Kathmandu

Monday, June 29, 2026

The Government of Nepal's proposed Company Act 2026 introduces mandatory beneficial owner disclosure, differential capital requirements scaled from Rs 50-250 million based on listing status, sweat equity allocations up to 40% for startups and centralized CSR fund management

KATHMANDU: Nepal is preparing to overhaul its corporate legal framework with a draft of a new Company Act that seeks to replace the two-decade-old Company Act 2006. The proposed law aims to modernize business regulation in line with the country’s digital economy, startup ecosystem and international corporate governance standards.

It introduces sweeping changes to company registration, ownership disclosure, investor protection, corporate governance, startup financing and compliance requirements, while also tightening transparency rules and expanding regulatory oversight of large businesses and strategic sectors.

What specific capital requirements does the new act establish for public companies, and how do these compare to the previous law?

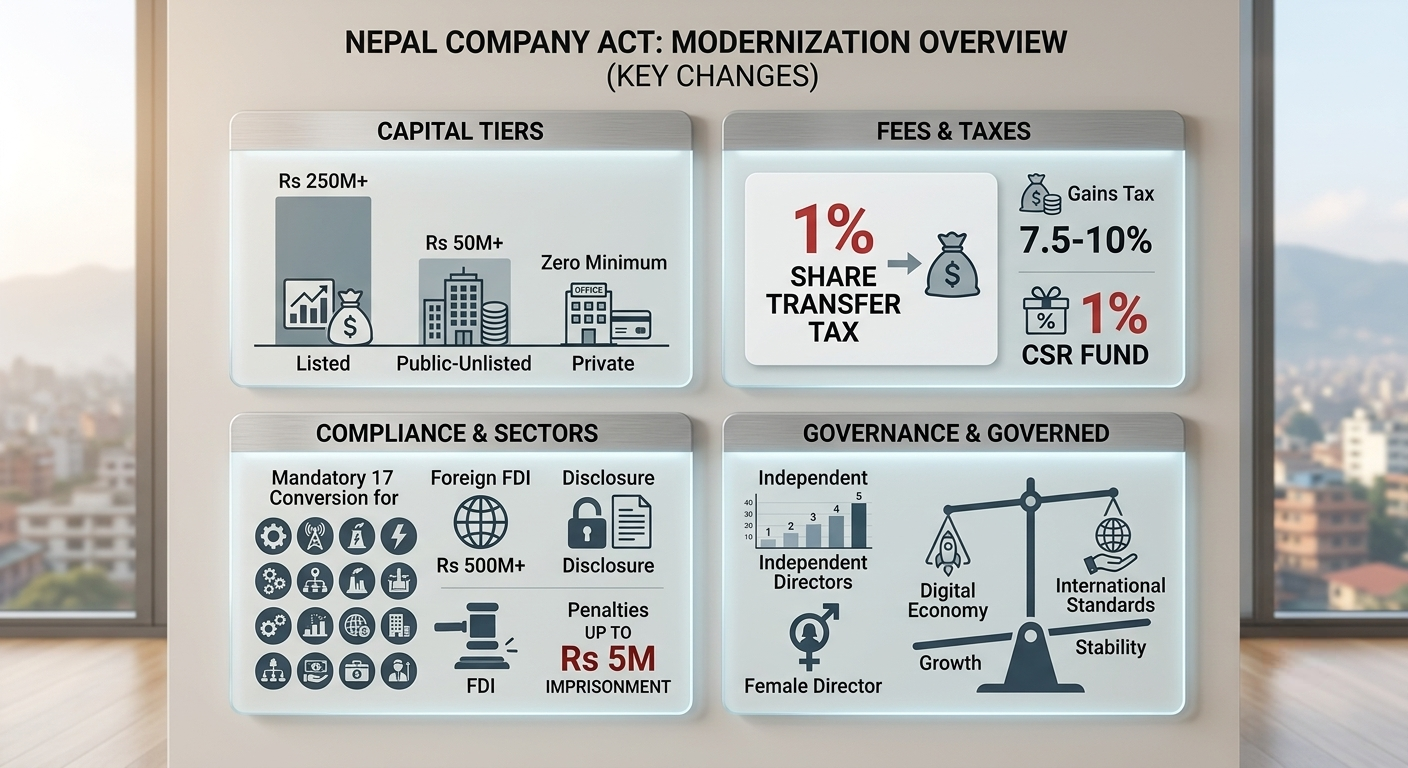

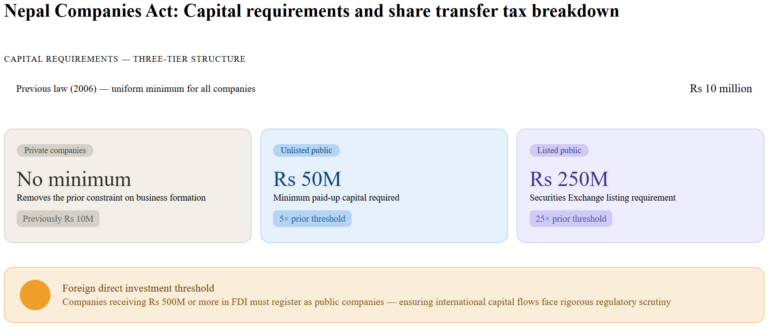

The act introduces a three-tier capital structure departing radically from the uniform Rs 10 million minimum established in 2006. Unlisted public companies must now maintain minimum paid-up capital of Rs 50 million—five times the prior threshold. Listed public companies trading on Nepal’s Securities Exchange must hold Rs 250 million minimum paid-up capital, representing a 25-fold increase from the Rs 10 million baseline.

This differentiation reflects recognition that securities market listing imposes substantial regulatory compliance burdens and continuous disclosure obligations justifying capital entry barriers. Private companies face no uniform minimum capital requirement, addressing criticism that the prior Rs 10 million mandate constrained legitimate business formation.

