Kathmandu

Sunday, June 21, 2026

Established between the 1960s and 1980s, Nepal’s public enterprises were meant to build self-reliance, but many now struggle with inefficiency, political interference, and low returns

KATHMANDU: Nepal established most of its public enterprises between the 1960s and 1980s to spark industrialization, generate employment, and secure strategic sectors when the private economy was still nascent. Today the country maintains 45 such entities, covering power, fuel, aviation, cement, water, and financial services.

While a few utilities post solid profits, many others suffer chronic losses due to outdated plants, political appointments, and weak management. By late 2025 the government’s total exposure had climbed past Rs 930 billion, yet returns to the treasury remain minimal, sparking renewed calls for reform, selective revival, mergers, and closures.

What are public enterprises in Nepal and why were they originally set up?

Public enterprises, often called state-owned enterprises, are companies where the government holds full or majority ownership and plays a direct role in operations. Nepal began creating them in earnest during the Panchayat period and continued into the early democratic era.

The main goal was to build industrial capacity in a country that lacked strong private investors at the time. Policymakers believed the state needed to take the lead in producing essential goods like cement, sugar, textiles, and cigarettes, while also managing critical services such as electricity generation and distribution, petroleum imports, domestic aviation, and drinking water supply.

These entities were expected to create jobs, especially in regions far from Kathmandu, reduce dependence on imports, and promote balanced regional development. Many received support through foreign aid or soft loans from friendly countries.

In those early decades the approach made some sense because the private sector was small and risk-averse. However, over time the model revealed serious weaknesses. Without market discipline or strong oversight, many enterprises became inefficient, overstaffed, and vulnerable to political influence.

By the 1990s liberalization led to the privatization or closure of more than 80 earlier entities, leaving behind a smaller but still significant portfolio of 45 today. The original vision of self-reliance has largely given way to debates about whether these firms still serve the public interest or have become an expensive drag on the national budget.

How many public enterprises exist in Nepal as of early 2026, and what sectors do they operate in?

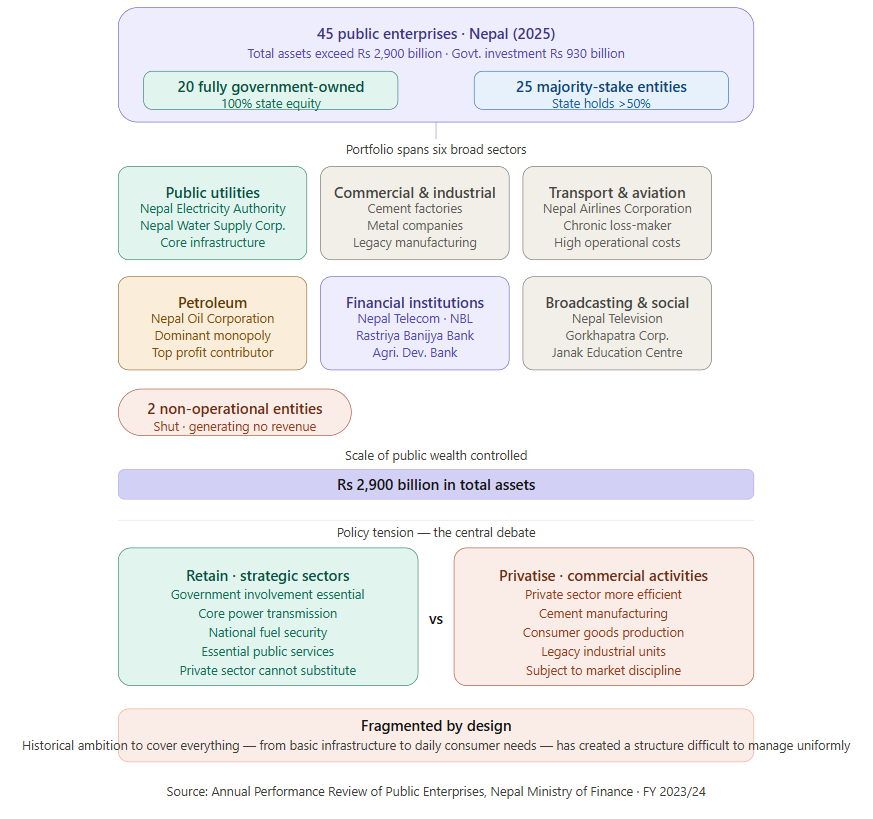

As of the latest available official reviews from 2025, Nepal operates 45 public enterprises. Of these, 20 are fully owned by the government while the state holds a majority stake in the remaining 25. The portfolio spans several broad categories.

