Kathmandu

Wednesday, June 17, 2026

Slow growth, rising debt, and heavy reliance on remittances define the current outlook

KATHMANDU: Finance Minister Dr. Swarnim Wagle has presented Nepal’s current economic status report, in line with the announcement he made upon assuming office. The Ministry of Finance made the report public on Monday.

Despite abundant natural resources, a young population, and expanding infrastructure, the country has struggled for decades with weak governance, political instability, and deep-rooted structural economic challenges.

Prepared by the Ministry of Finance in April 2026, the report offers a candid assessment of where Nepal’s economy stands today, covering growth, public debt, trade imbalances, financial sector health, and key social indicators, while identifying the opportunities and policy pathways for meaningful economic transformation.

The report particularly analyzes the impact of the West Asian conflict on Nepal’s remittances and supply chains.

It also highlights the challenges Nepal faces after being placed on the Financial Action Task Force (FATF) grey list and as it moves toward graduation from the Least Developed Country (LDC) category.

How fast has Nepal’s economy been growing, and how does that compare to its neighbors?

Nepal’s economic growth over the past decade has averaged just 4.2 percent annually, which is significantly lower than most comparable developing economies in South and Southeast Asia. Within that period, growth has been volatile, swinging from a contraction of 2.4 percent to a peak of 9.0 percent in a single decade.

In fiscal year 2024/25, the economy grew at 4.61 percent, but growth is projected to slow further to 3.5 percent in fiscal year 2025/26. This sluggish pace reflects weak private investment, poor capital spending by the government, and a business environment that has failed to generate strong domestic demand.

Neighboring countries have consistently outperformed Nepal. The report does not shy away from this comparison, noting that the country’s growth trajectory looks quite slow when placed alongside peers in the region. The fundamental causes are identified as distorted incentive structures, rent-seeking over productive enterprise, and repeated policy inconsistency rather than any lack of natural potential.

What is the structure of Nepal’s economy, and is it changing in a healthy direction?

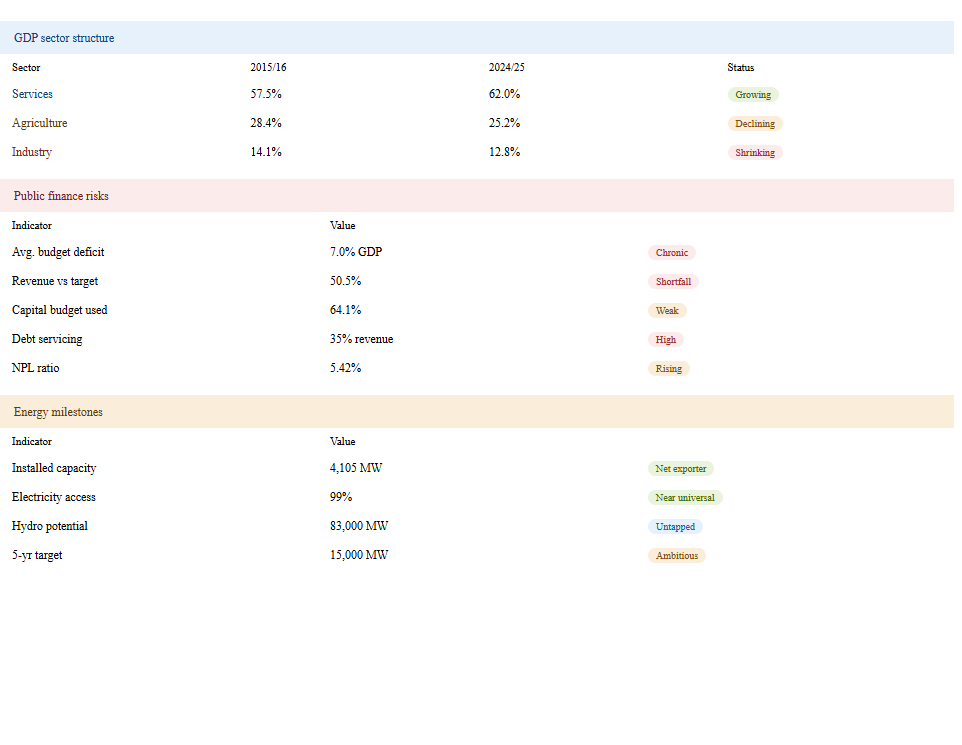

Nepal’s economy has shifted over the past decade, but not in the direction economists consider healthy. Agriculture’s share of GDP has fallen from 28.4 percent in fiscal year 2015/16 to 25.2 percent in fiscal year 2024/25. The services sector has grown from 57.5 percent to 62.0 percent over the same period. However, the industrial sector has actually shrunk, from 14.1 percent to just 12.8 percent.