The tiered approach acknowledges that a manufacturing firm operating with Rs 20-30 million in paid-up capital may function efficiently as a private entity, but accessing public capital markets requires financial cushioning protecting investors from sudden insolvency.

The act specifically targets foreign investors, mandating that companies receiving Rs 500 million or more in foreign direct investment must register as public companies, ensuring international capital flows undergo rigorous public scrutiny and regulatory monitoring.

Nepal’s stock exchange currently indexes approximately 200 trading securities with mixed institutional participation; the capital requirements effectively restrict public listing to medium and large enterprises.

Industry observers note that existing listed firms predominantly exceed Rs 250 million capitalization, suggesting the new baseline aligns with current market composition rather than imposing new barriers on established entities seeking continued listing status.

How does the 1% share transfer tax function, and what are the specific transaction costs investors now face?

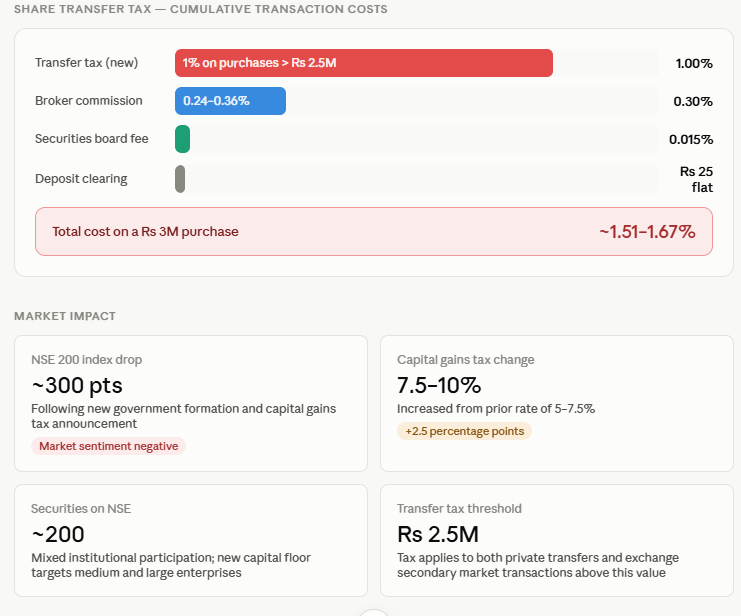

The government introduced a 1% transfer tax on share purchases exceeding Rs 2.5 million, collected from the buyer upon beneficial ownership transfer. This provision applies simultaneously to private company transfers and stock exchange secondary market transactions, creating immediate controversy regarding market impact.

For private transactions, the company registrar collects the tax during transfer recording and deposits funds in the federal consolidated fund. For exchange-traded shares, brokers collect the 1% tax alongside existing trading costs and remit proceeds to the consolidated fund. This dual application means stock market investors now face cumulative transaction costs substantially exceeding historical levels.