Public utilities include major players like the Nepal Electricity Authority and Nepal Water Supply Corporation. Commercial and industrial units cover cement factories, metal companies, and remnants of older manufacturing ventures.

Transport and aviation feature Nepal Airlines Corporation. Petroleum remains dominated by the Nepal Oil Corporation. There are also financial institutions, broadcasting services, and a few specialized service or social sector bodies.

Two enterprises remain non-operational or fully shut. The total assets controlled by these entities exceed Rs 2,900 billion, making them a substantial part of public wealth even if their contribution to overall economic growth feels limited compared to the expanding private sector.

The spread across sectors reflects the historical ambition to cover everything from basic infrastructure to daily consumer needs, but it has also created a fragmented structure that is difficult to manage uniformly.

Recent policy discussions emphasize the need to distinguish between truly strategic operations that require government involvement and purely commercial activities that could be handed over to private players.

What does the most recent financial performance data show for Nepal’s public enterprises?

According to the Annual Performance Review of Public Enterprises covering fiscal year 2023/24, the 45 public enterprises together recorded a net profit of Rs 42.62 billion. This figure represented a decline of nearly 13 percent from the previous year.

While 28 enterprises managed to stay in profit, 15 incurred losses totaling Rs 3.63 billion, and two remained inactive. Operating revenue across the board stood at around Rs 660 billion, showing only marginal change.

The biggest profit contributors continued to be entities with natural advantages or monopoly positions, such as the Nepal Oil Corporation, which posted strong results in recent years thanks to improved pricing mechanisms and infrastructure upgrades.

Nepal Electricity Authority also generated significant revenue from power sales and exports, though its profit dipped in 2024/25 due to higher costs and foreign exchange losses.

On the negative side, traditional loss-makers like certain cement plants, water supply operations, airlines, and education material producers continued to struggle. Dividend payments to the government dropped sharply to Rs 8.83 billion, reflecting weaker overall performance and the limited cash actually flowing back to the treasury.

These numbers highlight a persistent pattern: a handful of utilities carry the load while many others require ongoing support.

Why do so many of Nepal’s public enterprises continue to run at a loss year after year?

The reasons behind the repeated losses are deep-rooted and interconnected. Many factories and plants rely on decades-old technology that cannot compete with modern private or imported alternatives, driving up production costs while lowering quality and efficiency.

Political appointments to boards and management positions often prioritize loyalty over professional expertise, leading to delayed decisions, poor procurement choices, and sometimes outright interference in daily operations.

Labor unions, frequently aligned with political parties, resist necessary reforms such as staff rationalization or performance-based incentives, resulting in high administrative expenses and low productivity. Weak accountability mechanisms mean that even clear cases of mismanagement rarely lead to consequences.

External shocks like past power shortages, the 2015 earthquake, or global price fluctuations hit these entities harder because they typically operate with thin financial cushions. Accumulated debts, unfunded pension obligations, and environmental liabilities further strain their balance sheets.

Nepal Earthquake 2015. File photo

In many cases the original social objectives, providing employment or subsidized services, clash with commercial viability, yet governments hesitate to adjust pricing or scope for fear of public backlash.

Without fundamental changes in governance and market orientation, the cycle of losses and repeated bailouts is likely to continue.

Which public enterprises are the strongest performers and which ones generate the heaviest losses?

The standout performers tend to be those enjoying regulated or monopoly-like positions. The Nepal Oil Corporation has consistently delivered strong profits in recent years through efficient fuel handling and the adoption of automatic pricing adjustments.

Nepal Electricity Authority also ranks among the top contributors, generating revenue from domestic sales and growing electricity exports to India, although its margins faced pressure in 2024/25 from rising expenses and currency fluctuations. Certain financial and investment-related entities have also shown steady results when managed with relative autonomy.

At the other end, chronic loss-makers include Nepal Airlines Corporation, burdened by high operational costs, aging fleet issues, and accumulated debts running into tens of billions.

Nepal Water Supply Corporation struggles with poor revenue collection and infrastructure maintenance. Older industrial units such as Hetauda Cement and certain textile or rubber factories continue to bleed money due to obsolete machinery and inability to match market competition.