This pattern is described in the report as “premature de-industrialization,” meaning Nepal has shifted away from agriculture without building up a strong manufacturing base in between. Normally, countries pass through an industrial phase where factory jobs absorb agricultural workers and raise productivity before moving on to services. Nepal has largely skipped this phase.

The manufacturing sector specifically has grown at an average of only 2.9 percent annually over the last decade, well below the overall economy’s average. High production costs, reliance on imported raw materials, low technology adoption, and limited investment are cited as the core reasons. This structural imbalance makes it harder to create the kind of stable, well-paid employment that drives broad-based prosperity.

How dependent is Nepal on remittances, and what risks does that create?

Remittances are the single largest stabilizing force in Nepal’s external economy. In fiscal year 2024/25, remittance inflows reached 28.2 percent of GDP, nearly equal to the entire value of goods imported into the country. In the first eight months of fiscal year 2025/26, remittance inflows grew by a further 37.7 percent, reaching Rs. 1.449 trillion.

Around 839,000 Nepali workers received labor approvals to go abroad in fiscal year 2024/25 alone, and over 557,000 had already done so by mid-March 2026 in the current fiscal year. Over the past decade, the number of workers going abroad has grown at an average of 28.6 percent annually.

The report is candid about the risks this creates. While remittances provide short-term relief for poverty, consumption, and the balance of payments, they cause a long-term drain of skilled and semi-skilled workers. They also reduce domestic wage pressure, weaken incentives for local investment, and create a structural vulnerability: if conditions in Gulf countries or other labor markets deteriorate, Nepal’s entire macroeconomic stability could be shaken quickly. The West Asia conflict is flagged as an immediate concern.

What is the state of Nepal’s public finances and government budget?

Nepal’s public finances show chronic structural weaknesses. Over the past decade, the federal budget deficit has averaged 7.0 percent of GDP annually. Revenue collection has consistently fallen short of targets, reaching only 87.6 percent of budget targets on average over the same period. In the first eight months of fiscal year 2025/26, revenue collection was only 50.5 percent of the annual target.

The federal government’s consolidated fund had a negative balance of approximately Rs 117 billion as of mid-March 2026, meaning the government was spending more than it was receiving in real time and borrowing to cover operational gaps.

A particularly troubling finding is that unpaid government liabilities from multi-year contracts amount to approximately Rs 402 billion, of which only Rs 128 billion was budgeted for the current year, leaving Rs 290 billion worth of obligations to be funded in future years. Health insurance claims owed but unpaid stand at approximately Rs 16.87 billion. The report describes the management of these growing payment obligations as a serious challenge that requires immediate attention.

How has Nepal’s public debt grown, and is it sustainable?

Nepal’s public debt has expanded dramatically over the past decade. As of the end of fiscal year 2014/15, public debt stood at 22.5 percent of GDP, equivalent to Rs 544 billion. By the end of fiscal year 2024/25, this had risen to 43.8 percent of GDP, or Rs 2.674 trillion. By February 2026, the total had climbed further to Rs 2.878 trillion, and by mid-March 2026, it reached Rs 2.929 trillion.

The annual average growth rate of public debt over this period was 17.6 percent. The report notes that while this level remains within internationally accepted management thresholds, it is only sustainable if the borrowed funds are used productively to raise economic output.

A particularly important concern is that debt servicing now consumes a very large share of public resources. In fiscal year 2024/25, principal and interest payments consumed 24.0 percent of total federal spending and 35.0 percent of total federal revenue. In fiscal year 2025/26, roughly 21.0 percent of the entire budget has been allocated just for debt repayment. This squeezes the space available for development spending and social programs.

How effective has capital spending been, and why does it matter?

Capital spending is critical because it is the mechanism through which governments build roads, irrigation, power projects, hospitals, and other long-term assets that raise private sector productivity and economic growth. Nepal has consistently underperformed in this area.

Over the past decade, capital expenditure averaged only 19.0 percent of total federal spending. More strikingly, only 64.1 percent of the capital budget allocated each year was actually spent. In fiscal year 2024/25, capital spending was just 14.8 percent of total expenditure. The government has repeatedly allocated ambitious capital budgets on paper while failing to implement them in practice.

The report identifies the quality of capital spending as a further concern, beyond just the quantity. Projects are delayed, poorly planned, and often selected without rigorous cost-benefit analysis. Meanwhile, current expenditure on salaries, subsidies, and administration has grown steadily, averaging 66.8 percent of total spending over the past decade. The imbalance between current and capital spending is seen as one of the most important structural barriers to Nepal’s long-term economic transformation.