Current secondary market trading costs already include broker commission ranging from 0.24% to 0.36% of transaction value, a securities board fee of 0.015% per transaction, and a deposit clearing charge of Rs 25 per transaction executed. Adding the 1% transfer tax on purchases exceeding Rs 2.5 million means a single share purchase at Rs 3 million faces approximately 1.51-1.67% in combined transaction costs (1% transfer tax plus 0.24-0.36% broker commission plus 0.015% board fee).

Market participants compared this unfavorably to prior cost structures, noting that transaction taxes typically reduce market liquidity. Stock market indices reflect this sentiment: the NSE 200 benchmark dropped approximately 300 points following the new government’s formation and announcement of capital gains tax increases from 5-7.5% to 7.5-10%.

Legal scholars noted that beneficial owner disclosure and transfer taxation operate on parallel timelines, potentially creating double compliance burdens and confused implementation procedures during the legislative refinement period.

Why did the Ministry initiate the revision of 1% share transfer tax provision?

The Ministry of Industry, Commerce and Supplies has initiated removal of the controversial 1% share transfer tax provision from the proposed act following intense market opposition that triggered broad-based investor concern.

The NSE 200 benchmark index fell 16.54 points to close at 2,632.96 within the first trading day after the draft’s public release, signaling immediate market deterioration. Ministry officials acknowledged that “many suggestions” opposing the provision arrived during the public feedback phase, stating the draft represented preliminary recommendations subject to substantial modification rather than final legislative language.

RSP lawmaker Hari Dhakal intervened publicly claiming the tax should apply exclusively to “off-market” private transactions where direct company name-registry transfers occur, not to NEPSE secondary market trading where institutional clearing mechanisms and regulatory oversight operate.

The Ministry’s revision process indicates recognition that transaction taxes reduce market liquidity precisely when policymakers simultaneously announced capital gains tax increases from 5-7.5% to 7.5-10%, creating compounding disincentives to equity market participation at a moment when capital market deepening constitutes government priority for facilitating private sector expansion.

What does the 1% CSR fund contribution require from large corporations, and how is this centralized fund controlled?

Companies with annual turnover exceeding Rs 250 million must deposit minimum 1% of net annual profit into a mandatory central CSR fund, eliminating prior discretionary spending frameworks. A company generating Rs 1 billion in annual turnover with 20% net profit margin faces mandatory Rs 200 million annual profit, requiring Rs 2 million CSR contribution.

This centralization represents fundamental policy shift from decentralized company discretion over social spending to government-managed fund allocation. Smaller companies with turnover below Rs 250 million retain voluntary CSR participation, though the act permits such enterprises to contribute if preferred.

The proposed act establishes a seven-member governing committee chaired by the Industry Minister, with mandatory membership including secretaries from the Prime Minister’s Office, Commerce Ministry, and Finance Ministry; the National Planning Commission secretary; Nepal Rastra Bank’s deputy governor; and the company registrar serving as member-secretary. This composition excludes corporate representatives entirely, concentrating spending discretion exclusively within government hands.

The committee must convene minimum twice annually, though additional meetings occur as needed. Permissible fund applications include education, healthcare, disaster management, environmental conservation, skill development for disadvantaged communities, financial literacy programs, cultural heritage maintenance, infrastructure in remote districts, orphanage and elder care facility operations, human trafficking victim rehabilitation, pandemic response, and nationally significant research initiatives.

Nepal Rastra Bank in Thapathali. Photo: Bikram Rai/Nepal News

The Nepal Rastra Bank previously conducted studies documenting systematic CSR misuse: many companies directed funds toward brand promotion and leadership relationship-building rather than demonstrable social benefit. Implementing agencies must file impact reports within three months of fiscal year conclusion detailing activities, expenditure categories, and documented social outcomes.

This centralized model builds on international best practice acknowledging that genuine social benefit requires professional fund deployment rather than corporate brand-building disguised as philanthropy.

What are the specific beneficial owner disclosure requirements, and what penalties apply for non-compliance?

The act mandates that individuals holding registered share certificates must declare if they represent beneficial (ultimate) owners or merely hold shares on behalf of actual beneficiaries. Company registration applications now require founders, shareholders, and beneficiary owners to provide identifying documentation establishing true control chains.

Public and large private companies must disclose beneficial ownership structures in annual financial statements. This requirement directly targets ownership concealment that the Nepal Rastra Bank’s investigations documented: extensive use of benamed (proxy) shareholding enabling money laundering and illicit asset concealment. Under the act, companies systematically withholding beneficial ownership information face penalties from Rs 500,000 to Rs 5 million depending on violation severity.