Janak Education Materials Centre and broadcasting services have also featured regularly among the under-performers. These loss-making entities often account for the bulk of the sector’s red ink, highlighting how a small number of troubled operations can offset gains elsewhere.

How much has the government invested in public enterprises, and what actual returns do taxpayers receive?

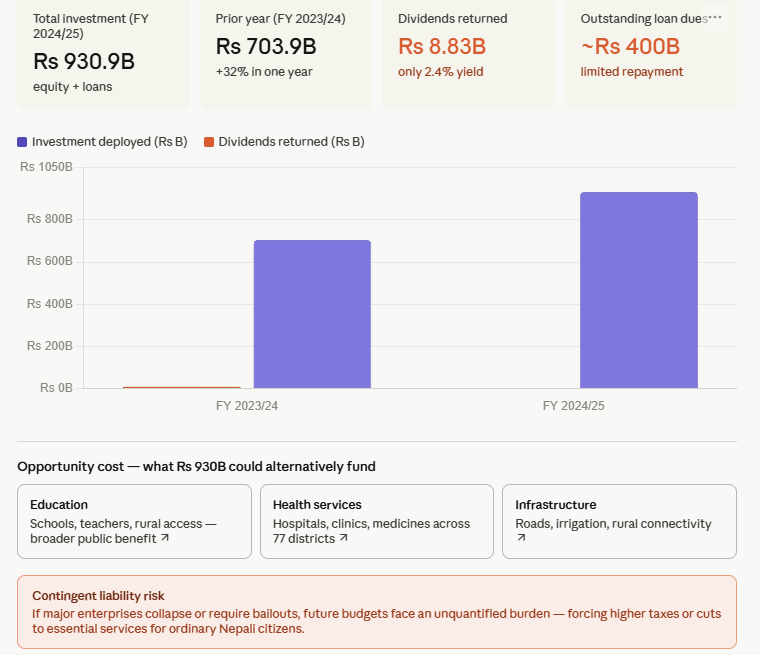

By the end of fiscal year 2024/25, the government’s total investment in public enterprises combining equity share capital and loans had reached approximately Rs 930.88 billion. Earlier reviews for 2023/24 put the figure at Rs 703.93 billion, showing steady growth as fresh funds are injected to cover shortfalls.

Despite this massive commitment, the returns flowing back remain disappointingly low. In recent years the government has received only around Rs 8.83 billion in dividends, translating to roughly a 2.4 percent yield on equity.

Repayments on loans have also been limited, with outstanding dues climbing toward Rs 400 billion in some reports. This low recovery rate means ordinary citizens, through taxes and reduced spending on other priorities, effectively subsidize these entities year after year.

The gap between investment and return creates contingent liabilities that could burden future budgets if major enterprises face collapse or require large-scale bailouts. Independent analysts point out that the opportunity cost is significant money locked in inefficient operations that could instead support critical infrastructure, education, or health services that deliver broader public benefits.

What is the historical background of public enterprises in Nepal?

The story begins in the 1960s and 1970s when Nepal, under the Panchayat system, sought to modernize its economy. With limited domestic capital and a small private sector, the state stepped in to establish factories for cement, sugar, textiles, cigarettes, and other basic goods.

Foreign assistance from countries like India and China helped fund many of these projects. After the restoration of multiparty democracy in 1990, economic liberalization brought a major wave of privatization. More than 80 enterprises were sold, closed, or dissolved during the 1990s as policymakers embraced market-oriented reforms.

The remaining core group survived because they were viewed as strategically important—securing energy supply, fuel distribution, or national aviation—or because closing them carried high political costs in terms of job losses. However, without the competitive pressures that privatization introduced elsewhere, many of the survivors stagnated.

The Privatization Act of 1994 provided a legal framework, but actual implementation slowed dramatically after 2008 due to union opposition, valuation disagreements, and shifting political priorities.

Today’s 45 enterprises represent a legacy mix of old industrial ambitions and newer service-oriented bodies, but the original development rationale has been overtaken by decades of operational challenges.

Why have several public factories remained closed for many years?

A number of industrial units, including Janakpur Cigarette Factory, Butwal Yarn Factory, Gorakhkali Rubber Industry, and older textile mills, have stayed shuttered for over a decade. The primary causes include outdated and inefficient machinery that cannot produce goods at competitive prices.