What is Nepal’s situation in international trade, and how serious is the trade deficit?

Nepal’s trade situation is characterized by a deep and structural imbalance. Over the past decade, the merchandise trade deficit averaged 29.7 percent of GDP annually. As of February 2026, exports covered only 14.8 percent of imports, meaning Nepal imports roughly seven times as much as it exports in goods.

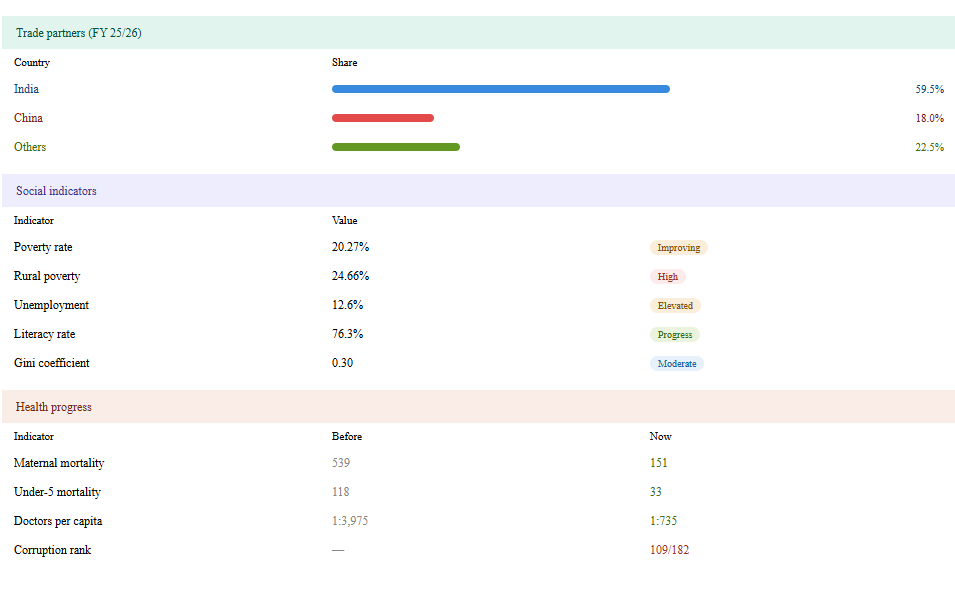

Nepal’s foreign trade remains heavily concentrated toward India, which accounted for 59.5 percent of total foreign trade in the first eight months of fiscal year 2025/26. China accounted for 18.0 percent, and all other countries combined for only 22.5 percent.

Exports have grown in nominal terms, from Rs 70 billion in fiscal year 2015/16 to Rs. 277 billion in fiscal year 2024/25. However, the report flags a distorting factor: re-exported vegetable oils, mainly soybean and palm oil, account for 39.4 percent of the total export figure and 42.2 percent in the current year. Strip out this re-export activity, and the underlying export base is very narrow. Nepal’s export strategy has not succeeded in building value-added manufacturing or diversifying into new product categories.

How is Nepal’s financial sector performing, and what are the key risks?

Nepal’s banking and financial sector has expanded substantially over the past decade. Private sector credit from banks and financial institutions grew from 55.2 percent of GDP in fiscal year 2014/15 to 91.6 percent in fiscal year 2024/25, a ratio that is now higher than India, Bangladesh, Sri Lanka, or Pakistan. Total deposits in the banking system stood at Rs 7.746 trillion as of February 2026.

However, there are growing signs of stress. The non-performing loan ratio, which measures the share of loans that borrowers are not repaying, rose from 3.02 percent in fiscal year 2022/23 to 5.42 percent by January 2026. While still within accepted thresholds on average, the trend is upward and concentrated particularly in development banks and finance companies.

Credit growth has been sluggish, growing only 4.4 percent in the first eight months of fiscal year 2025/26, reflecting weak business confidence and poor investment demand. The system holds excess liquidity: banks had parked Rs 904 billion in excess deposits with the central bank by mid-March 2026, up from Rs 654 billion in July 2025, because lending opportunities in the productive sector remain limited.

What is Nepal’s inflation situation and what is happening to the exchange rate?

Nepal’s inflation has moderated significantly in recent years. Average consumer price inflation was 4.1 percent in the previous fiscal year and fell further to an average of 2.13 percent in the first eight months of fiscal year 2025/26. This reflects weak domestic demand, slow credit growth, and relatively low imported inflation.