Company officers bearing responsibility for false beneficial owner declarations face Rs 1 million to Rs 3 million fines plus 1-3 year imprisonment, establishing serious criminal jeopardy. Companies providing deliberately false beneficial ownership information receive substantial penalties; officers face imprisonment up to 3 years. This criminal threshold represents categorical distinction from regulatory violations typically addressed through civil penalties.

The beneficiary owner definition encompasses any person enjoying economic benefit or exercising control over company decisions and profits, regardless of formal share registration name. For corporate shareholders (one company holding another’s shares), registrars require disclosure of the ultimate individual beneficiaries within the corporate structure, preventing use of company-within-company structures to obscure ownership indefinitely.

The provision specifically addresses situations common in Nepali private equity where founding family members place assets in trusted employees’ or relatives’ names to manage estate complexity or avoid marital property disputes—previously legal but now requiring formal declaration to prevent regulatory arbitrage.

What are the mandatory public company sectors, and which foreign investment levels trigger conversion requirements?

The act designates 17 business categories requiring mandatory public company status: mining and mineral extraction (specifically copper, iron, gold, silver, natural gas, and petroleum extraction/refining); telecommunications; securities trading and stock exchange operations; securities issuance agencies; mutual fund management; portfolio/investment management; remittance and foreign exchange services; electricity generation, transmission, and distribution exceeding 5 megawatts; insurance operations; banking and financial institutions; government companies; and credit rating agencies.

Any company receiving cumulative foreign direct investment of Rs 500 million or more must convert to public status, ensuring international capital flows receive public market scrutiny. Existing private companies operating in these sectors face mandatory conversion within two years of the act’s enactment, creating transition obligations for thousands of entities.

Delay penalties escalate: companies missing the two-year deadline face 0.1% of paid-up capital annually during year one for non-compliance charges, increasing to 0.3% annually in year two and beyond. A private mining company with Rs 100 million paid-up capital operating in a mandatory sector faces Rs 1 million annually if conversion delays into year two (0.3% of Rs 100 million). This graduated penalty structure creates financial pressure without immediate bankrupting consequences, allowing conversion transitions while discouraging indefinite delay.

The mandatory classification reflects government determination that strategic sectors warrant public accountability mechanisms including shareholder meetings, transparency requirements, and regulatory scrutiny enabling government oversight of critical infrastructure, particularly regarding capacity, service quality, and security implications.

Nepal’s telecommunications sector, largely private following deregulation, now faces retroactive public company requirements; Nepal Oil Corporation already operates as state-owned public entity.

What are the specific sweat equity percentages for startups versus general companies, and how is valuation determined?

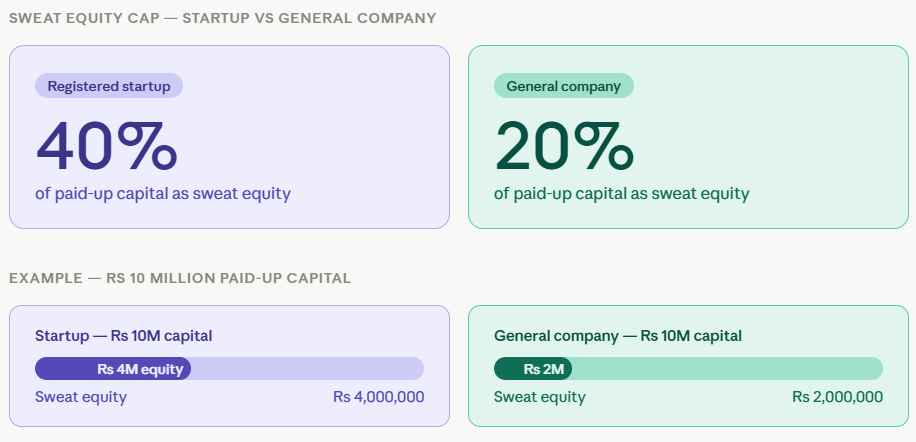

The act permits companies to issue shares to employees and founders as compensation for intellectual property contributions, technology transfer, business innovation, and similar non-cash value additions. General (non-startup) companies may allocate maximum 20% of paid-up capital as sweat equity.

