, resources, and political will.

Bagmati Province, home to nearly a third of active cooperatives, exemplified widespread irregularities due to weak enforcement and governance lapses.

Local units, often understaffed and politically influenced, allowed thousands of inactive or paper cooperatives to persist while fraud flourished unchecked.

Coordination gaps between levels delayed probes and asset recovery. The NCRA’s creation aimed to centralize supervision, yet low registration rates and ongoing jurisdiction battles show persistent fragmentation.

Provincial-federal handoffs created blind spots where most savings reside, particularly in rural areas. Past governments’ inertia despite early warnings from 2014 complaints compounded the problem.

The roadmap seeks to fix this through unified standards and digital systems, but until all tiers enforce uniform accountability without interference, vulnerabilities will remain.

This multi-level failure not only enabled billions in losses but also eroded citizens’ faith in decentralized governance itself.

What lasting lessons should Nepal draw to prevent future scams?

Nepal must internalize several hard lessons from the cooperative crisis to safeguard against recurrence.

First, transparency and professional governance are non-negotiable: mandatory digital audits, real-time reporting, and independent boards free from political patronage can prevent elite capture.

Second, diversification beyond deposit-lending is essential; cooperatives should refocus on productive sectors like agriculture and micro-enterprises, mirroring successful global models that build real assets rather than chase speculation.

cooperative victims protesting in Buddhanagar in Kathmandu demanding justice. File photo

Third, robust, independent regulation modeled on Nepal Rastra Bank, with dedicated tribunals and credit bureaus, is critical to close loopholes.

Fourth, member education and public awareness campaigns can empower depositors to demand accountability rather than blindly trust.

Fifth, depoliticization through strict conflict-of-interest laws and insulation of regulators ensures decisions serve communities, not connected insiders.

Finally, swift justice mechanisms, including asset tracing and international cooperation, must accompany any future crisis response.

Only by treating cooperatives as true community institutions—transparent, productive, and accountable—can Nepal restore trust and prevent another generation from losing hard-earned savings to systemic betrayal.

What does the future hold for Nepal’s cooperative sector?

Looking ahead, Nepal’s cooperative sector stands at a genuine crossroads, with cautious optimism possible if the Good Governance Roadmap translates into action.

Swift refunds for small savers within the promised 100-day window could ease immediate suffering and rebuild some trust, while structural changes like an empowered NCRA, investment bans, and digital oversight might prevent recurrence.

Success could see cooperatives rebound as engines of inclusive growth, refocused on productive lending and community needs. However, risks abound: ongoing court battles, fugitive operators, and implementation delays could prolong victim distress and deepen cynicism.

Political transitions or waning attention might sideline reforms, leaving the sector scarred and irrelevant. Broader economic pressures, remittance fluctuations, and post-LDC graduation challenges will test resilience.

If executed with transparency and urgency, the roadmap offers a path to revitalization; failure risks permanent erosion of financial inclusion, pushing millions toward informal or riskier options.

The coming months, starting with tangible disbursements and visible arrests, will reveal whether this is transformative reform or another unfulfilled pledge.

Ultimately, the sector’s future depends on whether Nepal learns from this betrayal to prioritize people over patronage, ensuring cooperatives once again serve as pillars of hope rather than symbols of despair.