While overall price stability has been maintained, the report notes that prices of key daily consumption goods still fluctuate noticeably in the market. The ongoing conflict in West Asia has begun pushing petroleum product prices higher, which poses a fresh inflationary risk given Nepal’s heavy dependence on fuel imports.

On the exchange rate, Nepal has maintained a fixed peg of its currency to the Indian rupee for 33 years, since 1992. However, against the US dollar, the Nepali rupee has depreciated substantially: from Rs 49.80 per dollar in 1992 to Rs 150.67 per dollar by mid-March 2026. The real effective exchange rate is assessed as somewhat overvalued. This depreciation automatically increases the local currency cost of dollar-denominated foreign debt and makes imports more expensive, adding fiscal and trade pressures simultaneously.

Where do Nepal’s foreign exchange reserves stand, and are they adequate?

Nepal’s foreign exchange reserves are currently at a comfortable level, largely because of high remittance inflows. As of February 2026, total foreign exchange reserves stood at Rs 3.414 trillion, equivalent to approximately USD 23.08 billion. This is sufficient to cover 18.5 months of goods and services imports, well above the standard international benchmark of three months.

The current account has been in surplus for the past two fiscal years, with a surplus of Rs 409.20 billion in fiscal year 2024/25 and Rs 552.85 billion in the first eight months of fiscal year 2025/26. The balance of payments overall recorded a surplus of Rs 658.35 billion in the same period.

The report, however, cautions that this reserve comfort is structurally dependent on remittances rather than on export earnings or productive foreign investment. The underlying trade deficit remains wide. If remittance flows were to slow due to geopolitical disruptions in the Gulf region or policy changes in labor-receiving countries, the reserve position could deteriorate rapidly. The report calls for developing alternative sources of foreign exchange through productive investment and export expansion.

How has Nepal performed on poverty, unemployment, and inequality?

According to the most recent Nepal Living Standards Survey conducted in fiscal year 2022/23, approximately 20.27 percent of Nepal’s population lives below the poverty line, equivalent to about 6 million people. This is down from 25.16 percent recorded in the fiscal year 2009/10 survey, but the pace of reduction has been slowed by the COVID-19 pandemic and other disruptions.

Rural poverty stands at 24.66 percent and urban poverty at 18.34 percent, reflecting the persistent rural-urban divide. In some municipalities, small-area poverty estimates show that more than 70 percent of the local population lives in absolute poverty.

The youth unemployment rate is particularly alarming at 22.7 percent for those aged 15 to 24. Overall unemployment stands at 12.6 percent nationally, with women’s unemployment at 13.1 percent and men’s at 10.3 percent. Of those who do have jobs, 64.9 percent are engaged in daily wage labor, with no job security or benefits. The Gini coefficient, which measures inequality, stands at 0.30, with urban areas slightly more unequal than rural ones. Gender inequality in property ownership is stark: women hold individual ownership of only 24.2 percent of privately owned land.

What is the state of Nepal’s electricity sector and hydropower development?

Electricity generation represents one of Nepal’s genuine success stories and the area of most dramatic progress in recent years. Total installed generation capacity stood at just 697.85 megawatts after a century of hydropower development up to July 2011. Since then, capacity has grown nearly sixfold in a much shorter period, reaching 4,105 megawatts by February 2026. Electricity access has been extended to 99 percent of the total population.

Nepal has crossed an important threshold: it is now a net exporter of electricity. However, the country still needs to import power during dry seasons when river flows fall and run-of-river hydro output drops. Many additional projects remain under construction.

Despite this progress, critical challenges remain. Transmission line capacity is insufficient to carry all the electricity being generated to consumers and export markets. Domestic electricity consumption needs to grow substantially to absorb new capacity and improve the commercial viability of projects. The report calls for prioritizing reservoir-based hydropower and solar energy to address seasonal supply gaps and for building transmission infrastructure in parallel with generation projects to avoid stranded assets.

How is Nepal performing on education and health outcomes?

On literacy, Nepal has made meaningful progress. The literacy rate for those aged six and above reached 76.3 percent by the 2021 census, up from 58.0 percent in the 2011 census. School enrollment rates at the primary and lower secondary levels remain above 95 percent in recent years.

However, the quality of education is a growing concern. The report identifies a widening mismatch between what the education system produces and what the labor market needs. Vocational and technical training remains underdeveloped, and graduate unemployment is rising sharply. Secondary completion rates fell to 35.4 percent in 2025, a worrying sign.