Startup enterprises officially registered under Nepal’s startup framework receive substantially higher allowances: 40% of paid-up capital may constitute sweat equity. This differential reflects deliberate government support for technology-driven enterprises operating on knowledge and innovation rather than accumulated financial capital. A startup with Rs 10 million paid-up capital may issue Rs 4 million in sweat equity to founders/employees contributing core technology or business concepts.

An established company with Rs 10 million capitalization can issue only Rs 2 million maximum in sweat equity. Valuation of sweat equity requires certification by independent professional valuers, preventing artificial over-pricing that would dilute other shareholder interests without corresponding business value.

Agreements between companies and employees/founders must document sweat equity terms in writing, specifying vesting schedules, conditions for forfeiture, and performance criteria if applicable. The act recognizes intellectual property, technical knowledge, goodwill contributions, service value, and technology transfer as legitimate valuation bases. This framework removes structural barriers preventing capital-poor talented individuals from participating in company ownership.

Previous law’s requirement for cash contributions meant startup founders operating on venture capital or bootstrapped capital could issue equity only through cash injections, limiting employee participation regardless of contribution magnitude. The sweat equity provision enables technology firms to retain skilled staff through equity participation while conserving scarce capital for operational expenses.

What is the new company secretary threshold, and what relief does it provide to small enterprises?

Prior law mandated company secretaries for all enterprises with paid-up capital exceeding Rs 10 million, imposing substantial compliance costs on modest firms. The act raises this threshold to Rs 500 million exclusively for private companies, exempting thousands of small and medium enterprises from mandatory secretary employment. Listed and public companies retain unconditional secretary requirements regardless of capital size.

A manufacturing company operating at Rs 20 million paid-up capital—representing substantial enterprise for rural Nepal—previously faced mandatory secretary employment at annual salary typically Rs 3-5 lakh, consuming 15-25% of net profit for marginal enterprises. This reform reflects calculation that professional company secretary value correlates more strongly with entity complexity and regulatory burden than mechanical capital thresholds.

A company with Rs 1 billion capitalization managing complex shareholder structures, multiple regulatory agencies, and substantial employee workforces genuinely benefits from professional secretaries coordinating statutory compliance. A Rs 20-million manufacturing or professional services firm with single or family ownership can typically manage compliance through finance staff or external consultants without permanent secretary positions.

This risk-based compliance approach aligns with international governance frameworks where regulatory intensity scales with enterprise complexity rather than uniform thresholds.

The exemption applies only to private companies; public companies including those with minimal capitalization must maintain secretaries. This distinction reflects recognition that public company status carries inherent accountability obligations—quarterly disclosures, shareholder meeting administration, regulatory correspondence—justifying professional staff regardless of capital size.

What gender and independent director provisions does the act introduce?

The act links independent director requirements to board composition rather than maintaining uniform minimums. Boards comprising seven or fewer directors must include minimum one independent director. Boards exceeding seven members require minimum two independent directors. Prior law mandated only one independent director for all public companies regardless of board size, failing to account for agency risks escalating with larger boards.

Public companies with female shareholders must designate minimum one female director on the board, mandating gender representation proportional to ownership diversity. This requirement addresses documented underrepresentation of women in Nepali corporate governance despite women comprising substantial shareholder percentages.

Independent directors must satisfy specific independence criteria: no employment relationships with company management, no significant business dealings with the company, and no family connections to controlling shareholders. These provisions reflect international governance standards adopted by major economies, positioning Nepal competitively for foreign investment evaluation.

Research from developed markets demonstrates that independent board oversight correlates with reduced fraud, improved capital allocation, and reduced management entrenchment. Female director representation addresses both fairness and empirical evidence that gender-diverse boards improve decision-making quality through broader perspective integration.

What share transfer tax ambiguities exist regarding secondary market application?

The most critical implementation uncertainty concerns whether the 1% share transfer tax applies to stock exchange secondary market trading. The act’s language indicates that shares transferred through “securities exchange system” undergo identical 1% taxation, with brokers collecting proceeds for central fund deposit. This interpretation would add approximately 1% to trading costs for exchange-traded shares, suppressing market activity already demonstrating weakness.

Current secondary market trading volume reflects investor concerns regarding additional tax burdens. The NSE 200 benchmark index dropped 300 points following government formation and announcement of concurrent capital gains tax increases from 5-7.5% to 7.5-10%. These combined provisions—capital gains tax increase plus potential 1% transfer tax on secondary trading—create compounding disincentives to equity market participation.

