Kathmandu

Saturday, July 25, 2026

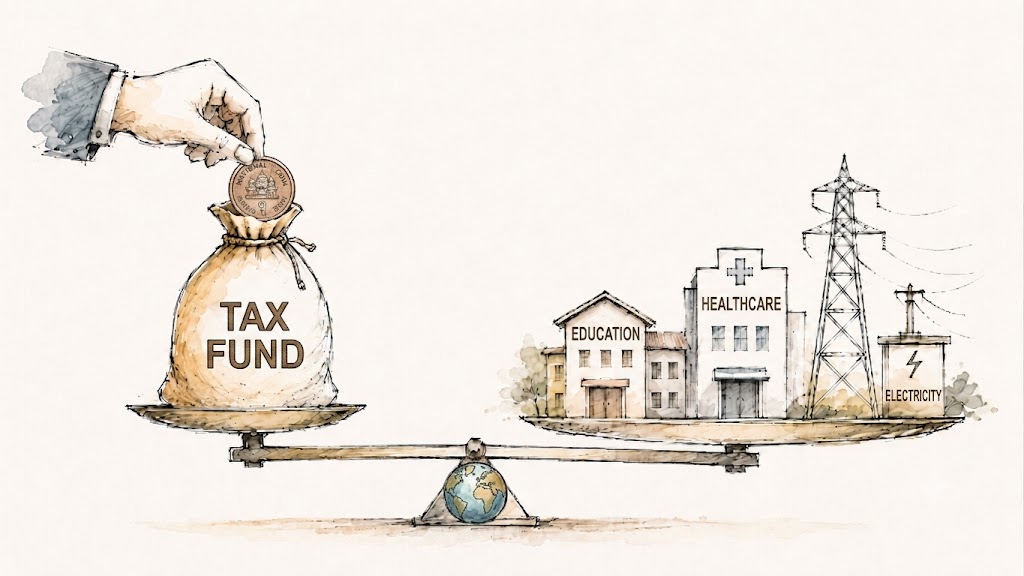

In Nepal, education, healthcare, and electricity have already been established as profit-generating commodities. Forcing their operators into the tax ambit—and levying a nominal additional fee on the consuming class to fund basic services for the marginalized—is a model example of progressive taxation and social justice.

KATHMANDU: Every year in Nepal, on May 29, the federal government presents its statement of income and expenditure (the budget) for the upcoming fiscal year. This proposal aims to run public administration, invest in infrastructure development, and fulfill state obligations defined by the Constitution. Shortly before and after the budget announcement, “taxation” becomes the primary topic of discussion among ordinary citizens, writers, intellectuals, bureaucrats, and journalists. Indeed, tax is such a powerful weapon of the state that if it is not wielded wisely, it can instantly inflict unparalleled impacts on income opportunities, livelihoods, as well as business assets and liabilities.

In the Nepalese context, the moment the words “budget” and “tax” are heard, most citizens perceive them either as developmental projects, salaries and allowances, or a sheer burden. However, the special contribution of taxes behind making public goods and services—like education, healthcare, roads, and security—and daily utility services like electricity and drinking water possible, is often ignored. This happens not out of ignorance, but rather due to a deliberate pretense of blindness. Constitutionally, tax is a medium through which citizens exercise their rights, and a tool for the state to fulfill its obligation to guarantee those rights. It is not a weapon of oppression.

Let us now discuss electricity—which has been taxed for the first time through the budget of the upcoming fiscal year—and education and healthcare operated as private institutions, which have been brought back into the tax ambit after being removed once before. A question has been raised here: is it justifiable for the state to impose an additional burden by taxing basic services like education, healthcare, and electricity, which should ideally be provided free of charge? The answer to this is simple: it is crystal clear that the Government of Nepal, under current circumstances, is in no position to provide these basic services to its citizens for free, let alone at cost price (a price equal to the marginal cost).

Recognizing this inability of the state, basic services like education, healthcare, and electricity were accepted as commercial goods, creating an environment where the private sector could turn a profit.

Compelling any profit-making business to comply with state laws and bringing it under the tax net is not only the government’s right but also its constitutional obligation. On one hand, this creates an environment that secures the inherent right of citizens to consume quality basic services. On the other hand, it helps manage resources to provide basic services below cost price or free of charge in non-profitable areas. The core issue here is that while the state exercises its right to collect taxes, that right must be used for social justice, the redistribution of income or dividends, and enhancing service quality. This is because taxation is not the state’s ultimate end; rather, it is merely a means of service delivery.

When discussing public finance and state authority, it is essential to understand the right to tax to raise investment sources for producing, constructing, or supplying public goods, along with its established theoretical dimensions. In modern governance, collecting taxes to provide public goods and services is a paramount function of the state. The state does not exercise this right arbitrarily; it is rooted in the principle of necessity in economics (the demand side), the principle of public service (the supply side), and the principle of benefit distribution (social justice). According to these principles, the state exercises its sovereign power to collect taxes from citizens and businesses and invests them to supply non-rivalrous and non-excludable public goods—such as security, the rule of law, basic energy, education, and healthcare—to its citizens.