On health, Nepal has achieved substantial reductions in maternal and child mortality. Maternal mortality fell from 539 per 100,000 live births in 1996 to 151 by 2022. Under-five mortality dropped from 118 to 33 per 1,000 live births over the same period. The doctor-to-population ratio improved to one doctor per 735 people by 2025 from one per 3,975 in 2005.

Despite these gains, quality and accessibility remain problematic. Rural populations still lack reliable access to specialist care. Nepal’s health insurance program is facing a financial crisis, with unpaid claims causing hospitals to suspend services to insured patients, threatening the program’s viability.

What challenges does Nepal face with corruption, governance, and international financial compliance?

Governance quality is identified in the report as one of the most fundamental constraints on Nepal’s development. Transparency International’s 2025 Corruption Perceptions Index gave Nepal a score of just 34 out of 100, placing it at rank 109 out of 182 countries globally. This reflects widespread irregularities in the public sector and the weak effectiveness of regulatory and enforcement institutions.

Unaudited government liabilities accumulated over years remain unresolved. The 62nd report of the Auditor General found total unresolved audit irregularities of Rs 733.19 billion across all three tiers of government up to the end of fiscal year 2023/24, with Rs 91.59 billion added in that single year alone.

Nepal was placed on the Financial Action Task Force grey list in February 2024, meaning the international financial community has formally flagged concerns about anti-money laundering and counter-terrorism financing controls. Despite legal and policy reforms being enacted, the report concedes that effective enforcement and tangible results remain inadequate. This designation risks complicating international banking relationships, foreign trade financing, and investment flows if not resolved through demonstrated implementation.

What is the situation with Nepal’s subnational governments under the federal structure?

Nepal adopted a federal structure with three tiers of government in 2015, but significant challenges persist in making decentralization work effectively. In fiscal year 2024/25, the federal government accounted for 65.6 percent of consolidated public expenditure, while provincial governments spent 9.8 percent and local governments 24.6 percent.

Revenue generation at subnational levels remains very weak. The federal government collects 92.1 percent of all government revenue, with provinces and local governments together collecting only 7.9 percent. This creates heavy dependence on federal transfers.

Budget utilization rates at subnational levels are also low: provinces spent only 71.3 percent of their allocated budgets and local governments 76.4 percent in fiscal year 2024/25. Limited technical and managerial capacity at the local level is identified as the primary reason. The report notes that subnational governments sitting on unspent funds while development needs go unmet is a direct brake on aggregate economic demand and public service delivery. Strengthening subnational capacity and clarifying functional assignments between tiers are identified as urgent priorities.

What are the main opportunities Nepal has for economic transformation?

Despite the serious challenges catalogued throughout the report, the Ministry of Finance identifies multiple credible pathways to economic transformation. The most significant revolves around hydropower: Nepal has an estimated potential of 83,000 megawatts, of which only 4,105 megawatts have been developed. Scaling up to 15,000 megawatts within five years, as the government targets, could anchor industrialization, support energy-intensive manufacturing, and generate stable export revenues through regional electricity trade.

Tourism, agriculture modernization, digital services, and export-oriented manufacturing are also highlighted. Nepal’s geographic position between India and China offers transit and logistics opportunities that have barely been tapped. The remittance economy, if redirected toward productive investment through entrepreneurship support and skills development, could become a driver of domestic capital formation rather than simply a consumption subsidy.

The overarching vision stated in the report is to achieve average economic growth of seven percent annually starting from the next fiscal year, raise per capita income above USD 3,000 within five to seven years, and bring the total size of the economy close to USD 100 billion, qualifying Nepal as a lower-middle-income country with genuine dignity.

What does Nepal need to do to achieve its economic goals, and what are the biggest barriers?

The report is direct in its diagnosis: Nepal’s core problem is not a shortage of resources but a failure of governance, policy consistency, and institutional capacity. The country has water, forests, minerals, a young population, and significant natural beauty. What has been lacking is the political will and administrative capability to convert these into sustained growth.

The most urgent priorities identified include fixing the business environment so that private investment, both domestic and foreign, becomes genuinely attractive. This means protecting property rights, enforcing contracts, reducing regulatory burdens, and creating a transparent and predictable tax system. The report explicitly criticizes the current system where business success depends more on access to licenses and connections than on innovation and productivity.

Structural reforms in public financial management, including rationalizing social protection spending, improving capital budget execution, reducing the informal economy’s size, and broadening the tax base, are all described as essential. The report also calls for serious action on corruption, resolution of the FATF grey list status, upgrading credit ratings toward investment grade, and developing the capital market. Ultimately, the report frames economic transformation as inseparable from political and governance reform: without reliable, honest, and capable state institutions, policies will continue to be implemented poorly regardless of how well they are designed on paper.