Market analysts argue that transaction taxes typically reduce liquidity, trading volume, and price discovery efficiency through reduced participation. Professional broker associations protested the provision’s secondary market application, arguing that tax policy should distinguish between illiquid private share transfers and organized exchange trading requiring regulatory approval and transparent pricing.

Current secondary market trading volume reflects investor concerns regarding additional tax burdens. The NSE 200 benchmark index dropped 300 points following government formation and announcement of concurrent capital gains tax increases from 5-7.5% to 7.5-10%. These combined provisions—capital gains tax increase plus potential 1% transfer tax on secondary trading—create compounding disincentives to equity market participation.

The government acknowledged implementation ambiguity and committed to refinement during the legislative process, indicating that final enacted language may restrict transfer taxation to private transfers while exempting organized exchange trading. This distinction would align with international practice where taxes on private transactions serve anti-evasion functions while exchange trading receives regulatory facilitation through cost minimization. The resolution remains pending based on stakeholder feedback during public consultation phases.

How do the act’s penalty structures compare to prior law, and what conduct attracts criminal imprisonment?

The act substantially increases penalties across all violation categories, reflecting tougher enforcement philosophy. Most significantly, false beneficial owner disclosure by responsible officers attracts Rs 1 million to Rs 3 million fines plus 1-3 year imprisonment, establishing serious criminal jeopardy. Companies withholding beneficial ownership information face Rs 500,000 to Rs 5 million penalties; the lower range applies to minor omissions while the upper range addresses systematic concealment.

Company officers engaging in asset misappropriation, document falsification, or fraud face 2-5 year imprisonment plus criminal fines equivalent to the value embezzled. Prior law’s penalty structures proved insufficient to deter violations by calculating actors who viewed civil fines as ordinary business costs.

The criminal imprisonment provisions shift calculation incentives by imposing personal liberty consequences beyond corporate entity penalties. These enhanced sanctions align with international corporate governance expectations where major economies impose imprisonment for financial statement fraud and beneficial ownership concealment.

Officers face cumulative penalties: both corporate entity fines and individual criminal prosecution, preventing use of corporate liability as shield against personal accountability. The graduated penalty approach incentivizes good-faith compliance efforts while severely punishing intentional evasion. Technical non-compliance receives modest penalties; deliberate deception attracts criminal sanctions.

This severity reflects specific focus on preventing money laundering and corruption where beneficial owner concealment constitutes essential infrastructure. By establishing serious personal consequences, the act attempts behavior modification among corporate leadership toward fuller compliance.

How does the strike-off mechanism address inactive company registration accumulation?

The act recognizes that thousands of registered companies exist without conducting actual business operations, consuming registrar resources and complicating property title searches. Companies failing to submit annual financial statements or conducting no business activities for three consecutive years qualify for automatic strike-off by the registrar following notice procedures. This strike-off power eliminates lengthy dissolution proceedings previously required under 2063 law, removing bureaucratic impediments that left defunct companies cluttering the registry indefinitely.

For companies proactively seeking deregistration, the act provides expedited pathways. Firms applying for deregistration within two years of the act’s enactment face maximum Rs 500,000 combined penalties regardless of accumulated non-compliance violations, providing substantial financial incentive for voluntary closure.

Beyond the two-year window, standard penalty schedules apply based on violation severity and duration. This transitional generosity acknowledges that thousands of registered companies represent failed ventures; maintaining their registry presence serves no regulatory function while creating psychological barriers to formal closure.

Previously, accumulating penalties for missed financial statements discouraged formal deregistration, leaving zombie companies technically alive but not operating. The strike-off mechanism relieves entrepreneurs from perpetual liability for defunct ventures, removing stigma associated with business failure and encouraging eventual formal closure rather than indefinite non-compliance.

Registrars must follow defined procedures protecting creditor interests during strike-off, enabling creditor claims before final removal from registry. This balance prevents company owners from using strike-off to escape legitimate liabilities while eliminating bureaucratic costs for genuinely defunct enterprises.

What capital gains tax changes accompany the new act, and how do these affect investor incentives?

The government announced simultaneous changes to capital gains taxation on share transactions as part of a broader push toward “final taxation” concepts. Prior rate structure taxed capital gains at 5-7.5% based on holding period and income category. The revised rate increased to 7.5-10%, representing 33-50% rate increase depending on the prior applicable rate. This increase accompanies the proposed 1% share transfer tax, creating compound disincentives to trading activity.