Once the economy opened to imports and private players, these state factories quickly lost market share. Labor disputes, management changes with every government shift, and lack of fresh capital for modernization compounded the problem.

A photo collage of Butwal Yarn Factory (left), Gorakhkali Rubber Industry (top right) and Janakpur Cigarette Factory (bottom right)

In some cases, land and buildings have faced encroachment or fallen into disrepair while raw material costs rose and consumer preferences changed. Successive governments have announced revival packages with great fanfare, but follow-through has been weak. Without detailed feasibility studies, clear business plans, or credible private partners, potential investors stay away.

Political hesitation to accept job losses or asset sales has also played a role. As a result, valuable public assets sit idle, generating no revenue while still incurring maintenance or security costs. The prolonged closures illustrate how good intentions without sustained execution can turn promising projects into long-term liabilities.

What steps is the government currently taking to revive closed public enterprises?

In 2025 the cabinet approved an investment management plan targeting seven long-defunct factories, including Janakpur Cigarette, Gorakhkali Rubber, Hetauda and Udayapur Cement units, and others.

The approach focuses on public-private partnership models under the existing PPP law, combined with asset revaluation, possible tax incentives, and land management strategies. An expert committee was formed to study liabilities and explore revival options, with emphasis on making commercially viable units operational again.

However, independent observers note the absence of fully fleshed-out timelines, detailed budgets, or binding commitments from potential partners. Past attempts at revival have repeatedly faltered due to changing ministers and shifting priorities.

The current push reflects growing fiscal pressure and recognition that idle assets represent wasted capital. If successful, revived factories could generate employment and reduce import dependence in selected sectors. Yet without transparent bidding, professional management, and realistic market analysis, there is a real risk that these efforts will repeat earlier disappointments.

As of early 2026, concrete restarts remain limited while studies and consultations continue.

Has privatization of public enterprises been successful in Nepal, and why has further progress stalled?

The privatization wave of the 1990s produced mixed outcomes. Some enterprises transitioned into competitive private firms that improved efficiency and innovation. Others faced difficulties, with critics pointing to inadequate worker safeguards, opaque bidding processes, or cases where assets were primarily valued for their land rather than ongoing operations.

Overall, the process helped reduce the government’s direct burden and demonstrated that market discipline could work in certain sectors.

Since around 2008, however, meaningful privatization has largely come to a halt. Strong opposition from labor unions fearful of job losses, combined with political reluctance to be accused of “selling national assets,” has kept the issue off the active agenda. Disputes over proper valuation and fears of asset stripping have added further delays.

Recent high-level recommendations have suggested partial privatization for viable units like cement plants, but actual implementation has been slow. The experience shows that successful privatization requires not only political will but also transparent mechanisms, social safety nets for affected workers, and a mature regulatory environment to prevent monopolistic abuses after sale.

What key changes does the 2025 Public Enterprises Management and Good Governance Policy introduce?

The policy approved in late 2025 represents one of the more structured attempts in years to overhaul the system. It proposes classifying enterprises into “commercial” ones that should compete on market terms and “strategic” ones essential for national interests, such as core power grid operations or fuel security.

All entities are expected to gradually convert into companies under the general Companies Act rather than operating under outdated formation orders.

The framework emphasizes reducing direct ministerial interference, appointing boards and chief executives through merit-based processes with performance contracts, and introducing greater financial discipline, including regular audits and clear exit strategies for consistently loss-making units.

It also opens the door for public share offerings or bond issuance in viable cases to broaden ownership and bring in fresh capital. While the policy sets a sensible direction toward professionalism and accountability, its success will ultimately depend on whether future governments resist the temptation to treat these entities as instruments of patronage.

Early signs suggest cautious movement, but full transformation will take consistent effort across multiple administrations.

What specific recommendations did the High-Level Economic Reform Recommendation Commission make regarding public enterprises?

The commission, led by former Finance Secretary Rameshore Khanal (who later served as Finance Minister in the interim government following the Gen Z movement) submitted its report in 2025, offering a candid and unvarnished assessment. It recommended outright closure or liquidation of five enterprises deemed beyond realistic revival, citing their chronic losses and inability to adapt.

Former Finance Minister Rameshore Khanal (middle) delivers remarks at the Ministry of Finance after he assumed the office on September 15, 2025. File photo: RSS

For the two major cement plants, it suggested merging operations where feasible, retaining a minority government stake if necessary, and selling the majority to private investors to bring in modern technology and management.