Maintaining a balance between efficiency in tax collection and social justice in distributing the tax dividend is the primary challenge of public finance management, specifically regarding budget allocation and shifting the tax burden. This is the root cause behind the annual “bickering” over fluctuations or adjustments in tax rates accompanying the budget. The justification for the current taxes levied on education, healthcare, and electricity lies right here. When a basic service transforms into a profit-making commercial commodity, it loses the non-rivalrous and non-excludable characteristics of a public good. Consequently, a certain segment of society that cannot afford the price of such commercialized goods becomes deprived of their consumption.

It is the responsibility of the state to provide minimum basic services to this marginalized group, even if it means collecting taxes from the group capable of competing at market prices.

In this sense, the current government’s policy cannot be faulted for collecting a three percent equity tax from the segment capable of consuming expensive education and healthcare services, and investing that revenue to deliver basic education and healthcare to marginalized communities. Similarly, collecting Value Added Tax (VAT) from the segment that consumes massive amounts of electricity as a commercial input to generate income, and investing it in infrastructure for those who use it as a basic necessity, cannot be labeled an extra burden. The results of these policies look set to be positive in the future and beneficial for improving social welfare. Therefore, bickering over this matter is self-serving and amounts to opposition for the sake of opposition.

Why must the state adopt such a roundabout approach? It is because the private competitive market cannot provide public goods and services, as no one can be excluded from their consumption. Take security services, for example: even if a person does not pay taxes, they derive indirect benefits from a secure country. In economics, this is called the “free-rider problem.” While such a problem is unacceptable in businesses operated by the private sector, the government must provide free-rider services even if it means taking on debt. To internally resolve the problem of delivering services through borrowing, the state can exercise its special power to impose mandatory taxes. This is a sovereign right of the state, arising from the needs of the citizens themselves. Whether the state spends on citizens’ needs through taxes or loans, it is the citizen taxpayer who ultimately bears the liability for repayment.

At this point, a distinction must be made between a citizen and a taxpayer. It is a straightforward concept, but it has been heavily convoluted by self-serving arguments tailored to individual convenience. Not all citizens may be taxpayers in terms of the tax base levied on state protection, income generation, property, or business; however, all taxpayers can be citizens. Looking at it this way, the current government’s rationale holds ground: those taxpayers who have the capacity and willingness to pay consumption-based taxes are the very ones utilizing private education, private healthcare, and higher amounts of electricity. Therefore, collecting taxes from them to invest in marginalized groups is a textbook example of progressive taxation.

Had such investments been raised through loans instead of taxes, the burden would have fallen not just on the taxpayers capable of consuming these goods in a competitive market, but also on ordinary citizens paying ownership-based taxes—like property and land revenue taxes—and service fees for relationship verifications or recommendations. Such a tax burden tends to be regressive. Therefore, it is best not to bicker much over the new taxes introduced in the current budget, as they represent a model of progressive taxation.

International practice

Countries like Australia and the United Kingdom impose high taxes on tobacco products and alcohol to fund public healthcare. On one hand, this discourages citizens from consuming harmful products, while on the other, the revenue funds public hospitals and medicines. In neighboring India, while Goods and Services Tax (GST) is exempted on public education, healthcare, and basic electricity consumption, provisions exist to tax luxury and specialized private education, healthcare, and commercial electricity. In the United States, funds for running public schools are raised through local property taxes. This means the wealthy segment pays more taxes to send their children to expensive schools, while the poor pay less and receive services accordingly.

Since this system can still fail to cover those marginalized by economic inequality, state governments provide equalization grants to local governments.

Nearly a decade has passed since Nepal transitioned to federalism, and equalization grants are provisioned to manage fiscal disparity. While the local governments’ share of total public expenditure stands at around 20 percent, their internal revenue does not sustain even 25 percent of their total expenses. The rest relies entirely on grants from the federal government. Previous governments were not unaware of this reality; despite knowing everything, they refrained from taxing education, healthcare, and electricity for political popularity, causing the burden of debt and regressive taxes on all levels of citizens to skyrocket. The current government has stated that it will collect consumption-based taxes from those who can afford it and spend it on services for those who cannot and are marginalized. This requires everyone’s backing and cooperation.

In Nepal, federalism has granted local levels the authority over secondary education and basic healthcare services, but they lack the authority to levy consumption-based taxes on those services. Consequently, they must look toward the central government for local electrification, education, and healthcare services. Until citizens believe that the tax they pay goes directly to a school or a hospital, public accountability toward such taxes will not increase. The current government has stated that the equity tax paid on education and healthcare will be spent on the targeted groups for those exact services.

Therefore, citizens capable of consuming education and healthcare in a competitive market need to understand that the taxes they pay are utilized for marginalized citizens in remote areas. However, regular monitoring and vigilance are absolutely necessary to ensure that these funds are not misused.