An investor purchasing shares at Rs 100 and selling at Rs 130 faces 30 rupees capital gains. Under prior law at 5% rate, taxes consumed Rs 1.50 of gain (5% of Rs 30). Under new law at 7.5% rate plus the 1% transfer tax on the Rs 130 sale transaction, total taxes increase to approximately Rs 3.45 (Rs 2.25 from capital gains tax at 7.5% plus Rs 1.30 from 1% transfer tax), representing 130% increase in total tax burden. However, implementation confusion remains regarding whether capital gains taxation applies separately from transfer taxation or whether transactions face exclusively one mechanism.

The government indicated in budget announcements that capital gains would become final taxation (no additional income tax on investment returns), theoretically maintaining revenue neutrality. However, the actual statutory implementation remains unclear.

The Nepal Rastra Bank tracks trading volume through exchange member reporting; recent declines correlate with these tax announcements. Market participants expressed concerns that compounding taxation rates would reduce foreign investor participation and domestic capital market depth, potentially reducing capital availability for listed company expansion.

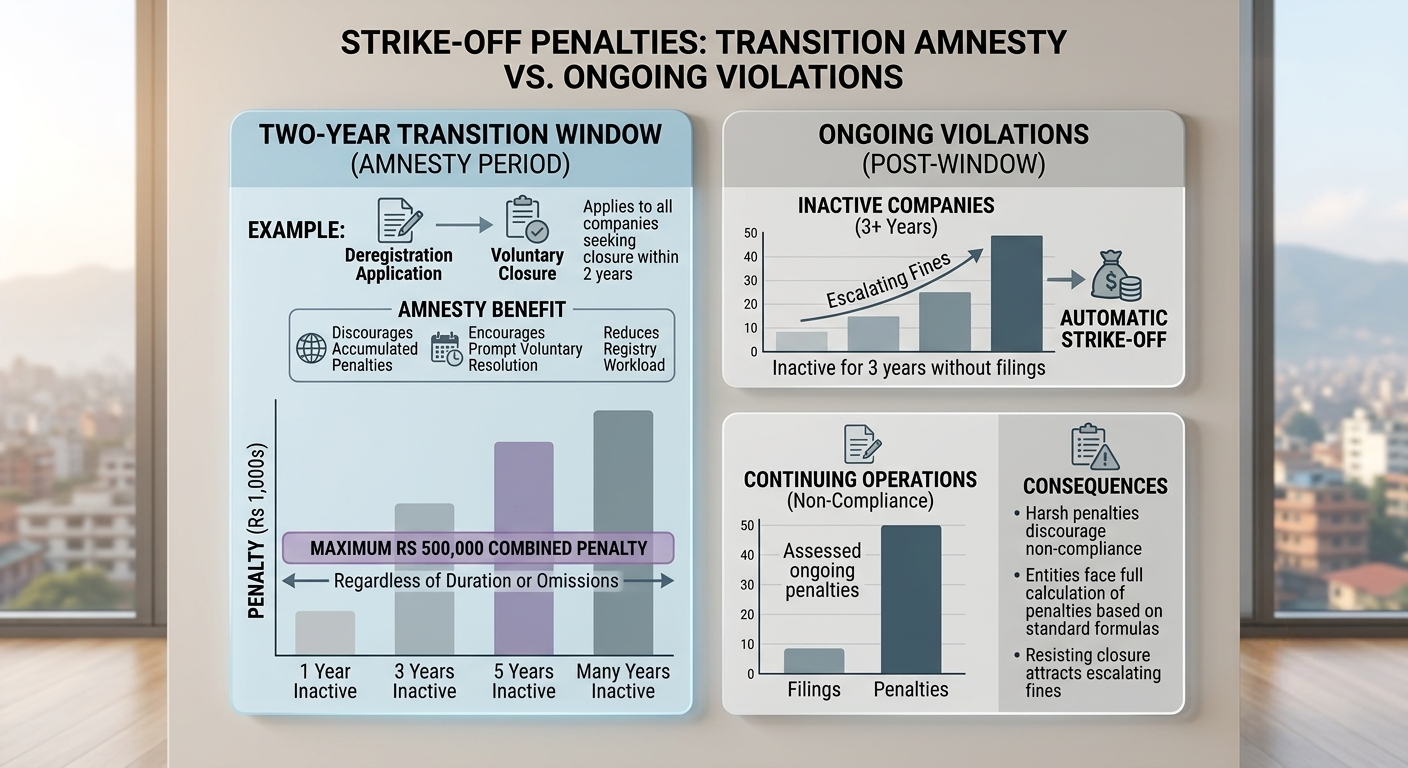

What specific strike-off penalties apply during the two-year transition window versus ongoing violations?