The report also advocated creating a professional holding company structure for better oversight of fully government-owned entities while pushing for performance-linked appointments and clearer separation between commercial and social objectives.

It framed the current situation as an unsustainable fiscal risk, arguing that treating public enterprises as employment schemes rather than businesses had drained public resources for decades.

Although the government has referenced the report in subsequent policy statements, full adoption of the tougher recommendations, particularly closures, has faced expected resistance from unions and local political interests. The commission’s work has nevertheless helped keep reform discussions alive on the national agenda.

Why has the proposal to place all public enterprises under a single holding company faced criticism?

Critics argue that simply creating another centralized layer would not address the fundamental problems facing individual enterprises, such as obsolete technology in one factory or fleet issues in the airline.

A holding company might concentrate rather than diversify risk, potentially turning localized failures into systemic ones. Many experts believe it could become yet another bureaucratic structure open to the same political influences that already hamper performance.

International examples show holding companies can serve as temporary bridges toward privatization or professionalization, but only when paired with decisive action on closures and sales.

In Nepal’s context, without strong safeguards, the holding company risks delaying hard choices while adding administrative overhead. Commentators have described the idea as rearranging deck chairs rather than fixing the leaking ship.

The debate underscores a broader point: structural tweaks alone rarely solve governance and incentive problems that require cultural and political shifts toward greater accountability and market orientation.

In what ways does political interference damage the performance of public enterprises in Nepal?

Political appointments frequently place party loyalists rather than sector experts in key leadership roles, leading to decisions driven by short-term considerations instead of long-term viability. Procurement processes can become avenues for favoritism, resulting in overpriced contracts or substandard supplies.

Pricing policies for essential services sometimes get distorted to serve populist goals, undermining financial sustainability. Unions aligned with political parties can block reforms or demand benefits that exceed productivity gains.

Even profitable entities occasionally face pressure to undertake projects or subsidies that serve narrow interests rather than the enterprise’s health. This environment discourages professional managers from taking tough but necessary decisions and breeds a culture where accountability is weak.

The 2025 policy attempts to limit such interference through performance contracts and merit-based selection, but changing entrenched habits will require sustained commitment from successive governments.

Until politicians view these enterprises as businesses rather than patronage networks, genuine efficiency improvements will remain elusive.

What real burden do under-performing public enterprises place on ordinary Nepali citizens?

Every fresh loan or subsidy extended to loss-making entities ultimately comes from the national budget funded by taxpayers through VAT, income tax, customs duties, and other revenues.

When dividends are minimal or nonexistent, citizens see little direct benefit from the hundreds of billions locked in these operations. Opportunity costs are significant—funds used for bailouts or debt servicing cannot support new schools, hospitals, rural roads, or irrigation projects that would deliver wider benefits.

Moreover, the growing contingent liabilities, including unpaid pensions and potential cleanup costs, represent future risks that could force higher taxes or reduced services later.

In a country still grappling with basic development challenges, propping up inefficient factories diverts scarce resources from more productive uses. Independent reviews consistently describe these enterprises as a net drain rather than an asset, highlighting how poor performance in the public sector indirectly affects the living standards of ordinary families across Nepal.

Are there any notable success stories among Nepal’s public enterprises?

Yes, a few entities demonstrate that state ownership can work under the right conditions. Nepal Electricity Authority has shown significant improvement in recent years through better tariff adjustments, reduced system losses, and expansion of hydropower capacity, enabling profitable power exports.

Nepal Oil Corporation has benefited from its strategic position in fuel supply and the introduction of more market-aligned pricing, generating substantial revenue and contributing heavily to government coffers in strong years.

Certain financial public entities have also delivered consistent results when granted operational autonomy. These brighter spots share common features: natural monopoly characteristics that limit destructive competition, relatively stable regulatory frameworks, and periods of more professional leadership less prone to day-to-day political meddling.

Their relative success proves that with clear mandates, modern management practices, and insulation from excessive interference, public enterprises can generate value. However, they remain exceptions that highlight by contrast the deeper structural issues affecting the majority of the portfolio.

How is the Balen-led government specifically addressing the reform of Public Enterprises within its 100-point roadmap?