The act provides exceptional leniency during a two-year transition period from enactment. Companies applying for deregistration within this window face maximum Rs 500,000 combined penalties regardless of the specific number of years operating without filing financial statements or the magnitude of statutory violations.

A company dormant for five years but applying for deregistration within the two-year window pays Rs 500,000 maximum, compared to standard penalty formulas that might assess Rs 1+ million for such extensive non-compliance. This transitional generosity reflects government acknowledgment that thousands of companies accumulated penalties under previous regulatory regimes and that maintaining harsh penalties would discourage voluntary closure.

After the two-year window closes, standard penalties apply: companies inactive three consecutive years face automatic strike-off, while those actively resisting closure face escalating fines tied to violation type and duration. For companies continuing operations but failing financial statement submission, registrars assess ongoing penalties.

The time-limited amnesty incentivizes prompt voluntary resolution while preserving penalty mechanisms for entities continuing non-compliance indefinitely. Industry observers estimate that 5,000-10,000 registered companies never commenced operations, representing massive registry accumulation.

The two-year window likely triggers substantial voluntary deregistration applications as entrepreneurs facing Rs 500,000 maximum liability resolve long-dormant ventures, substantially reducing registrar workload and improving registry accuracy.

What are the new conversion procedures between private and public company status, and what asset transfer provisions apply?

The act enables private companies to convert to public status through shareholder special resolution (supermajority vote), modified governance documents, and registrar approval. All company assets, liabilities, contracts, and employee relationships automatically transfer to the converted entity without requiring separate conveyances. This automatic transfer mechanism prevents creating shell successors used to escape creditor claims or regulatory oversight.

Upon conversion completion, the registrar issues a conversion certificate establishing the entity’s new public status for all legal purposes. Conversely, public companies may convert to private status under specified conditions. The primary trigger involves shareholder count decline: if founder-shareholder numbers fall below seven, the company may petition for private status conversion.

A second trigger involves minimum capital erosion: if a public company fails maintaining capital minimums (Rs 250 million for listed entities, Rs 50 million for unlisted), it must convert to private status or recapitalize within six months. Companies must complete conversion procedures within six months of conditions arising, through amended governance documents and registrar submission. This structural flexibility enables efficient responses to changing circumstances.

A technology startup initially private may convert to public upon securing institutional investment or planning exit through public capital markets. A listed company consolidated through family acquisition may find private status appropriate, reducing quarterly disclosure obligations, auditor fees, and regulatory compliance costs.

The automatic asset/liability transfer prevents creation of successor entities used to escape obligations while permitting legitimate structural optimization.

What is the investor protection fund’s scale and permitted application categories?

The act establishes an investor protection fund receiving unclaimed dividends, shareholdings without identified owners, and related orphaned corporate funds. This pooled resource accumulates capital that companies previously retained indefinitely. The fund operates under explicit purpose restrictions: deployment only toward capital market development initiatives, investor education programs, and company law improvement projects.

The fund mechanism recognizes that legitimate shareholders sometimes miss collection deadlines due to relocation, illness, or death, with heirs occasionally unaware of shareholdings. Previously these assets remained corporate property indefinitely, essentially providing companies interest-free loans.

The fund consolidates resources for market-benefiting purposes rather than individual retention or government seizure. Shareholders retain permanent rights to claim historical entitlements through documented procedures, with registrars maintaining records enabling claim verification decades after initial non-collection. The fund serves custodial functions pending resolution of legitimate claims rather than acting as permanent seizure mechanism.

This framework reflects governance best practice acknowledging that unclaimed assets require stewardship—retained indefinitely by companies (inefficient) or seized by government (inequitable), but deployed toward market participant benefit. Nepal’s capital markets historically concentrated shareholding among institutional investors and wealthy individuals; retail participation remains limited.

Investor protection fund allocations toward education initiatives address documentation that many Nepali retail investors lack knowledge of trading mechanics, corporate financial analysis, and risk management principles.

These education programs funded through unclaimed dividend pools can improve market participation quality while making productive use of funds that individual shareholders abandoned or forgot.