The Balen Shah-led government’s approach to Public Enterprise reform, as outlined in the March 2026 “100 Blueprints for Governance Reform,” shifts the focus from political patronage to a commercial, results-oriented framework.

At the heart of this roadmap is the aggressive conversion of viable state entities into public limited companies, a move designed to invite market scrutiny and distribute ownership among the citizenry while reducing direct state interference.

By mandating that these enterprises operate under professional management rather than political appointees, the government is introducing strict performance contracts and key performance indicators for all chief executives.

First meeting of the Council of Ministers held on March 27 at the Office of the Prime Minister and Council of Ministers in Singha Durbar. Photo courtesy: Prime Minister’s Secretariat

This professionalization is further supported by the controversial but decisive ban on party-affiliated trade unions, which aims to eliminate the historical trend of politically motivated strikes and administrative paralysis within state units.

Complementing these roadmap goals, early 2026 governance measures include the active rationalization of overlapping administrative bodies to streamline public financial management and reduce redundant overhead costs.

Instead of pursuing sweeping privatizations, the government is prioritizing public-private partnerships for the revival of closed industrial zones, ensuring that the state retains land assets while the private sector provides the necessary technical and operational expertise.

Regular, independent performance audits are now being institutionalized to ensure that taxpayer money is utilized efficiently, signaling a broader transition toward incremental professionalization. While these reforms face ongoing challenges from displaced political interests, the current strategy focuses on building a stable, consensus-driven environment that treats public enterprises as drivers of economic growth rather than fiscal burdens.

Should Nepal continue operating commercial-style public enterprises or limit the state to only truly strategic sectors?

This question lies at the center of current policy debates. The 2025 framework explicitly tries to draw a distinction: retain significant government involvement only where private participation is impractical or where national security and essential services are at stake, such as core electricity transmission or strategic fuel reserves. For purely commercial activities like cement manufacturing or consumer goods production, the argument is that a mature private sector can now handle operations more efficiently.

Advocates of a leaner state point to decades of losses and low returns as evidence that government should focus on regulation and enabling infrastructure rather than running businesses. Critics of rapid change worry about job losses in certain regions and the risk of private monopolies replacing public ones.

Economic logic and international experience favor limiting direct state operation to genuinely strategic areas while subjecting the rest to market discipline through privatization or closure. The challenge remains translating this principle into politically feasible action.

What practical lessons can Nepal learn from its own past experience and from other countries?

Nepal’s 1990s privatization drive showed that transparent processes and adequate worker support can ease transitions, but rushed or poorly communicated efforts breed resentment and suspicion. The long stall in further reforms highlights how union resistance and political risk aversion can freeze necessary change.

Internationally, successful models emphasize professional boards insulated from day-to-day politics, clear performance metrics with consequences for failure, and decisive exit strategies for non-viable units.

Countries that treated state enterprises primarily as employment tools rather than businesses often faced escalating fiscal burdens. The clearest takeaway for Nepal is that half-hearted measures, new policies without enforcement, or holding companies without hard decisions rarely deliver results. Sustainable improvement requires consistent political courage to prioritize long-term economic health over short-term patronage, combined with transparent mechanisms that build public trust.

Learning from both domestic setbacks and global best practices will be essential if public enterprises are to become genuine assets rather than ongoing liabilities.

What is a realistic outlook for public enterprises in Nepal over the coming years?

Barring major political disruptions, change is likely to remain incremental rather than dramatic. The 2025 policy and commission recommendations have created a useful roadmap for classification, professionalization, targeted closures, and selective privatization.

A few loss-making units may eventually be shut or merged if momentum holds, while viable ones could see gradual conversion to company structures with broader ownership. Revival attempts for closed factories will continue through public-private models, though success will depend on credible execution.

Persistent challenges union resistance, valuation disputes, and the temptation to use enterprises for political purposes mean that full transformation will take time and sustained commitment across governments. If budgets in coming years show rising dividends, reduced bailouts, and actual asset recoveries rather than fresh injections, it would signal meaningful progress.

Without stronger political will to implement tough recommendations, however, the risk of continued slow leakage of public resources remains real. The coming years will test whether Nepal can finally shift from managing legacy burdens to building a more efficient and focused public enterprise sector.

(Disclaimer: This explainer is based on official performance reviews and policy documents available as of May 3, 2026. The situation continues to evolve with ongoing policy implementation and fiscal developments.)